Today’s housing finance data for May, released by the Australian Bureau of Statistics (ABS), revealed sharp falls in both owner-occupied and investor finance commitments.

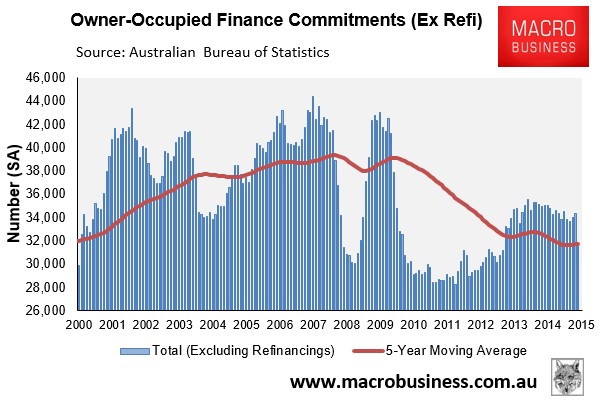

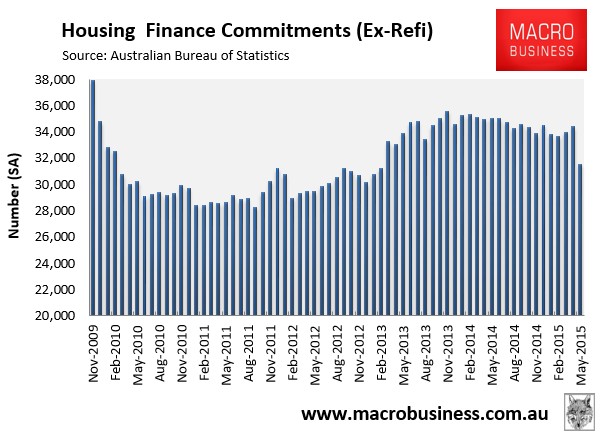

According to the ABS, owner-occupier finance commitments (excluding refinancings) tanked by a seasonally adjusted 8.2% over the month and were down by 10.0% over the year (see below charts).

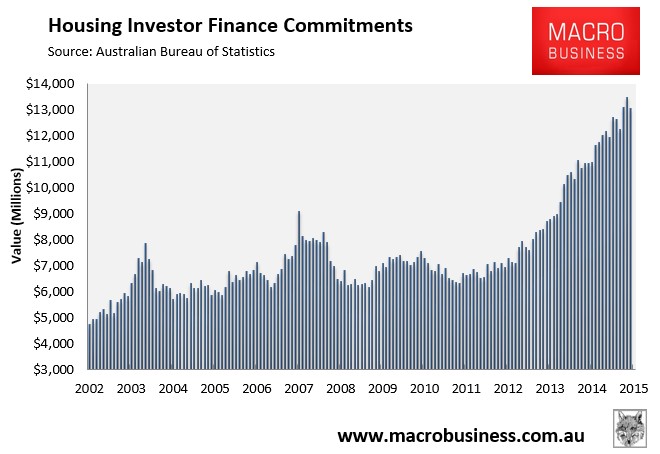

The value of investor finance commitments also fell by 3.2% in May, but were up by 19.4% over the year (see next chart).

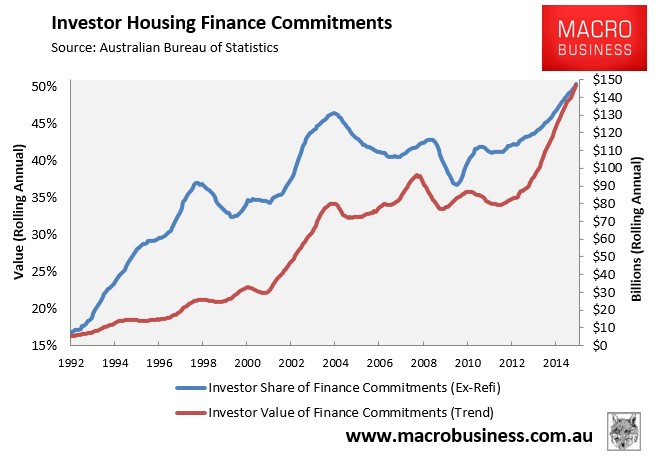

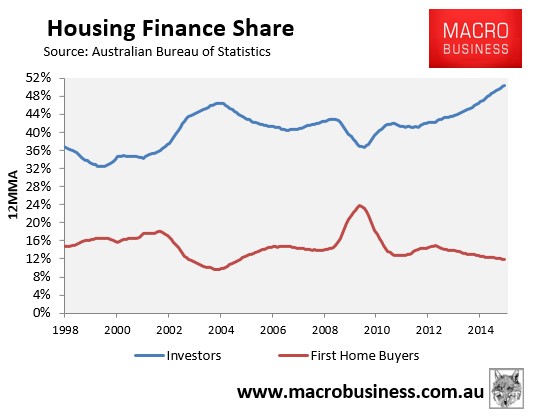

Nevertheless, investors accounted for a record 50.4% of total finance commitments (excluding refinancings) in the year to May 2015:

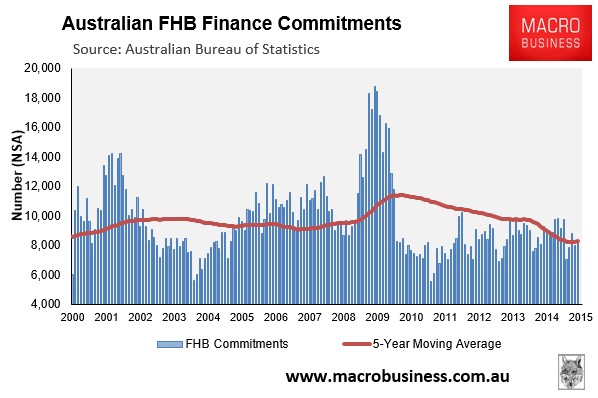

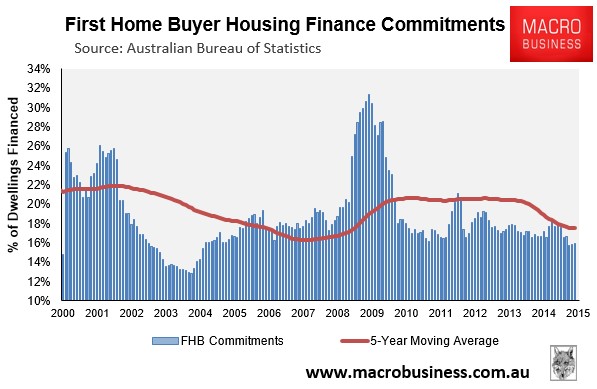

Meanwhile, first home buyer (FHB) demand remained tepid in May, rising to just 15.9% of total finance commitments despite falling by 10.2% over the year (see below charts).

The comparison of the share of investor and FHB commitments is stark, with a near inverse correlation present, suggesting that investors are locking young Australians out of home ownership:

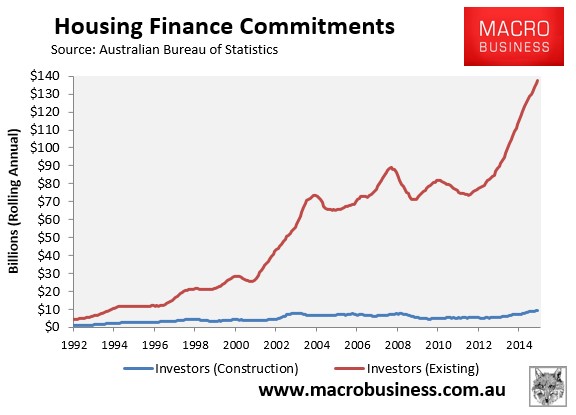

Despite the lies from the property lobby that investors are adding to housing supply, they remain primarily interested in hoovering up existing homes:

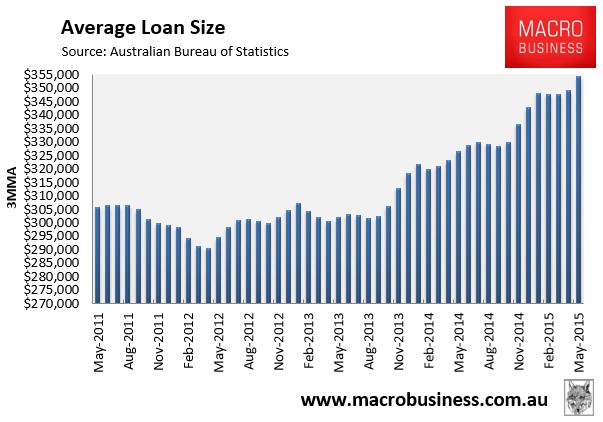

Meanwhile, the average loan size was flat in May but was up 10.1% over the year, and has moved upwards again on a 3-month moving average basis:

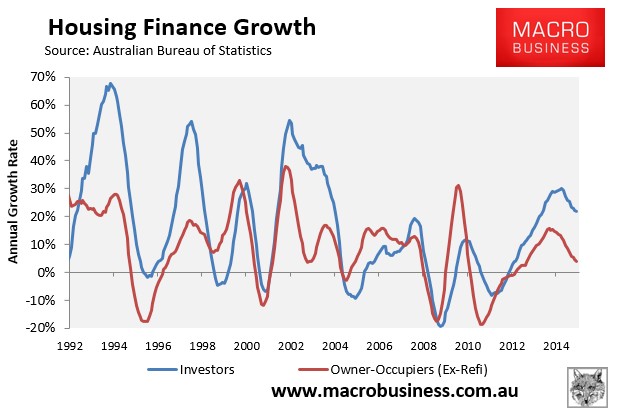

Finally, those banking on continued strong house price growth might get a shock from the next chart showing both owner-occupier and investor mortgage growth falling:

House prices tend to follow finance commitments, suggesting national house price growth should soon start to fall.