The Committee for Economic Development Australia (CEDA) has released a new paper, The super challenge of retirement income policy, outlining its plan for retirement reform.

The paper argues that Australia’s ageing population and decreasing housing affordability means the current structure and policies in place may not be robust enough to ensure that Australians can retire comfortably in the future, and are likely to put unsustainable pressure on the Federal Budget.

With the old age dependency ratio (the number of people over 65 for every working-age person 15 to 64) set to double over the next 40 years, there will be significantly fewer taxpayers supporting a growing demand for pensions and services including health and aged care. When combined with the continually declining home ownership rate amongst younger cohorts, more people will retire without owning their home and an increasing number of retirees will likely to be at the mercy of the private rental market.

Therefore, CEDA argues that the current structure of Australia’s retirement system needs to be reviewed or Australia risks more Australians living in poverty in retirement. The poverty rate of older Australians is already three times the OECD average, and that statistic is likely to worsen if Australia does not review the structure of our retirement system.

CEDA makes some sensible suggestions, such as reforming superannuation concessions, which overwhelmingly benefit the wealthy. The report notes that superannuation concessions “primarily benefit the rich, with the top 20 per cent of income earners accounting for 58 per cent of superannuation tax concessions (including concessions on earnings)”, and that this “is an equity concern”.

It recommends mandating that superannuation contributions be made from after-tax (net) income and including the family home in the assets test for the Aged Pension as part of the same reform.

It also calls on super funds to provide products, such as deferred lifetime annuities, that offer longevity protection to help retirees better manage their funds and reduce under-consumption.

However, CEDA also stupidly calls for demand-side policies to assist home ownership, including allowing first home buyers (FHBs) to use their superannuation to purchase a home, and allowing mortgage payments to be made from pre-income tax:

Owner-occupied housing (also known as the family home) is a key component of the third pillar of the retirement income system (voluntary private savings). However, the system should better recognise the extent to which owner-occupied housing contributes to household wealth and retirement liveability. People who do not own homes are exposed to the high-cost rental market and risk poverty in retirement. Home ownership continues to decline among young Australians, more of whom are expected to retire without owning a home.

The government should recognise the role of housing in poverty alleviation and in contributing to the objectives of providing for a decent retirement. It should:

– Allow first home buyers to access superannuation funds to purchase owner-occupied housing; and

– Address housing affordability, including for rental and social housing…

Given the importance of housing for retirement, another option would be to allow mortgage payments to be made pre-income tax. This would allow two important components of retirement savings – superannuation and the family home – to be treated the same.

As I have noted previously, when Nick Xenophon and Joe Hockey first canvassed allowing FHBs to use their super to purchase a home, CEDA’s demand-side reforms would likely be self-defeating and simply push-up house prices.

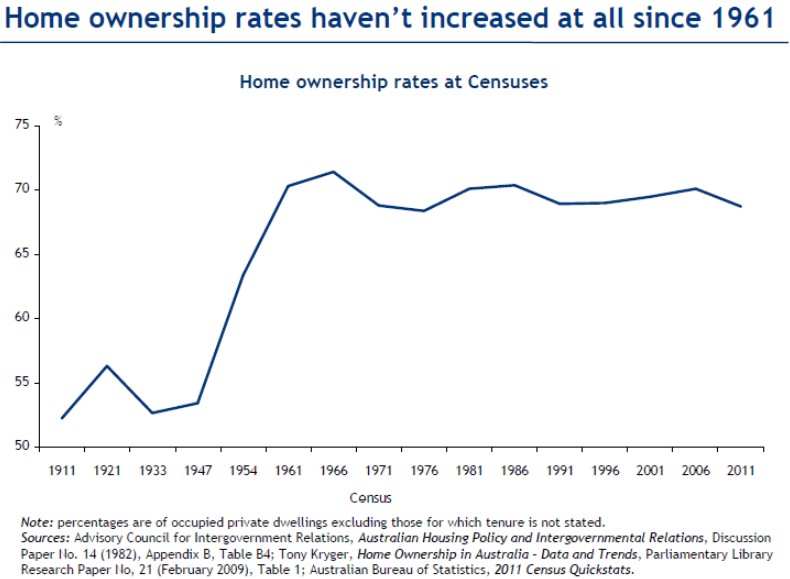

Saul Eslake’s 50 Years of Housing Policy Failure presentation showed us unequivocally that demand-side measures aimed at promoting “housing affordability” and home ownership do not work. Despite the massive decline in interest rates and the myriad of subsidies provided to first home buyers, the home ownership rate has decreased over the past 50 years (see next chart).

Under Australia’s constipated planning system, CEDAs proposed demand-side reforms reform would increase buyer’s capacity to pay and would soon be capitalised into higher home prices. At the same time, Australian’s retirement savings would be compromised for little additional benefit, potentially placing further strain on the Aged Pension.

Canada’s Garth Turner, who oversaw the introduction of a similar housing-super system in Canada in the 1990s, has admitted that it was a massive mistake, placing further upward pressure on Canadian house prices and putting at risk retirement savings.

As I have argued previously, there are really only two approaches to improving housing affordability and boosting home ownership rates:

- Removing artificial (speculative) demand from the market; and/or

- Introducing measures that improve the supply of affordable land/housing.

This is where CEDA’s focus should be, not on adding more mortgage fuel to the housing bonfire.

unconventionaleconomist@hotmail.com