The Reserve Bank of Australia’s (RBA) Statement on Monetary Policy, released on Friday, provided an interesting analysis of Australian household debt, which found that debt levels aren’t as bad as commonly thought due to the prevalence of offset accounts; although rising education debts are having an adverse impact:

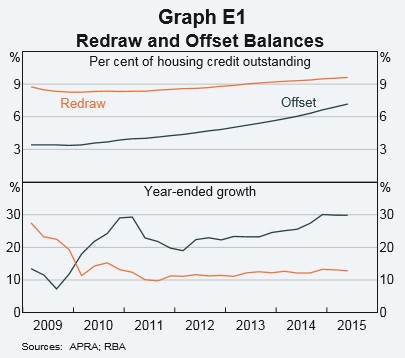

Since offset account balances have been growing by around 30 per cent annually over recent years, annual growth in net housing debt, which takes into account offset accounts, is about 6 per cent. This compares with annual growth in housing credit of around 7 per cent…

This growth has the potential to continue as older loans that are less likely to have offset accounts are replaced with new loans, where it is more common to have an offset account. Available redraw balances, at around $120 billion, are larger than offset account balances, but have grown at a pace closer to 10 per cent over recent years…

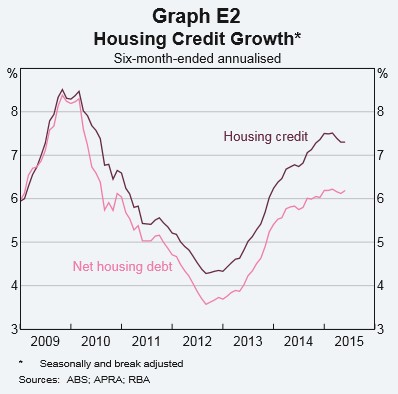

Since offset account balances have been growing much more rapidly than housing credit, net housing debt is growing more slowly than housing credit; over the six months to June, annualised net housing debt growth was around 6 per cent, compared to 7 per cent for housing credit growth (Graph E2).

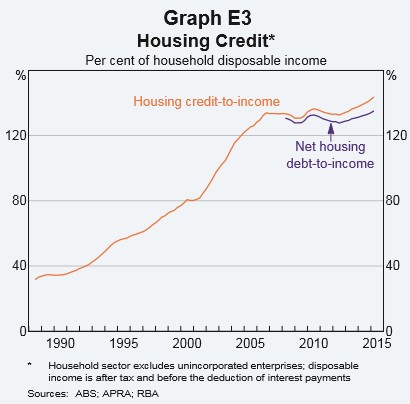

The treatment of offset account balances also has implications for measuring the household debt-to-income ratio… Without adjusting the stock of outstanding housing credit for offset account balances, housing debt as a share of household disposable income has been increasing since mid 2012 to be at a historical high of 144 per cent (Graph E3). Adjusting for offset account balances suggests that this ratio has been rising at a slower pace, and has only just surpassed its most recent peak in late 2010.

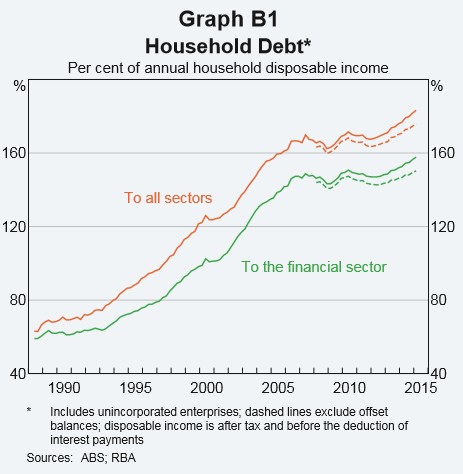

Over the past few years, however, household debt to the non-financial sector has grown more rapidly (Graph B1). This has largely been caused by debt owed to the government sector and the rest of the world growing at a faster rate than debt to the financial sector. These trends have been driven by an increase in the number of government-funded university places for Australian students and a high level of net overseas migration in recent years.

A comprehensive measure of household debt should also be net of balances in offset accounts because they effectively reduce the household sector’s net debt position… Since offset account balances have been growing faster than housing debt, this netting reduces the increase in the household debt-to-income ratio somewhat, but not by enough to offset the growth in debt to the government and to the rest of the world. Overall, all measures point to a moderate increase in household debt relative to income in recent years.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.