Credit Suisse strategists stick to their bullish view on Aussie equities due to their solid free cash flow growth and an accommodative cost of debt.

They predict interest rate cuts in China – which happened overnight – Thailand, Indonesia, New Zealand, and Australia, and no Fed rate hike until December.

They add that the recent sell-off in Aussie equities was the sixth largest since the early 1990’s and makes the market looks reasonably priced on P/Es and dividend yields.

They also note that one of the sharpest drawdowns in global investor risk appetites hasn’t resulted in a meaningful rise in Australian corporate bond yields.

Additionally, they say the recent capital market moves suggest Aussie Industrial companies can now generate 0.6% accretion from each 1% buyback – the highest in over 20 years.

That might work as argument for BTFD (buying the fucken dip) in the very short term. Such can kicking is certain.

However, what you ought to ask yourself is does it make any sense in a slightly larger context. Will those rate cuts be meaningful to Australian, Indonesian, Thai and Kiwi profits? Very likely not as all will be overwhelmed by capital outflow, weak external demand and falling terms of trade (rising for the manufacturers). That is especially the case if the Fed hikes at all, let alone as soon as December. If the Fed itself turns dovish then maybe we’ve got a little longer in the cycle but as discussed this morning that is at serious risk of coming too late as well.

Advertisement

The CS argument is really only an appeal to more financial repression which is why it swings almost entirely upon the last point, the hope of roping firms into the same ponzi party.

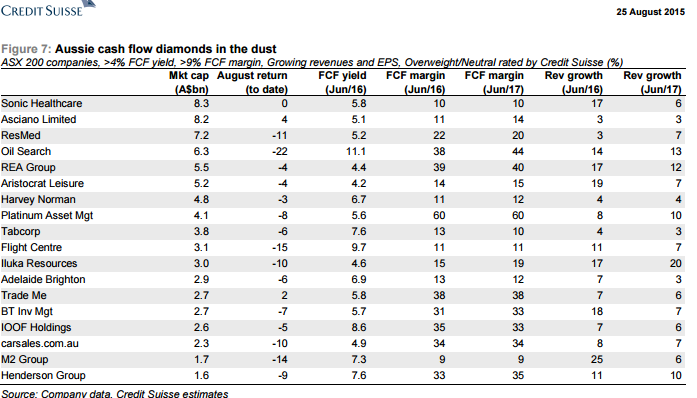

The CS list is alright with its smattering of dollar-exposed industrials but if the macro-economic settings deteriorates as expected (not in a hurry necessarily) then they are all going to fall too.

This is not a time to be grabbing at falling knives. It is a time to be setting shorts on any rally and preparing your war chest for worse to come.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.