By Chris Becker

A quiet night on Friday across both sides of the Atlantic as US industrial production printed stronger than expected, boosting interest rate expectations again as the Chinese PBOC continued to sooth market concerns about the Yuans depreciation. Slightly weaker than expected second quarter GDP results for Germany and Europe didn’t phase the markets either with just a small bond selloff the result. European stocks finished their cash sessions slightly in the red, while US stocks lifted lightly as the commodity selloff had a breather.

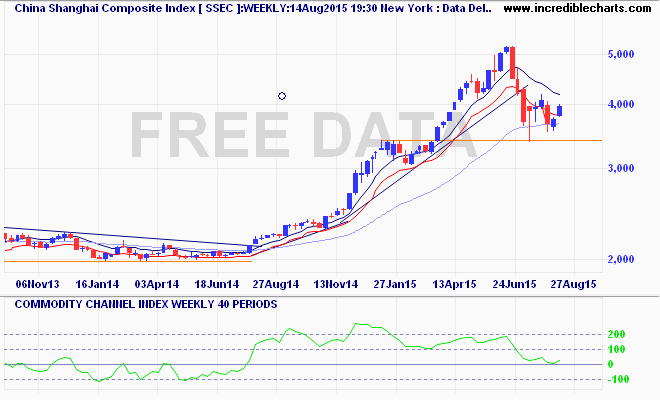

As usual for Monday, we’ll take a longer view of most markets to start the week, starting with the Shanghai Composite. The mainland Chinese bourse lifted a few points on Friday, but still remain below 4000 points as its sideways move on the weekly charts still points to a deflation down to support at 3400 points over the long run. We might see a small upmove to 4000 this week: