Just as I was hoping that a day would pass without needing to write another ‘take-down’ article on property tax concessions, possibly the worst ever (and that’s saying something) defence of negative gearing was published over the weekend in Fairfax’s Domain, penned by Jamie Alcock, an Associate Professor of Finance at the University of Sydney Business School.

In the article, Alcock presents five so-called “myths” about negative gearing, and provides flimsy arguments in a bid to debunk them. Let’s take a look.

Myth 1: Negative gearing is responsible for the recent house price surges in Sydney and Melbourne.

Negative gearing rules have been in place for more than a quarter of a century and the number of investors taking advantage of them has been stable for well over a decade. The recent price rises are more closely related to supply restrictions and falling interest rates.

Any examination of Australia’s negative gearing rules needs to be considered in tandem with its partner in crime, the 50% capital gains tax (CGT) discount, which was implemented in 1999.

Advertisement

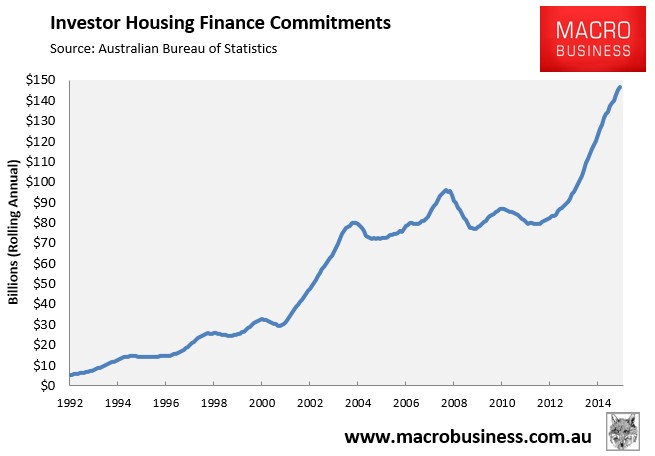

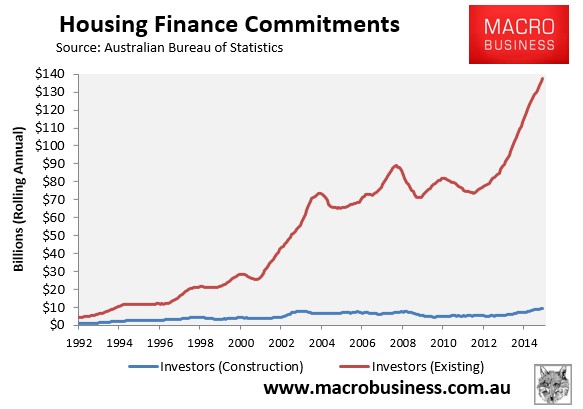

The evidence clearly shows that loans to housing investors surged since the CGT discount was first implemented, as well as recently:

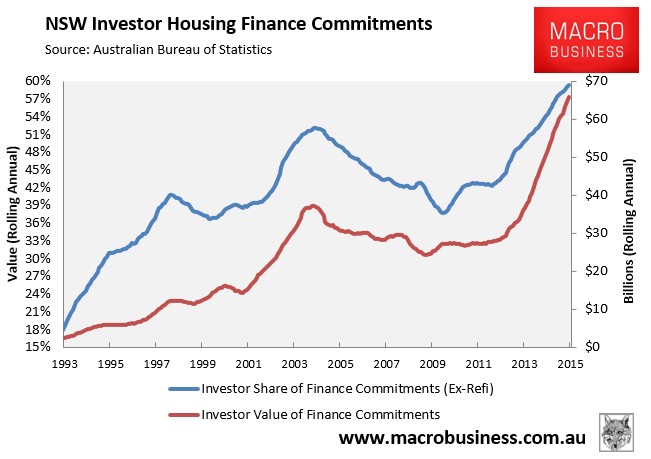

With the greatest impact in New South Wales (read Sydney):

