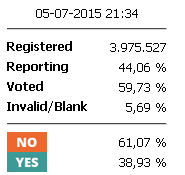

With 60% of the Greek referendum vote counted it appears to be over:

Who could have known that a sovereign people would tell a foreign power with whom they were previously at war to shove their blackmail demands?

Here is Deutsche with where we go from here:

NO, Scenario #N1. Soft deal

This, in our view, is by far the least likely outcome, as it would generate significant moral hazard issues, which in the longer term could be as damaging as an exit. If Europe were to offer significant concessions to Greece following a no vote, it would de facto incentivize other borrowing countries to call domestic referenda to improve the terms of their rescue packages. This would be unsustainable in the long-run as (a) it would create obvious political issues in creditor countries, (b) it would not deal with the structural adjustments and political integration which are necessary for the longer term viability of the euro area.

NO, Scenario #N2. Default-and-stay

A direct recapitalization of the Greek banks is more likely, we think, than a very soft programme, but would be a challenge for Greece and, above all, euro-area partners to accept.

From the European perspective, it could be the start of a new round of financial commitments, all the more so unless there is a strong, credible agreement on structural reform to boost growth and protect Europe’s capital investment. After a default, getting the necessary consensus for such a bank-based deal will be difficult. Indeed, a public default would likely lead to a cascade of private defaults — starting with corporates.

The most serious flaw with this scenario is the moral hazard it creates. If Europe facilitates this default-and-stay option in Greece, it opens the door across the periphery to similar demands. If it is easy to renege on debts but have Europe preserve your banking system and access to the single currency, others will want the same. It will promote instability.

It is not only a question of ex-post moral hazard either. There are general elections in Spain at the end of the year and in Ireland by April 2016. How could the governments of these countries explain to their electorates that they should help to shoulder the direct recap of Greek banks after their own public debt ballooned because of the recap of domestic banks?

From Greece’s perspective, the cost of direct recapitalization in terms of deposit bail-in and general economic conditionality (see Box 1) means this scenario is not a shoe-in either.

It is also a scenario that needs time, measured in months, to come to technical fruition. In the meantime, the economic and political cost of a closed banking system will be mounting. There is a considerable probability if Greece and Europe go down this route that it merges into Scenario N3.

An additional consideration is that the HFSF is a guarantor to the EFSF. In the event of a Greek default, the EFSF may have a direct claim on the HFSF shares in the Greek banks. If Europe becomes the beneficial owner of the Greek banking system, the argument for direct recapitalization could grow. This does not diminish the technical and political complexity of direct recapitalization.

NO Scenario, #N3. New deal

Whether the ECB withdraws ELA — and when — is almost beside the point. The liquidity in the Greece economy is seriously impaired and as each week passes the economic, social and ultimately political cost of the crisis will rise exponentially. The tourist season may be compromised. We cannot judge Greece’s capacity for this. There may be new negotiations after a NO vote, but the chances of a soft programme (Scenario 1) or direct bank recapitalization (Scenario 2) are, in our view, very low. In the meantime the domestic political cost of a closed banking system will rise.

At some point, the rising economic and political cost of a closed banking system could cause the Syriza government to fall. A national unity government could emerge and new negotiations could take place around a deal with the international creditors.

How quickly such a scenario plays out depends on the economic and political cost. By that time, after the economic shock of failing talks and default, the scale of debt relief required to return Greece to sustainability will be even larger. If the EU wants to retain Greece in the single currency, more debt relief might be the price to pay.

Such an agreement would have to be based on a more balanced programme, probably along the lines outlined by the IMF in their latest debt sustainability report. There would need to be much more emphasis on structural reforms in exchange for a less growth-unfriendly fiscal consolidation and a commitment on a gradual debt relief based on implementation milestones . There needs to be a sequence that creates the incentives to improve the ability of the Greek economy to pass and implement the structural reforms that would allow the country to stands on its own leg within the monetary union.

A risk under this scenario is political deadlock could result if the Syriza government resigns but parliament is incapable of forming a new, stable government capable of striking a deal with the international creditors. The parliamentary arithmetic says that about 45 Syriza MPs – about one third of the parliamentary party – would have to join forces with the MPs of New Democracy, PASOK and River to gain a majority in parliament. Syriza retains strong support in opinion polls. Combining forces with the opposition could erode support and push voters further into the political extremes.

