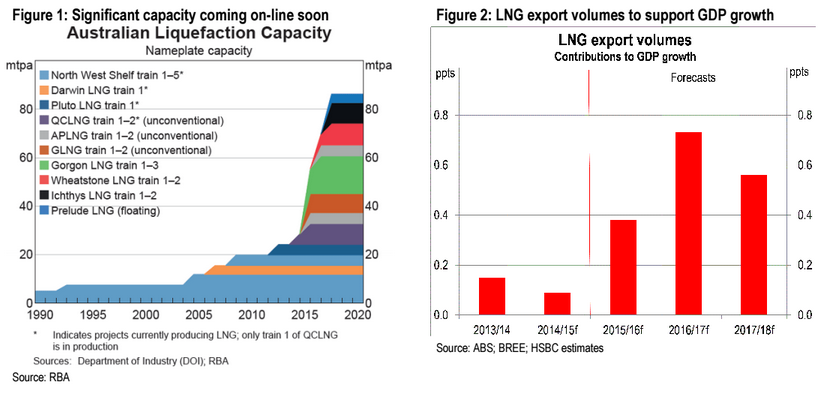

Australia’s much-anticipated ramp up in liquefied natural gas (LNG) exports has not arrived yet, but it will be here soon. And when it happens, it will be big! As is by now well understood, new LNG plants were the largest part of Australia’s resources investment boom. The capital spend was enormous, at over $220 billion. These plants are set to take export capacity from 20mtpa to 85mpta, making Australia the world’s largest LNG exporter by 2018. Also, with the LNG forwardsold on long-term contracts to Asia, the ramp up in exports is pretty much ‘baked in’. Although not quite in the monthly numbers yet, this ramp up should start to show up soon and is expected to contribute a hefty average of around 0.6ppts to GDP growth in each of FY2016, 2017 and 2018. It is hard to get the overall economy to look too weak with that sort of positive contribution.

Australia’s LNG story has been playing out over a decade, so it is easy for tick-by-tick market observers to lose patience with the narrative. Nonetheless, it grinds on. Recall that Australia has been in the process of building eight major LNG projects since construction commenced on the first, and largest, of the projects in 2009 (we set out the details here: ‘Downunder Digest: Australia’s LNG export boom to begin’, 30 October 2014).

Only one of the projects is now complete and moving into production, but all of the projects are expected to move into the production phase over the next two years. This is an important story that puts Australia in a different position to many other nations when it comes to trade. Although global trade remains weak, the ramp up in LNG production will almost certainly see Australia’s export volumes grow strongly over the next 2-3 years (Chart 1 and 2).

This is in addition to the pick-up in exports of tourism and education services that is currently being supported by the lower Australian dollar (something we have written about recently, see ‘Australia’s next growth driver: The rise of the services sector’, 10 July 2015).

Based on the capacity that is being built, official estimates show that LNG exports are set to rise from around 20 million tonnes per annum (mtpa) currently to around 85 million tonnes per annum (mtpa) by 2018. Australia is set to overtake Qatar, which currently produces one-third of globally traded LNG, to be the largest exporter of LNG.

These exports have been forward-sold on longterm contracts, mostly to Japan, China and South Korea. Of course, if Asia were to see weaker conditions than currently expected, this would affect the story, although most likely by pushing down the price, rather than volumes.

It is, of course, volumes that drive real GDP. Although there is considerable uncertainty about the pricing formulas that have been used in the forward-contracts, most of them have been benchmarked to the oil price. The sharp fall in oil prices since mid-2014 is therefore likely to limit the short-term profitability of many of the projects. Reduced profitability of the projects would weigh on corporate and state tax revenues. That is, GDP growth would still be supported, but local income growth could be weaker.

However, production is still expected to ramp up, which forms part of it intensive projects with huge fixed costs, so reducing or cutting production only weighs even more heavily on profitability. Besides, these projects have also been built with 30-50 year production horizons in mind. Weak short-term profitability (or even losses) should not stop the ramp up in volumes on the assumption that, at some point, the plants will be profitable.

From Australia’s perspective it is also worth noting that these projects are almost entirely owned and run by global multi-nationals. Although Australia’s economy may therefore not have benefited from all of the upside from these projects, it should also only be expected to suffer from part of any downside. There is a clear risk-sharing relationship with the rest of the world at work.

While some observers are, once again, starting to get worried that Australia could see a recession at the end of the mining boom, we remain more positive. As we noted last week, much of this positive view is due to the current upswing in the housing and services sectors, supported by low interest rates and recent falls in the Australian dollar. The expected ramp up in LNG exports is another important element in the story that should not be forgotten.

Who has forgotten it? I would argue that with the emerging market and commodity unwind that we are seeing, Australia’s LNG ramp up is actually the cause for increasing focus and concern. Markets disagree with Bloxo’s happy tone, they are not ignoring it. That’s why LNG equity is falling apart.

And why not? The volumes-led GDP Bloxo champions is in doubt at the margin. Prices have fallen far enough to already to question bullish volume assumptions and they are going to go lower. Aside from anything else the GDP uplift is more than offset by the capex downdraft rendering Bloxo’s analysis suspiciously partial.

As well, the incipient glut is so enormous as Asian demand shunts structurally lower than assumed that contracts are not worth the paper they are written on and prices are going stay much lower for much longer than the economics of projects assumed ensuring massive write downs and no profits for as far the eye can see. It’s not GDP that makes you rich, it’s profits.

Advertisement

Finally, Australia’s parasitic services economy has already leveraged the GDP in advance through another salivating housing boom ensuring that the disappointing GDP delivered will fail to repair extended national offshore borrowing ratios.

LNG is not the national saviour on any timeline that matters to you and I. It’s a millstone around our necks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.