Advertisement

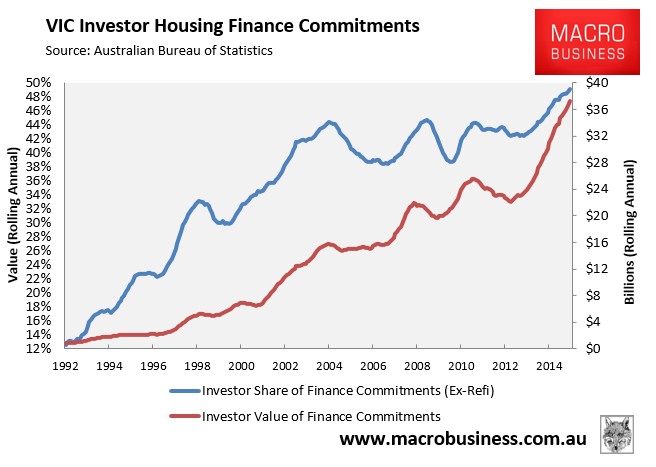

And Victoria (read Melbourne):

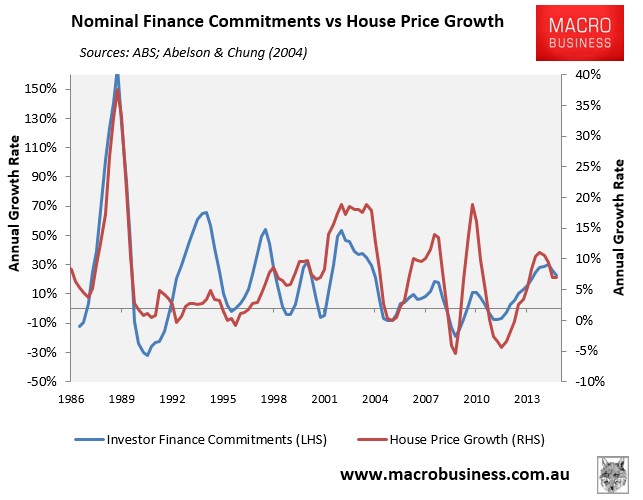

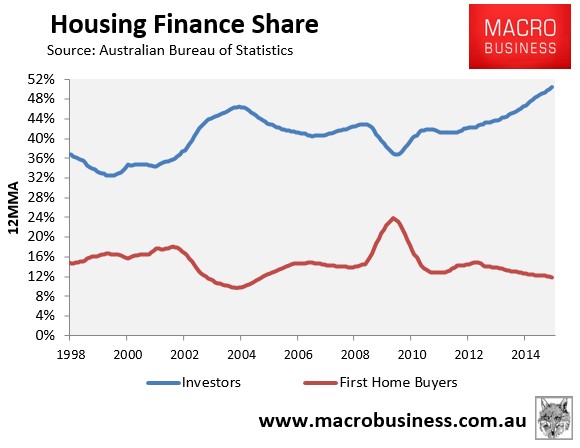

Moreover, the correlation between increased investor demand and rising house prices is clear as day, particularly after negative gearing was reintroduced in the late-1980s, after the CGT discount was introduced in 1999, and currently:

Advertisement

Back to Alcock:

Myth 2: Negative gearing makes property unduly attractive for investors.

All investments, including property, can be negatively geared. Property competes, as an investment, on a level playing field. Abolishing the negative gearing rules for property would cause a market distortion, not cure it.

“Level playing field”? As noted in the RBA’s submission to the House of Representative’s Inquiry into Home Ownership [my emphasis]:

Advertisement

…the interaction of negative gearing with other parts of the taxation system may have the effect of encouraging leveraged investment in property. In particular, the switch in 1999 from calculating CGT at the full marginal rate on the real gain to calculating it as half the taxpayer’s marginal rate on the nominal gain resulted in capital gain-‐producing assets being more attractive than income-‐producing assets for some combinations of tax rates, gross returns and inflation. This effect is amplified if the asset can be purchased with leverage, because the interest deductions are calculated at the full marginal rate while the subsequent capital gains are taxed at half the marginal rate. Since property can usually be purchased using higher leverage than other assets that produce capital gains, property is especially affected by this feature of the tax system.

Moreover, try and get a loan for negative gearing of anything other than property and see how far you get.

With regards to creating a “market distortion”, allowing investors to offset investment losses against unrelated wage/salary income and then allowing them to pay half the rate of CGT is a market distortion. It was also acknowledged as such by former Treasurer, Paul Keating, whose 1987 cabinet submission on negative gearing classified it as a “generally recognised tax shelter”:

Advertisement

The negative gearing measure was introduced [in 1985] to partially close-off a generally recognised tax shelter, a rationale which remains broadly valid…

The three basic features of a typical tax shelter are the absence of a full nominal capital gains tax, the deductibility of full nominal interest expenses, and the mis-match in the timing of the deductions and the recognition of taxable income (for example, because capital tax is payable on a realisations rather than accrual basis).

Rental property investment clearly exhibits each of these features, as do some other activities, and so effectively obtains tax benefits under the current tax system.

Back to Alcock:

Myth 3: Negative gearing pushes aggregate prices out of the reach of average Australians.

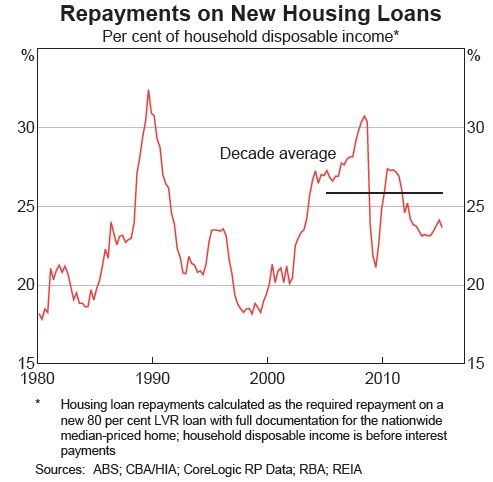

There is simply no evidence that prices are skewed out of the range of the average Australian. The RBA made this clear to the Senate inquiry – the current cost of servicing new loans on housing in Australia is significantly lower than the average over the past decade.

Rubbish. According to the RBA, initial costs on servicing a typical mortgage are below the decade average:

Advertisement

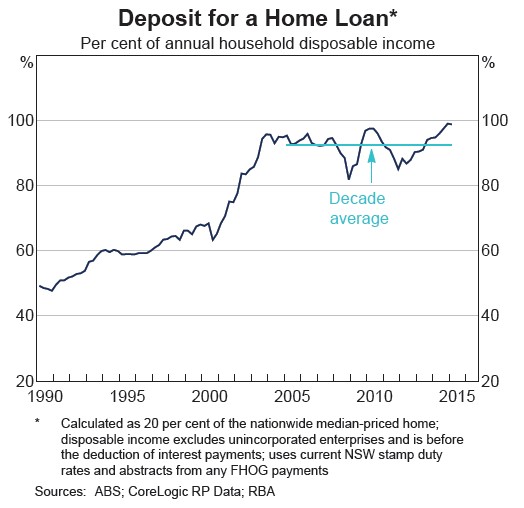

But the deposit required is at its highest ever level:

Advertisement

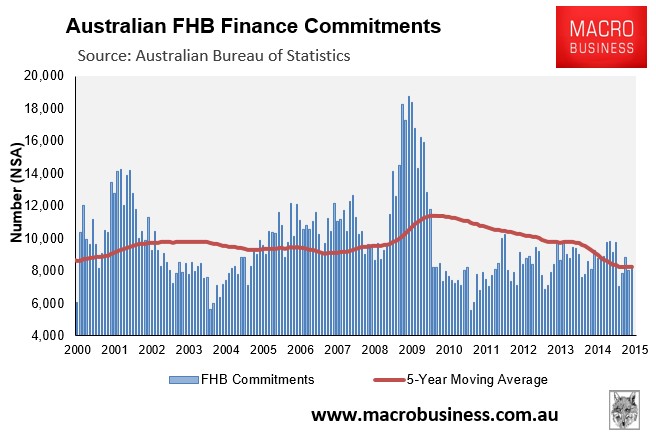

Which helps to explain why owner-occupier first home buyer demand is near its lowest ever level, despite record low nominal mortgage rates:

Back to Alcock:

Advertisement

Myth 4: Negative gearing benefits the wealthy at the expense of the poor.

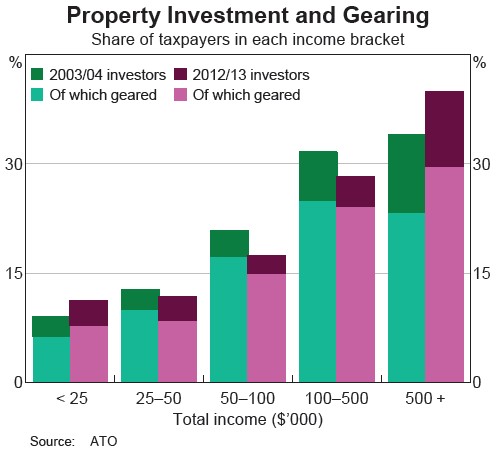

Taxation statistics from the ATO show that of those declaring a net rental interest in recent years; approximately three-quarters earn less than $80,000 per annum.

Alcock has confused gross income with taxable income as reduced by negative gearing. The RBA’s submission to the House of Representative’s Inquiry into Home Ownership clearly debunked his argument:

Tax data also show that the incidence of property investment and the incidence of geared property investment… increase with income…

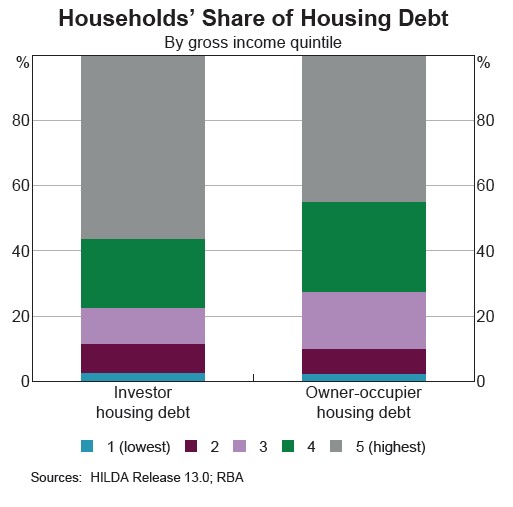

While the incidence of property investment increases with the level of income, the Household, Income and Labour Dynamics in Australia (HILDA) Survey also suggests that most investor households are in the top two income quintiles. These households hold nearly 80 per cent of all investor housing debt…

That’s right, the top 40% of income earners hold nearly 80% of all investor mortgage debt, according to the RBA.

Advertisement

Back to Alcock:

Myth 5: Negative gearing rules make it more difficult for first home-buyers to enter the housing market.

This is one of the most contentious myths in the popular mindset. The reality is that by encouraging investment in housing, the supply of rentals increases which keeps rents low. For example, in inner-Sydney gross rental yields can be as low as 2.5 per cent in some areas. This benefits the renter, not the investor, and allows renters a better opportunity to save for a deposit for their own home. Abolishing negative gearing would, in the long-term, drive rents up and make it much harder for renters to get on the property ladder.

