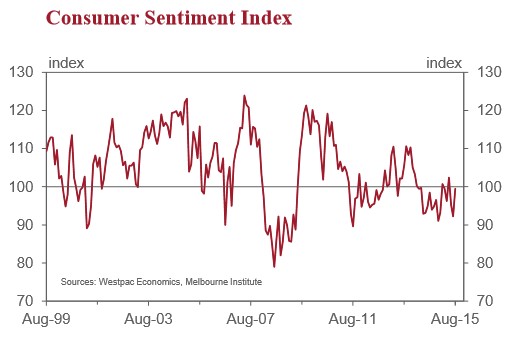

The Westpac-Melbourne Institute consumer sentiment index for August has been released, which rebounded sharply, rising 7.8% to 99.5 (from 92.2 in July), with the number of optimists and pessimists now almost equal:

According to Westpac chief economist, Bill Evans, the result was buoyed by the strong rise in house prices:

This is a very surprising result. Movements of the Index of this magnitude are unusual and generally associated with highly significant events such as interest rate moves or Commonwealth Budgets. There is no comparable event they may have triggered this response although the solution may lie with international issues and housing.

Last month we conjectured that the main reason behind the 3.3% fall in the Index related to concerns around global issues associated with Greece and the Chinese equity market. That fall had followed a fall in June of 7.1% (also influenced by concerns around Europe in particular) from the big increase in May (8.0% jump) which was most likely associated with the Reserve Bank’s rate cut in early May and a positive response to the Commonwealth Budget.

It seems that with the tensions in Greece and the Chinese equity market no longer dominating the media consumers are feeling more relaxed. However, the Index remains below 100 and is therefore the 16th reading out of the last 18 where the Index has been below 100 indicating that pessimists have consistently outnumbered optimists.

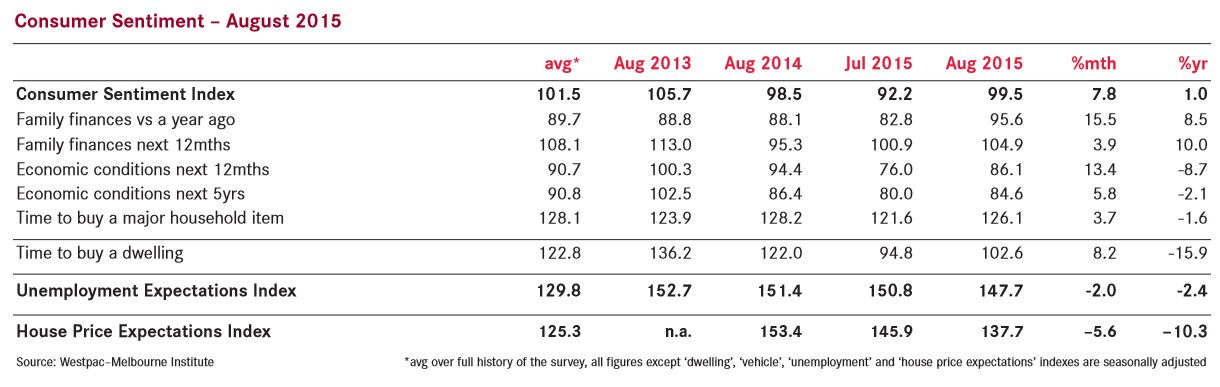

Ongoing positive news around house prices may also have buoyed confidence. Certainly there was a much larger lift in the confidence levels of those respondents who wholly own a property (up 6.2%) or who hold a mortgage (up 11.0%) than those who are out of the housing market (up 4.3%).

However Confidence is not being boosted by the expectation of more interest rate relief. In our special question around the outlook for mortgage rates 55% of respondents expect mortgage rates to rise over the next 12 months; 35% expect rates to be steady; and 5% expect further rate cuts (5% with no opinion).

However, Evans is not convinced that the sentiment rally will last:

Over that 18 month period there have been two months (following the RBA’s rate cuts in February and May) when Confidence has rallied but this has not proved to be sustained.

I expect that this current “rally” will equally prove to be unsustainable particularly given a resurgence of concerns around China and the evidence last week that the unemployment rate lifted to 6.3%.

