From Christopher Balding:

- Did China free the RMB to market forces? Yes and no. China is allowing the market to influence the RMB price that the PBOC announces every morning but the PBOC still retains ultimate authority over the official trading price. The PBOC will take into account the actual trading price of the RMB from the previous end of day when setting the new official price. The gives the market influence in setting the new price but the PBOC retains ultimate authority.

- Did China take this action with the RMB to try and join the treasured SDR, jump start growth by increasing exports, or due to increasing pressure on the RMB? Probably all of the above in happy coincidence more than masterful design. Let me rephrase the question to make my point. Would China increase market influence on the RMB to please the IMF if the economy was strong and capital was not rapidly leaving the country? I think that would be considered very unlikely. China had no problem thumbing its nose when complaints were flooding in that the RMB was undervalued, so I would consider it unlikely that China is doing this to please the IMF with an eye towards joining the SDR.

- Is China starting a “currency war”? Yes and no but more no than yes. Journalists and politicians have fallen back on the tired cliche that Beijing is starting a currency war as a way to stimulate growth at the expense of other countries. There are multiple problems with this narrative though. First, the total decline so far is a little more than 4%. That isn’t enough to seriously stimulate Chinese exports Paul Krugman has pointed out. For the world’s second largest economy any increase resulting from 4% would be little more than statistical noise. Second, a significant share, though less in recent years, of Chinese exports is processing trade of imported inputs. Consequently, while export prices may decrease, import prices will increase essentially washing any advantage. For instance, a large percentage of “high tech” exports rely heavily on imported components acting effectively as an assembly center.

- China can devalue the RMB because it doesn’t need to worry much about foreign denominated debt. Yes and no. As a percentage of GDP and financial markets, China has relatively little foreign currency denominated debts. According to a recent estimate, China has approximately $1.3 trillion in foreign denominated debt. While that may be small in relative terms, given the nature of a credit stressed economy, the relative concentration in strategic sectors like real estate and carry trading, and the Beijing hope that foreigners would buy a lot of government bonds at friendly rates, the lower value of the RMB is going to have an oversized impact. Given that approximately 500 firms still have suspended trading in shares due primarily to debt covenants that would require additional collateral after share price falls, 3.6 trillion in provincial debt restructuring due to loans coming due, and now $1.3 trillion in foreign debt, the Chinese economy should be considered a very credit stressed economy.

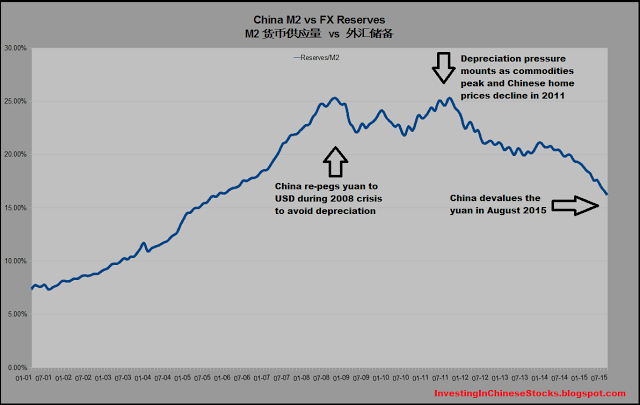

- With $3.6 trillion in reserves, China will have no problem defending the RMB and imposing its preferred value on the market. Yes and no but more no than people think. One of the most common

mistakes people make looking at Chinese data is distinguishing between absolute and relative data. $3.6 trillion is a large amount of reserves in absolute terms but much smaller in relative terms. According to my calculations, reserves relative to nominal GDP for 1997-8 Asian tigers is 23% compared to China’s current 34.7%. However, if you compare reserves to M2 money supply the picture is much different. By that measure, China only has reserves equal to 17% of M2 versus 28% in 1997-8 Asian tigers.

mistakes people make looking at Chinese data is distinguishing between absolute and relative data. $3.6 trillion is a large amount of reserves in absolute terms but much smaller in relative terms. According to my calculations, reserves relative to nominal GDP for 1997-8 Asian tigers is 23% compared to China’s current 34.7%. However, if you compare reserves to M2 money supply the picture is much different. By that measure, China only has reserves equal to 17% of M2 versus 28% in 1997-8 Asian tigers. - What is driving the downward push in the RMB? Confidence in the Chinese economy or more accurately, the lack thereof. Beijing officialdom and the PBOC can insist until they are red in the face that the economy is fine and there is no basis for the market pushing the RMB lower, but much like the official 7% GDP growth or Chinese milk powder, no one is buying it. Well heeled Chinese have been moving assets abroad for some time, a process which has sped up, and Chinese firms, especially those with international interests, have been stashing cash abroad as well. Debt and stock markets being propped up to avoid collapse coupled with deflation have never been known to be an investor paradise. These are characteristics of an economy that investors and citizens seek to take their money out of and put it elsewhere.

Some very clear thinking there (the chart is from Investing in Chinese Stocks. More at Balding’s World.