A Greek debt default and exit from the Euro have been averted, while the rout of the Chinese stock market continues. There exist little new domestic data to guide the Reserve Bank this month. Official inflation equals 1.5%, well below the RBA’s target band.

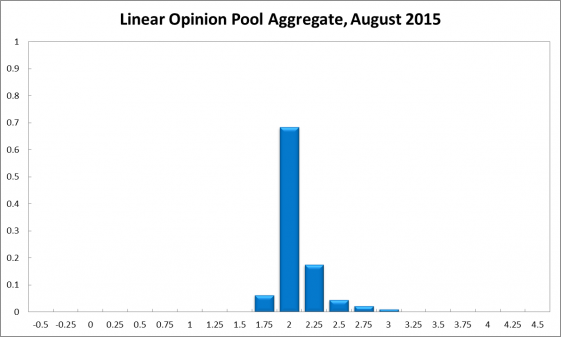

The CAMA RBA Shadow Board on balance prefers to hold firm. It attaches only a small probability to the need for a rate cut. In particular, the Shadow Board recommends the cash rate be held at its current level of 2%; it attaches a 68% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 6%, down 2% from the previous month, while the confidence in a required rate hike has fallen to 25%. Australia’s jobless rate, according to the Australian Bureau of Statistics, remains at 6%.

No new data has been released on wage growth, which recently has been at a record low of 2.3% per quarter. After hovering around the 76 US¢ mark, the Aussie dollar has fallen some 3 US¢. Yields on Australian 10-year government bonds have fallen slightly from the previous month, to under 3%. The number of home loan approvals, excluding refinancing, fell by 8.2% in May, its largest monthly decline in 15 years. Along with a fall in the value of investor activity of 3.2% in the same month, these numbers point to a possible cooling of the Australian property market. The S&P/ASX 200 stock market index rebounded slightly from its recent decline. High real estate prices remain a concern for many Shadow Board members and are often cited for a reason not to cut the cash rate any further.

Overseas, debt default and Greek exit from the Euro have been averted at the eleventh hour, while the Chinese stock market experienced a major correction from its lofty heights. The uncertainties surrounding the Chinese economy pose the biggest immediate threat to Australia’s export markets and thus to Australia’s GDP.

In a recent speech, Federal Reserve Bank Board Governor Janet Yellen has indicated that an increase in the federal funds rate is imminent, reflecting the solid expansion underway of the US economy.

Commodity prices, in particular crude oil, have fallen to new lows. The Westpac/Melbourne Institute Consumer Sentiment Index fell yet again from 95.3 in June to 92.3 in July. No other new data on consumer and producer confidence has been released since the last round.

Still unable to utter the words “macro prudential”. Given the tightening underway I’m not sure how it can render judgements without them. That’s not to say the RBA should or will cut tomorrow, it’s a guaranteed hold.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.