The rise in the overall Index was associated with a modest improvement in respondents’ confidence around the labour market. The Westpac Melbourne Institute Index of Unemployment Expectations fell by 2.1% following a 1.3% fall in July (a lower level indicates that respondents are more confident with the labour market outlook). However the Index is still above the level in May and 6% above the level in October 2011 immediately before the Reserve Bank began its easing cycle.

Nevertheless, the rise in sentiment was broad-based, even though it was housing driven:

Not surprisingly, all components of the Index increased. Possibly reflecting the house price theme we saw a huge lift in “family finances compared to a year ago” of 15.5% while “family finances over the next 12 months” rose by 3.9%.

Prospects for the economy, possibly influenced by a more settled global outlook, also lifted. “Economic conditions over the next 12 months” rose by 13.4% and “economic conditions over the next five years” was up by 5.8%. However note that these two components are still down on a year ago: –8.7% and –2.1% respectively.

“Whether now is a good time to buy a major household item” rose by 3.7% but is also still down 1.6% on last year.

Sentiment towards housing improved. “Whether now is a good time to purchase a dwelling” increased by 8.2%. But that really only represents a recovery from the precipitous fall last month of 15.4%. The level in August is still 8.5% below the level in June and still represents the second lowest print for this Index since November 2010 – the aftermath of the Reserve Bank’s rate hike cycle. There was only one state, New South Wales, where the Index fell further (– 3.3%) from the July level. The Index for New South Wales is now 22% below its level two months ago. This sentiment is probably being driven by concerns around both affordability and prospects for prices.

Respondents were less confident about the outlook for house prices. The Westpac–Melbourne Institute Index of House Price Expectations fell by 5.6% (to 137.7) from its level in July (145.8) and is now down by 10.3% over the year.

Westpac now believes that interest rates will remain on hold for the remainder of this year and next, and does not agree with the RBA’s bullish growth forecasts:

“The Reserve Bank Board next meets on September 1. There is very little chance that the Board will choose to move rates. Westpac expects that rates will remain on hold over the course of the remainder of this year and in 2016.

It is notable that the Reserve Bank’s forecasts in its recent Statement on Monetary Policy include a 3% growth forecast in 2016 lifting to a “heady” 3.75% in 2017. We are much more circumspect about the growth outlook in 2017. If, however, it became clear through the course of 2016 that the 3.75% growth outlook was likely to be achieved, and even exceeded, then rate increases would quickly move onto the radar screen.

Below are the changes in the sub-index components:

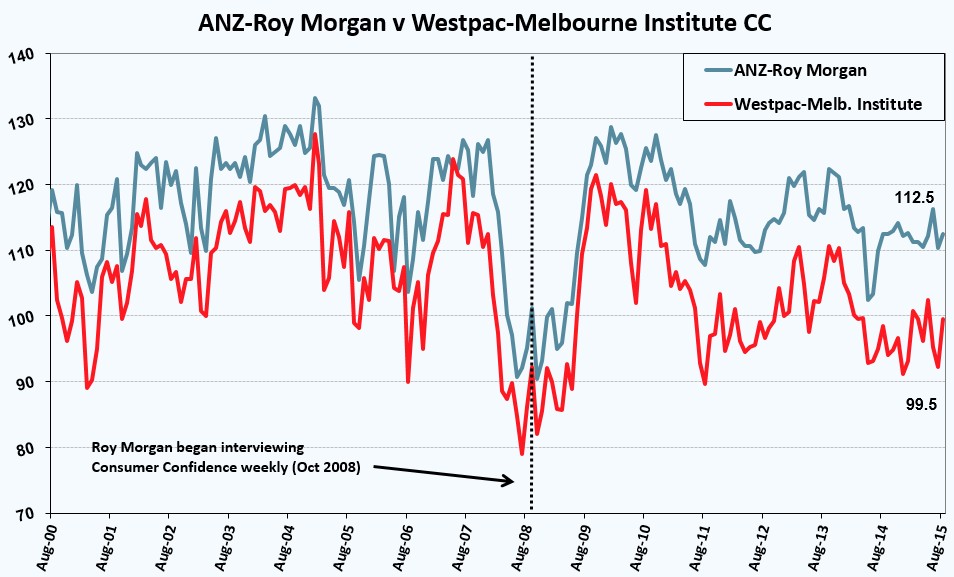

And below is a comparison of the Westpac-Melbourne Institute consumer sentiment index against the ANZ-Roy Morgan Research’s latest consumer confidence figures: