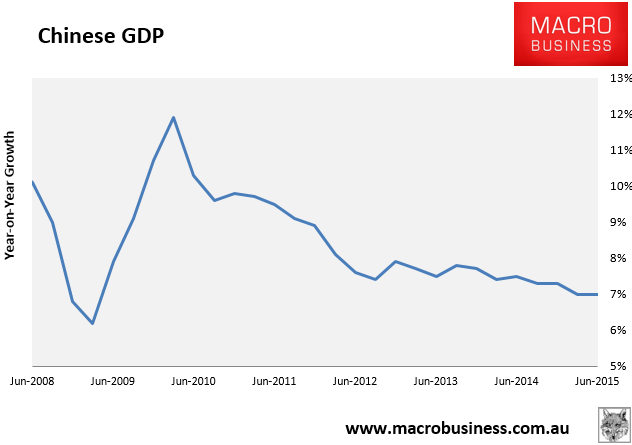

China’s June QTR data dump is out and is a handy beat to consensus with GDP coming in at 7% versus 6.8% expected:

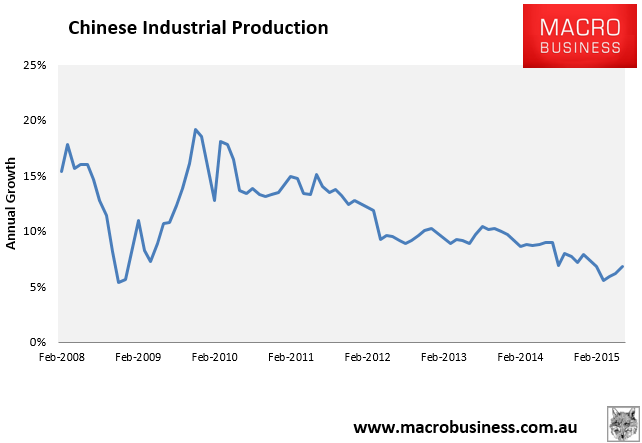

Monthly industrial production was also firm at 6.8% versus 6% expected:

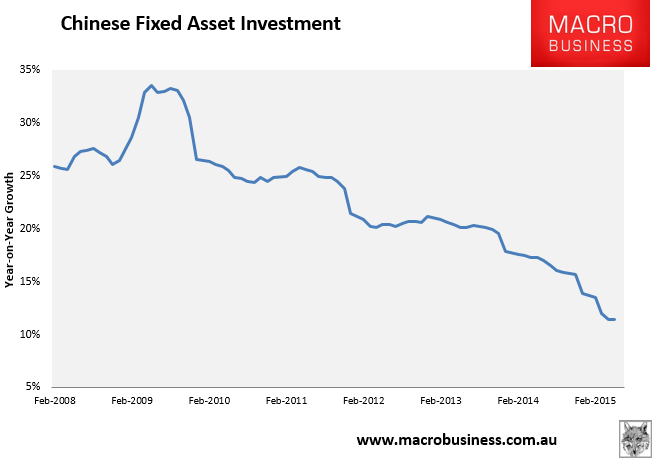

The all important fixed asset investment number was unchanged on the month at 11.4% versus 11.2% expected:

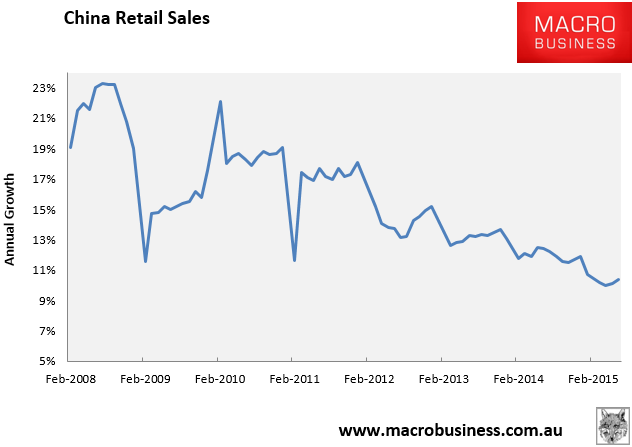

And retail sales were 10.6% year on year versus 10.2% expected:

These are better numbers and markets cheered with the Aussie adding 25 pips but I think after a bit of time these numbers will not please many. They are not terribly credible given the degree of pain we have seen in other core indicators yet they are good enough to choke off any hope of further stimulus for now. That’s not going to help Shanghai which is running on stimulus liquidity not the economy.

In fact, Capital Economics put the better result down to the bubble:

“One reason is that the surge in brokerage activity associated with the equity bubble feeds directly into the service sector component of GDP. As long as spending on brokerage services didn’t come at the expense of growth elsewhere, headline GDP growth will have been stronger as a result.”

“Perhaps more importantly (given that the brokerage boom is unlikely to last), there is growing evidence of an improvement in the wider economy.”

We can at least say that for the time being some stability has returned to Chinese macro indicators. I do not expect anything that you would describe as a “recovery”. Sideways for a quarter or two then down again.