If a government cannot be found, the next step would be early elections. Note that there would be legal and financial challenges to new elections. According to the Greek constitution, the incumbent government cannot call elections within 12 months of the previous election. The government would first have to resign, followed by renewed attempts by the President of the Republic at forming a government. The constitution calls for three rounds of at most 3-day negotiations with the next three largest parties in parliament before an early election can be called.

NO Scenario, #N4. Grexit

A resounding NO would embolden PM Tsipras to ask for a complete overhaul of the programme. Actually, from his perspective it would make a much softer deal for Greece a necessity. But as we wrote in Scenario N1, an excessive compromise might be as damaging to medium-term euro area stability as Grexit, if not more damaging.

There is no formal mechanism in the EU Treaty that allows a member state to be expelled. That does not mean exit is impossible. First, Greece can take a unilateral decision to change its national currency back to the Drachma. Greece has this right under international public law (“Lex Monetae”). Second, exit could be agreed by mutual agreement. There is a view that Article 352 of the Lisbon Treaty might provide a basis for such an approach. It requires the unanimous agreement of the European Council, i.e. all EU countries in the EU including Greece.

Even though there is no legal mechanism that allows a member state to be expelled, there is a practical mechanism to trigger exit, namely the withdrawal of ELA. Withdrawing ELA would force the Bank of Greece to call in the emergency lending. The banking system does not have the capital for allow this and the government guarantee for ELA triggers a general default. The Greek banks would not regain access to ECB funding until they have been resolved and recapitalized, a lengthy and costly process.

The Syriza government claims it has no intention of leaving the euro area and that it would fight attempts to force it out through the European courts. This leaves economic circumstance to determine the point at which Greece feels it has no choice but to leave the euro area.

What differentiates the Scenario N4 (Grexit) from Scenario N3 (new deal) is that the Syriza government survives and takes the decision to exit. After a NO vote, these are the two most likely scenarios, in our opinion. They have a broadly similar probability, but we see the probability of Scenario 4 (Grexit) rising the larger the margin of victory for the NO campaign.

It is important to note that leaving the euro area and leaving the EU are two separate questions. If Grexit occurs, Greece would leave the euro area but not the EU. There is no argument being made for Greece to leave the EU. Staying within the EU limits the geopolitical ramifications of the Greek crisis.

Sequencing of events after a NO vote

Given the limited contagion in other peripheral markets and the rising domestic pressures in Greece, it is probably in Europe’s interest to wait. The exposure to Greece is no longer growing now that the ELA is capped. Contagion has been contained and the ECB has the ability to intervene more forcefully if necessary. Therefore, there is little cost in waiting for now.

On the other hand, precipitating an exit by e.g. suspending ELA, would lead to a crystallization of the losses on the existing official sector exposure to Greece, the introduction of potentially more challenging contagion risks and initiating a process that will be difficult to reverse. Conversely, given the trust lost over the last six months, Europe is unlikely to find it attractive to loosen its terms without a more credible commitment from the Greek side (or a change in government), as discussed in Scenario N1.

Given the above, it would be rational for Europe to wait for the political process in Greece to play out, even in the case of a NO vote. It would neither trigger a formal exit, nor offer more lenient terms until one of the following three outcomes realizes.

First, in the most optimistic scenario, there is a credible change in position from the Greek government. This would then enable Europe to restart more constructive negotiations along the “new deal” scenario.Second, Greece itself gets closer to considering an exit. At that point, Europe may consider other alternatives such as a managed default within the eurozone, which will require Europe to recapitalize and control the Greek banking system which could lead to either “exit” or “default-and-stay” scenarios.

Third, there is an event that makes it institutionally very difficult for Europe to avoid exit. For instance, if the ECB decides that it is unable to maintain ELA following a default on the Greek bonds it owns, and Europe is not willing to recapitalize Greek banks, which would lead to the “exit” Scenario.

