The negative gearing ‘whack-a-mole’ continues today, with the following false claims from Minister for Social Services, Scott Morrison, who said the following in a speech yesterday to the Institute of Public Affairs:

For those seeking to buy their own home, the price has more than doubled the increase in wages over the past 25 years. More than 30% of family income is now required to meet median loan repayments, breaching a commonly accepted housing affordability threshold. The ratio of owner occupied housing debt to disposable income is now more than 90%, up from 55% in December 2000.

The supply of housing is simply not keeping up with demand. While record low interest rates is extending credit to more home purchasers, the lack of stock is forcing up prices.

Fortunately for renters, wages and rents have moved largely at a similar pace to wages and rents as a proportion of gross household income remain well below the 30% affordability threshold.

In Australia, private rental accommodation is supported by a large pool of mum and dad investors making private rental stock available, through negative gearing. By number, almost 80% of these investors are middle income Australians earning $80,000 a year or less, owning just one property. They are school teachers, police officers, nurses and office workers saving and investing to provide for their financial security. In the Europe and the US, it is large institutional investors who often play this role. They are absent from our housing market.

Let’s dissect Morrison’s comments.

Advertisement

First, the “supply of housing is simply not keeping up with demand” and “the lack of stock is forcing up prices”.

If this is the case, where is the sense in juicing housing demand via generous tax settings like negative gearing and the 50% capital gains tax (CGT) discount?

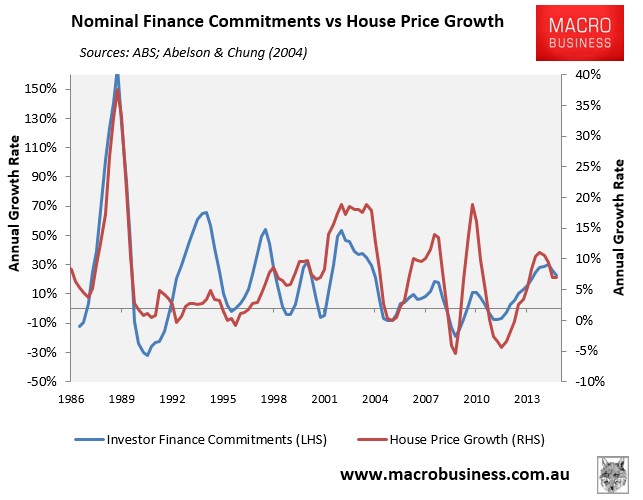

The correlation between increased investor demand and rising house prices is clear as day, particularly after negative gearing was reintroduced in the late-1980s, after the CGT discount was introduced in 1999, and currently:

Advertisement

What about Morrison’s claim that “private rental accommodation is supported by a large pool of mum and dad investors making private rental stock available, through negative gearing”?

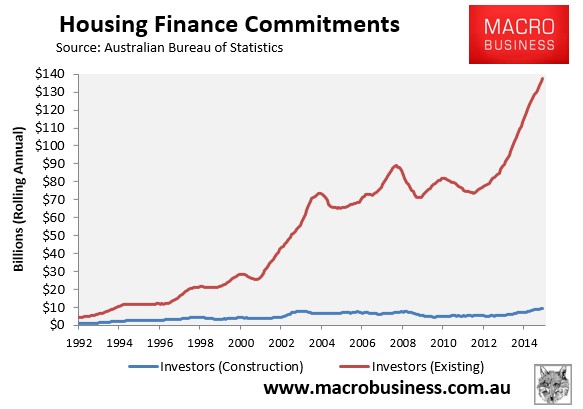

The data clearly shows that nearly 95% of investor mortgages are for existing dwellings, not new construction:

Advertisement

Hence, negative gearing and the CGT discount are clearly not adding to housing supply and are merely substituting homes for sale into homes for let.

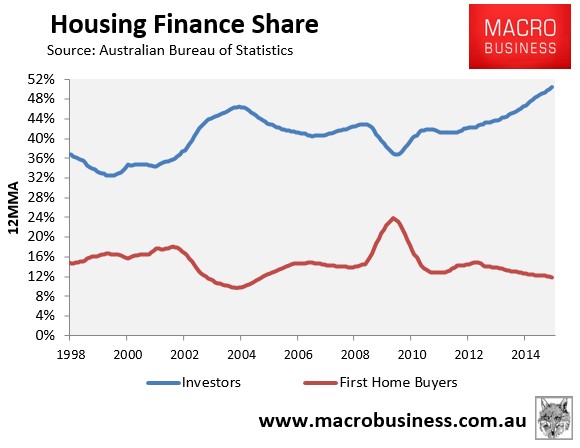

Negative gearing and the CGT discount, therefore, are not lowering rents, but rather helping to push house prices up. And this increased demand from investors is clearly crowding-out first home buyers seeking a home for owner occupation:

Advertisement

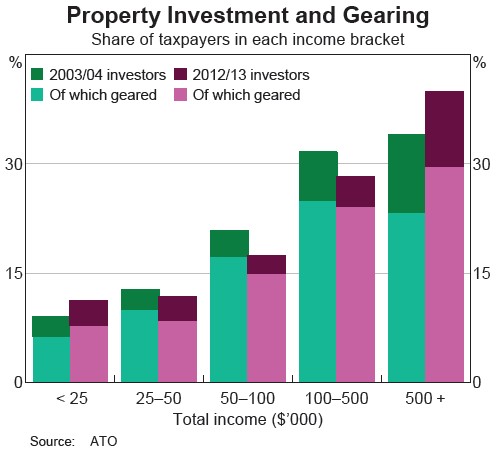

Finally, Morrison’s claim that “almost 80% of these investors are middle income Australians earning $80,000 a year or less, owning just one property” is clearly false.

Morrison has conflated gross income with taxable income as reduced by negative gearing. Average taxable income, according to the ATO’s latest taxation statistics, is only around $55,000, almost 50% below the $80,000 threshold identified by Morrison. Hence, someone earning $80,000 in taxable income is a relatively high income earner, not a so-called “middle income Australian”.

More importantly, the RBA’s submission to the House of Representative’s Inquiry into Home Ownership clearly debunked Morrison’s argument:

Advertisement

Tax data also show that the incidence of property investment and the incidence of geared property investment… increase with income…

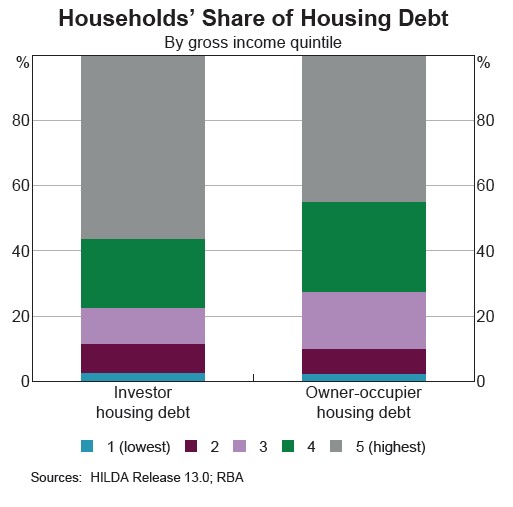

While the incidence of property investment increases with the level of income, the Household, Income and Labour Dynamics in Australia (HILDA) Survey also suggests that most investor households are in the top two income quintiles. These households hold nearly 80 per cent of all investor housing debt…

So, the top 40% of income earners hold nearly 80% of all investor mortgage debt, according to the RBA.

The negative gearing lies continue from the Abbott Government.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.