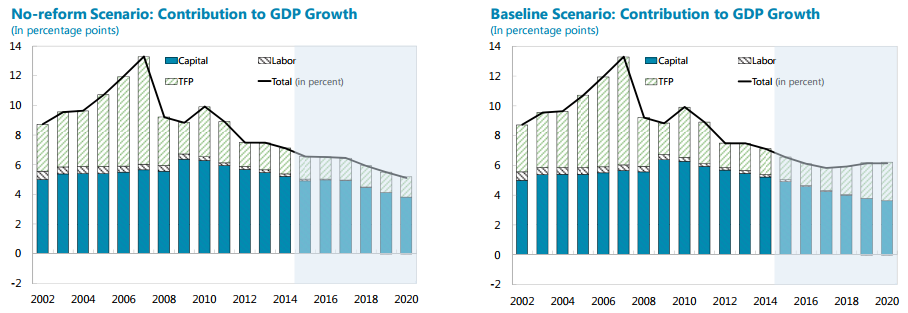

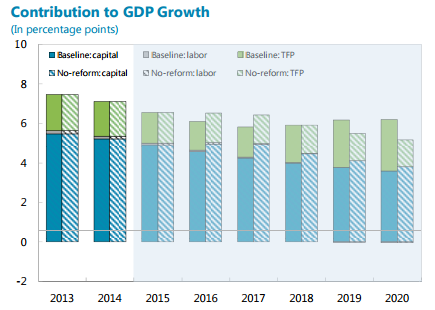

Implementation of the authorities’ reform agenda is critical for boosting potential growth. Without reforms, vulnerabilities would continue to rise. On the supply side, there would be strong headwinds from falling productivity and negative labor force dynamics. On the demand side, the dynamics of credit and investment would be unsustainable due to a combination of rising interest costs in the highly indebted corporate sector and local governments, and falling returns on investment. This would increase the risk of a sharp or protracted growth slowdown over the medium term, even though policy buffers limit risks in the near term. On the other hand, the implementation of the authorities’ reform program would lead to an initially slower, but ultimately more robust and higher growth.

Without reforms, growth would gradually fall to around 5 percent in 2020, with steeply increasing debt ratios. A no-reform scenario is constructed that assumes the authorities attempt to stabilize growth at around 7 percent. This strategy would eventually fail, as growth would slow as the marginal product of capital falls and productivity growth stagnates.

With respect to the IMF, such country assessments have a strong political dimension as local authorities define inputs into the report. As such the IMF is working within the official Chinese data set which inflates all figures. In fact, China is already growing at more like 5% not 7%. Thus, given the IMF narrative makes perfect sense, to understand the impact of what it is describing for growth and commodity prices in the future, you need simply to shift the baseline down by 2%.

Officially the IMF is already looking for 6.3% growth in China next year but that translates to 4.3% in reality and by 2020 it is 3% in the no reform scenario versus 4% in the reform scenario. That’s exactly what MB is looking for.

Advertisement

It really doesn’t matter which way you cut it, Chinese growth is going to fall. Either by accident or by design. And its constituents parts will also shift significantly away from the capital intensity which drives commodity consumption:

Note that Australia is actually worse off in the event that China succeeds in rebooting productivity based growth, as has been the case since 2011. What is good for China is now bad for Australia.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.