Note that it is not necessarily the case that ELA is suspended as soon as Greece fails to pay the ECB on 20 July – indeed, the ECB left the ELA volumes unchanged on 1 July despite the ‘default’ on the IMF. The rules of ELA are not published. It might also be the case that there is a 30-day grace period on the ECB held bonds. If so, the ECB could avail of the grace period before taking action on collateral (or suspending ELA). The counterargument will be that by permitting ongoing ELA the ECB will probably be in breach of the monetary financing prohibition in the EU Treaty.

And a more bearish JPM:

After the “big no”, euro exit is our base case

- After the “big no” it is now a race between two forces: political pressure for a deal, versus the impact of banking dysfunction within Greece

- Although the situation is fluid, at this point Greek exit from the euro appears more likely than not

Early indications of the official result suggest the result is a “No” by a comfortable margin. What happens next?

First, it will be important to see the tone of the immediate political responses both within Greece and outside. We would expect the tone to be somewhat more conciliatory on both sides. Hollande and Merkel are to meet tomorrow night to discuss the issue, and as we understand it, the Eurogroup is scheduled to meet on Tuesday. We expect that a split is likely to emerge in the coming days. The Commission and France (and possibly others) will argue that negotiations should resume immediately with an aim of finding agreement. Others will find it more difficult to return to negotiations with a newly emboldened Tsipras in short order.

In the German case, for example, the Bundestag has to be consulted before Mr Schauble can enter into discussions about a new program for Greece (as requested on 30th June). However, the Bundestag has just broken for summer recess, so any such vote will require a recall. We have seen reports that talks at a technical level between Greece and the creditors may restart tomorrow (Monday), but we can imagine that the Bundestag will express its displeasure if it feels those discussions are in-progress without their express consent.

Second, there are reports of an emergency meeting between the ECB, Bank of Greece and Finance Ministry tonight, and at the latest the ECB will likely have to take a decision about ELA support tomorrow (if not tonight). Our base case is that the ELA total will simply be rolled on a day-to-day basis for now. It is extremely difficult for the ECB to justify increasing the region’s exposure to Greece at this point. That effectively means that the Greek banks are likely to run increasingly short of cash, and the acceptability of electronic forms of payments will diminish rapidly.

The Bank of Greece and Finance Ministry has a joint committee working to prioritize payments out of Greece for essential imports. There are reports, however, that suggest the logistical problems arising from these procedures are biting. Importers are facing delays in seeing their requests to make purchases processed. And Greek exporters are finding it hard to get payment in euros from those they sell to, as their customers do not want to hold any euro balances within the Greek banking system. It is difficult to get a sense of the scale of these issues at this point. But our best guess is that these issues will multiply in the days ahead.

This suggests that what we see next will be a race between two forces: political pressure to move toward an agreement despite resistance from a number of northern European parliaments, versus the increasingly unpleasant implications of a dysfunctional banking system on the other. This latter force is unpredictable: it may manifest itself in pressure on the government to stand down, or it may generate a more unified “siege mentality” within Greece. The July 20th payment of €3.5bn to the ECB as Greek bonds mature creates one possibly fixed point as we look forward, but our sense is that could be dealt with via a number of mechanisms if political talks are progressing (transfer of SMP profits, short-term ESM loan, for example).

Our base case is that the pressures coming from a dysfunctional banking system in Greece will shorten the time horizon to negotiate a deal to a handful of weeks. As that pressure builds, there is likely to be a temptation to call a referendum in Greece on euro membership, and for the state to begin issuing I-O-Us or similar and giving these some status as legal tender. To the extent that pensioners and public sector employees find themselves being paid with such instruments, it takes the banks further away from solvency (they have liabilities in euros, but will have loans to individuals being paid or receiving “i-o-u” s which will be worth a lot less). Meanwhile, we expect at least some countries in the rest of the region (not least Germany) will not hurry over the design of a new program, and will find it difficult to get parliamentary assent for any such program.

This is a path that suggests to us that there is now a high likelihood of Greek exit from the euro, and possibly under chaotic circumstances. Perhaps the rest of the region will agree to a reasonably quick deal, or the ECB will raise ELA enough to retain minimal viability in the payments system. Perhaps the pressures of dysfunctional banks will force Mr Tsipras to stand down, and a deal is subsequently made. But for now, we would view a Greek exit from the euro as more likely than not.

Risk off, peeps.