The Labor party’s denial around the Aged Pension is deplorable.

Here were have a measure that currently takes up over a tenth of the Commonwealth budget (excluding civil servants) and costs around $40 billion currently or some 2.9% of GDP. The Aged Pension is also forecast in the Intergenerational Report to grow to around 3.8% of GDP by 2055 without measures to curb its growth.

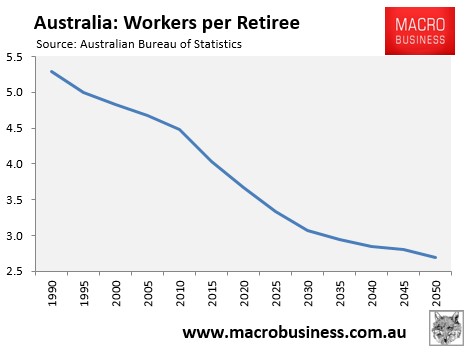

At the same time, the proportion of workers is projected to dramatically shrink (see next chart), meaning the burden on younger working Australians from rising pension costs will rise inexorably.

And yet despite these inalienable truths, Labor leader, Bill Shorten, has vowed today to block the Government’s sensible Aged Pension reforms in the Senate. From The Canberra Times:

Opposition Leader Bill Shorten has announced that Labor will oppose the government’s proposed pension changes.

The decision, revealed to the caucus on Tuesday morning, finally makes clear the federal opposition’s position on one of the most contentious measures contained in the budget.

Social Services Minister Scott Morrison announced in the budget that 170,000 pensioners with modest assets would be better off by an average of about $30 a week.

But as a trade-off, the pension assets test would be tightened and hit wealthier retirees, with around 91,000 expected to lose access to the part-pension and 236,000 people to have their pensions decreased.

A Labor source said the party had arrived at the decision after detailed consideration of the affect the changes would have on people leaving the workforce, with half of all people leaving the workforce in the next decade expected to be hit by the measures.

The Inter-Generational Report revealed just how poorly the Aged Pension is targeted, with those with substantial assets (in addition to the family home) qualifying for welfare:

A pensioner can continue to receive some payment and the Pensioner Concession Card with assets (excluding their primary residence) up to $771,750 for single homeowners and $1,145,500 combined for couple homeowners. A single person who does not own a home can have assets up to $918,250 and a couple up to $1,292,000 combined and still receive a part pension. A single pensioner can also earn up to $1,868.60 per fortnight (approximately $48,580 per annum) in income and continue to receive a part pension, while a couple can earn up to $2,860 per fortnight combined (approximately $74,360 per annum).

For example:

• Kathleen and Steve are 68, own their home and have $1.1 million in superannuation, shares and bank accounts. They have no other income. They will receive a part-rate pension.

• Liam is 75 is single and has superannuation, an investment property and shares valued at $910,000. He does not own a home and has no other income. He also receives a part-rate pension.

• Lillian is 85, single and lives in her own home worth $1.5 million. She has bank accounts valued at $50,000 but has no other income. Lillian receives a full-rate pension.

How is it appropriate that one’s principal place of residence is excluded altogether from one’s ability to fund their own retirement in the pension assets test? Worse, how is it appropriate that a couple who fully owns their home and has $1.1 million in financial assets still qualifies for taxpayer support?

Besides, all the Government’s Budget reforms were going to do was partly return the system back to its pre-2006 arrangement before the Howard Government stupidly relaxed the assets test to qualify for the Aged Pension by halving the taper rate applying to assets (excluding the family home). This measure effectively doubled the value of financial assets allowed for eligible part-Age Pensioners (see here), resulting in the shambles we have today.

In blocking the Abbott Government’s sensible reforms, Labor seems to think that it is okay for younger Australians (“generation rent”) to be called on to support their wealthier parents (“generation home owner”) via never-ending tax increases and growing public debt, rather than tightening eligibility to the Aged Pension, so that only those in genuine need receive it.

The longer that Labor maintains its delusion on Aged Pension reform, the more difficult it will become to tighten arrangements down the track, given the bulging number of oldies.

That said, the Abbott Government is just as negligent in refusing to reform that other great grey gouge: superannuation concessions. At least Labor has proposed reforms in this area, albeit far too weak.

Australia desperately needs reform of both the Aged Pension and superannuation before the Grey Army gets even more powerful and eats its children and grandchildren.

Both sides need to get their acts together fast: Labor on the Aged Pension and the Coalition on superannuation. Both are currently behaving deplorably when it comes to retirement policy.