Unbelievable. No mention of the fact that nearly 95% of property investors are buying established dwellings, thus they are not adding to housing supply and are merely substituting homes for sale into homes for let:

Advertisement

Hence, negative gearing and the CGT discount are not lowering rents, but rather helping to push house prices up. And this increased demand from investors is clearly crowding-out first home buyers:

But wait, there’s more. Alcock has also tried to debunk the claim that negative gearing did not push up rents when it was abolished between 1985 and 1987:

Advertisement

Some commentators have suggested that rents did not increase during the 1985 negative gearing hiatus. However, housing markets are sluggish to respond to demand shocks. Building new property to address market undersupply or waiting for population growth to absorb oversupply takes many years. Also most leases are fixed for a significant length of time. Observations made in a single year do not disprove fundamental economic principles.

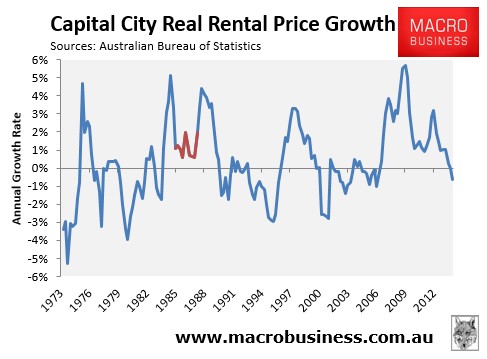

This is desperate stuff. The data clearly shows there was no effect on rents nationally (see red below). Moreover, the highest ever real rental growth was recorded in the late 2000s when both negative gearing and the CGT discount were in effect:

Advertisement

What does this tell you about negative gearing’s rent lowering capabilities?

The 1987 Cabinet Submission on negative gearing also noted that real rents fell across six out of eight jurisdictions in the year to March 1987, which was around 20 months after negative gearing was first ‘abolished’:

“Data for individual capital cities suggest that, as might be expected, rents have risen more rapidly in those cities where vacancy rates have been tightest. In the twelve months to March quarter 1987, rent increases in six of the eight capitals lagged the CPI“.

Advertisement

In any event, if Alcock is so worried about supply, then why not argue to limit negative gearing to new builds, as has occurred with the first home buyers grant?

Alcock also makes the ridiculous argument that unwinding negative gearing would destroy wealth and lead to unfair transfers:

Even if the opponents of negative gearing are correct, and abolition did reduce house prices, how much wealth would be destroyed? A 10 per cent reduction in average house value equates to a $570 billion wealth destruction. This is people’s life savings and retirement plans, and it would hurt those currently with mortgages most heavily. Destroying wealth in one sector of the community to increase wealth in another is simply a wealth transfer form one group to another.

Similarly, making changes to tax rules that hurt the entire country simply to help a select few in Sydney and Melbourne is a wealth transfer from the regional areas to the city.

Advertisement

So higher house prices = good, but lower house prices = bad?

If it is not acceptable to transfer wealth from property owners to prospective buyers, why is the reverse acceptable? And what are high prices in Sydney and Melbourne if not a wealth transfer from the country to the city?

Also, Alcock seems to have no concept of productivity. That is, channeling capital into unproductive housing necessarily starves the productive economy of funding, whilst pushing up land costs, which also chokes-out the productive economy.

Advertisement

Back to Alcock:

The reality is that abolishing negative gearing on property would create a market distortion, make it more difficult for future first-home buyers to save a deposit, increase rents and create significant wealth destruction and transfers.

“Create a market distortion”. No, it would unwind a market distortion and recognised tax shelter.

“Make it more difficult for future first-home buyers to save a deposit”. No, it would make it easier, since home prices would be lower and rents would be unaffected.

Advertisement

“Increase rents and create significant wealth destruction and transfers”. No, rents would be unaffected, since negative gearing does not add to supply. Moreover, homes would become more affordable. What’s wrong with that? Should Australia really aim to have the most expensive housing in the world?

Alcock then concludes with the following dross (my emphasis):

If the government is serious about improving housing affordability, then it should explore options to increase supply and reduce the cost of inputs. Some suggestions include removing stamp duties, simplify and relax the complex planning system, reduce social housing, tighten trade-union legislation and increase urban infrastructure coverage.

I agree with the supply-side stuff. But how exactly would reducing social housing improve housing supply?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.