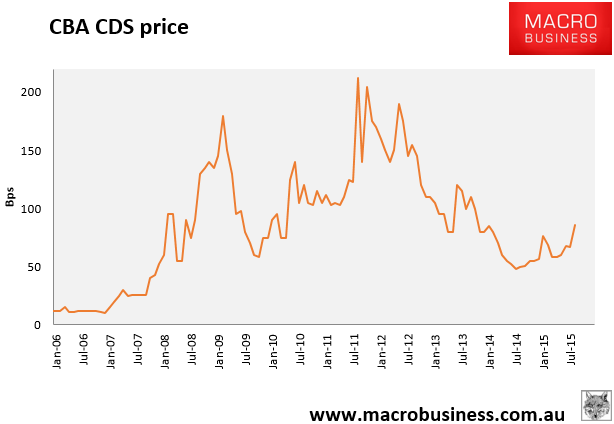

And so it goes with CBA 5 year CDS launching yesterday 10% to 86bps:

CDS is good proxy for the price that banks must pay to issue bonds, which contributes roughly one third of their liability funding.

That move through 2014 now looks like a long rounded bottom with the January spike forming a handle. In technical analysis, the “cup and handle” formation is very bullish.

Advertisement

We have to see spreads get to about 120bps before non-bank lenders start to get priced out. Banks themselves enter the pain zone anywhere above 150bps.

But in the mean time margins get squeezed and that means repricing loans either via higher rates or holding back cash rate cuts.