by Chris Becker

The “nuanced” view of local economists is superior to that of outside observers, according to the NAB, who has lambasted Paul Krugman’s recent dour take on the domestic economy today in Fairfax.

Here are the seven reasons Peter Jolly, head of research at NAB, cites as not being concerned about Australia, with my responses in bold

1. The Chinese economy is slower but it’s not collapsing. Correct: but its the deceleration of growth that the Australian economy cannot absorb as it has hitched all and sundry to the ChinaForever boom. Moreover, the composition of Chinese growth is changing, from commodity-intensive fixed asset investment (e.g. infrastructure and property construction) towards domestic consumption. Both are unambiguously bad for Australia.

2. Commodity prices are lower but Australian producers have in turn lowered their costs and are profitable. Correct: but they are not making nearly as much money as before, so the Terms of Trade is collapsing, hence lower income for the country. Commodity supply is still increasing as well, which means lower prices. Moreover, the cost-cutting by the miners is delaying the necessary adjustment to the supply-side and means that commodity prices will have to head even lower still to mothball the marginal producers (e.g. FMG and Atlas Iron).

3. The Aussie dollar has fallen a long way. It has also fallen more than commodity prices. What? Iron ore, LNG and oil are all down nearly 50% in the last 12 months, the AUDUSD is only off 25% in the same period. And it will fall further. The lower AUD also means that the purchasing power of households will fall further as import costs rise.

4. The non-mining economy is improving. The RBA normally hikes rates when business conditions are this strong. Well kind of: It’s not improving enough to fill the capex hole nor the reduction in growth from mining exports. The RBA knows this. Conditions are also only “this strong” because of the epic housing bubbles in Sydney and Melbourne, which are not sustainable. One they burst/deflate, it’ll be tough times given the lack of other drivers.

5. The unemployment rate has stabilised and jobs are being created. Sure. But this is because of unsustainable housing bubbles in Sydney and Melbourne. The problem comes in 2016-17 when mining investment craters, the car industry shuts down, and housing prices and construction unwinds.

6. The RBA is concerned about house prices. They bloody well should be. Where’s your concern?

7. The RBA governor implies the hurdle to cut again is high, and there’s a need to consider near and long term factors. He’s got a point here because we are fast coming to a point where a rate with a 1 in front of it implies convergence with US interest rates. But it will be forced to cut again given the headwinds outlined in point 5.

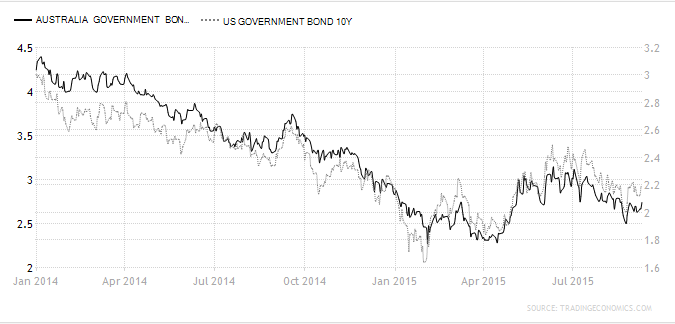

The US economy is doing much more swimmingly than Australia, with unemployment falling, GDP growth accelerating and its currency appreciating across the board. The gap between US Treasuries and Australian government 10 year bonds is closing swiftly – 2.16% vs 2.73% – not a good trend for the 70% plus foreign owners of the latter with a Federal Reserve eager to raise rates.

The AAA rating is under threat if interest rates are cut too low as the crucial 30% debt to GDP level is breached by fiscal deficits that are set to expand automatically as the economy struggles to grow at all.

Nuance is not a village in Southern France, it seems to be a new trademark for blinkers worn by market economists.