With the June quarter national accounts due for release on Wednesday, Westpac’s Andrew Hanlan looks at the factors likely to impact the result. Westpac is forecasting a subdued 0.4%QoQ, 2.2%YoY growth in real GDP, but with flat to falling nominal GDP in June and falling national income due to lower commodity prices (lower terms-of-trade):

The Australian National Accounts, to be released on Wednesday September 2, will provide an estimate of economic activity for the June quarter.

The economy expanded by a forecast 0.4% in Q2. This follows a surprisingly strong 0.9% gain in Q1. Annual output growth rounds down to a subdued 2.2%, from 2.3% in March.

Exports are the key swing factor over the first half of 2015, with a 5% surge in the opening months of the year – in part due to fewer weather disruptions than normal – partially reversed in Q2, down 2.5%. Net exports added 0.5ppts in Q1 but subtracted an estimated 0.4ppts in Q2.

An income squeeze remains a key dynamic. Commodity prices have tumbled as global commodity supply expands and China’s economy slows. Australia’s terms of trade is down sharply as a result, declining by an estimated 4.3% in the quarter, following a 3% drop in Q1, to be 17% lower than at the end of 2013. Incomes of business, households and government remain under pressure, constraining spending power.

Nominal GDP, crunched by the sharply lower terms of trade, could well be flat to down a fraction in the June quarter. Our forecast is for –0.1%qtr, 0.9%yr. Historically, annual nominal GDP growth has averaged around 5.8%.

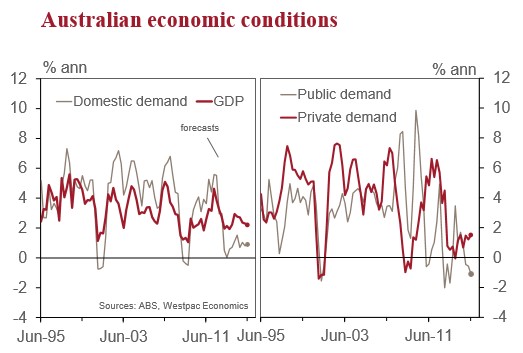

Domestic demand is forecast to rise by 0.7% in Q2, having stalled in Q1. However, this is a little misleading. A late cycle burst of work on mining projects in WA will see infrastructure activity add 0.5ppts to domestic demand.

More generally, key domestic headwinds in 2015 are public demand, associated with budget pressures, and business investment, as mining investment trends lower from record highs. For Q2, public demand is expected to be flat but business investment stages a one-off bounce of 3%, having fallen for the past six quarters.

A key positive is the housing sector, responding to low and falling interest rates. Having said, in the June quarter, home building activity dipped, down an estimated 2.0%.

The consumer is both a key interest and a key uncertainty. We are looking to the national accounts to provide a clearer picture of spending and incomes. We anticipate a lukewarm quarter for consumer spending, +0.6%. Wages growth has been weak and the household saving ratio, while lower than a year ago, remains relatively high.

The labour market made solid gains, with employment up 0.7% in the quarter, matching the Q1 result. Hours worked however rose by only 0.2%, following a 1.6% jump in Q1. We look to the Business Indicators survey on Monday for an estimate of wage incomes. A key dynamic is that average wages per hour are falling as higher paid jobs are replaced with lower paying ones.

Household consumption (0.6%): Consumer spending remains modest, up a forecast 0.6% in the quarter, following a 0.5% gain in Q1. Annual growth is lacklustre at 2.5%. Real retail sales grew by 0.8%, up a fraction from a 0.7% rise in Q1, led higher by household goods associated with the home building boom. However, vehicle sales stalled, after a modest gain early in the year. Private business surveys suggest that the consumer sectors experienced stronger sales in the second quarter.

Dwelling investment (–2.0%): Home building is in the midst of a strong upswing as approvals hit fresh record highs early in 2015, supported by record low interest rates, pent-up demand and strong interest from investors. Despite this, new home building activity dipped 3.6% in the quarter, following strong gains over the past half year. Renovation work is trending modestly higher.

New business investment (3%): Business investment managed a one-off bounce, breaking a six quarter run of declines. Infrastructure activity jumped 10% on a 35% spike in WA as construction companies rushed to make up for lost time with a view to avoiding penalties. Commercial building was flat, as the cycle is about to enter a modest downturn. Equipment investment contracted by 1.2%, with weakness in mining and manufacturing offsetting a lift in spending by the service sectors.

Public spending (flat): Public demand has stalled, with weakness in investment. Public construction work fell a further 8% in the quarter.

Net exports (–0.4ppts): A negative in Q2 as exports dipped, down 2.5%, partially reversing a 5% surge in Q1.

Private non-farm inventories (+0.5%, 0.0ppt contribution): Inventory levels, which are rising modesty to meet a lift in household demand, are expected to be neutral for growth in Q2.

The Business Indicators survey (Mon), the Balance of Payments (Tue) and Public Demand data (Tue) will provide further clues as to the risks surrounding our forecast for GDP (published Wed).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.