How the Australian property bubble will burst

Now that we know unequivocally that we are in the grip of a national property bubble let us explore the likely scenario that pops it. There are three clear risks at this point:

- China hard landing

- Grexit

- US tightening

At various points I have shuffled these around in order of probability (and that may well continue), as Europe has bumbled, China has adjusted and the US has inflated. Today I see the Grexit as the lowest probability shock. Although it still seems likely that Greece will leave the euro, given its dismal future if it doesn’t, one wonders now if it won’t take another external crisis to trigger the political chaos needed to force that outcome.

China is clearly struggling with its property bust and I expect only a bifurcated and muted recovery over the next year. The structural adjustment will roll on too. It’s stock market may be exciting and at risk of popping but it’s too small to matter in the scheme of things and, as is the way of such things today, only a solid economic recovery will pop it, which is not in all probability coming. Nonetheless, the command economy has the tools to maintain its chosen glide slope so it too should manage through until the external shock accelerates both its adjustment (and stimulus).

The US is now the top candidate to bring on a cycle ending shock. Its stock market bubble is impressive if not yet fully fledged. Its deleveraging has also been impressive but is only part way over. It’s consumer has recovered some but is no longer the global buyer of last resort and clearly still wants to save with deep GFC scarring driving the decisions of a generation.

History is also a guide to this analysis. If we look back at the last US depressionary episode there is a template that we can use a rough guide to the future.

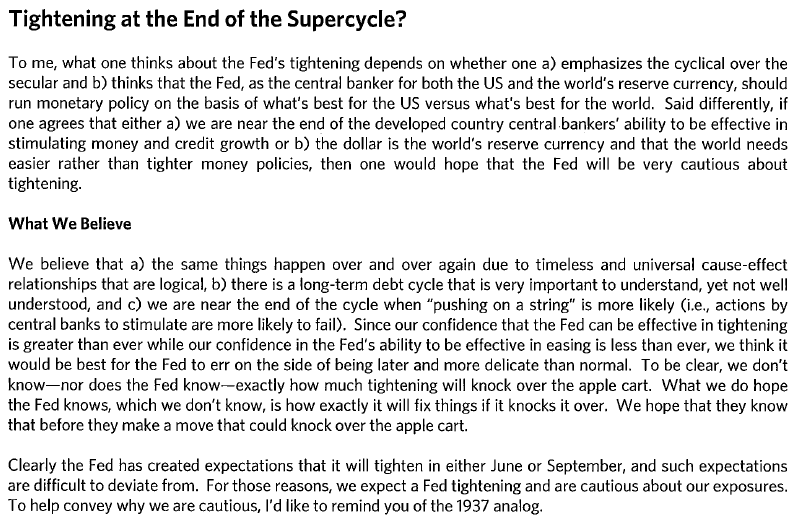

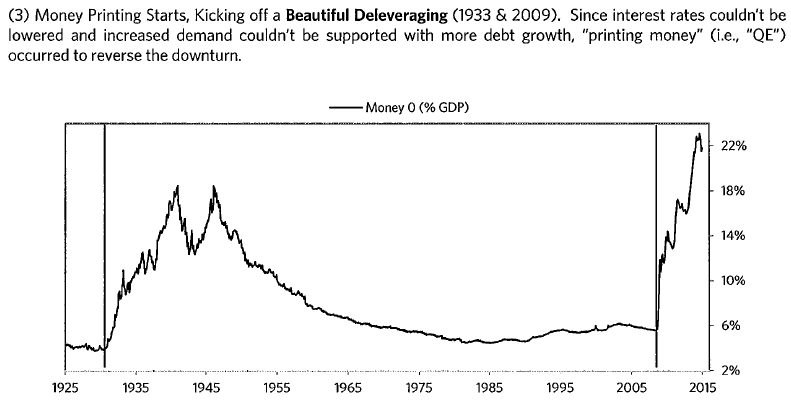

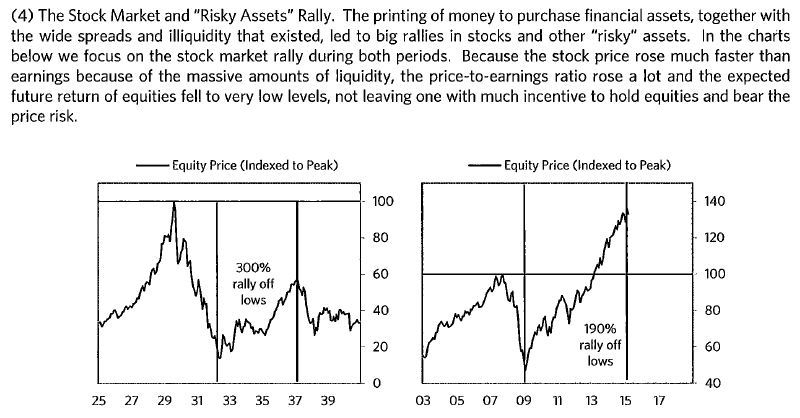

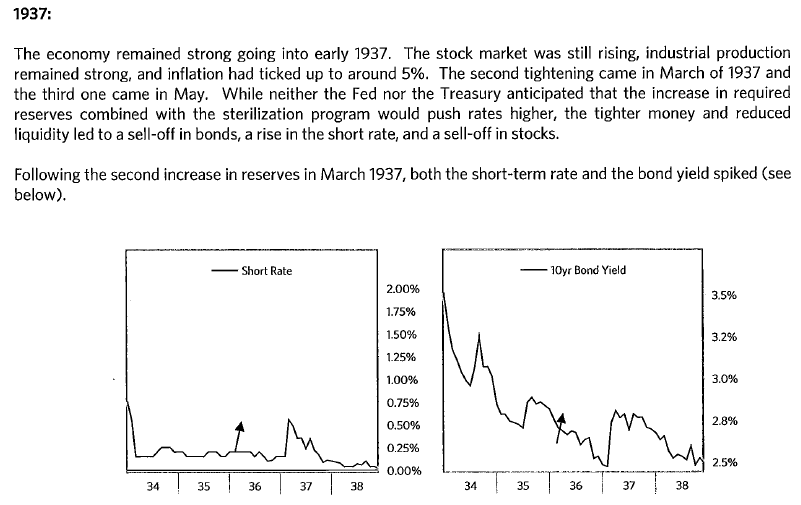

Several years ago at Macro Investor we discussed the “Mistake of 1937”. That was the episode in which the US Federal Reserve prematurely tightened and brought the post-Depression recovery to a shuddering halt. Bridgewater’s Ray Dalio recently examined it at length:

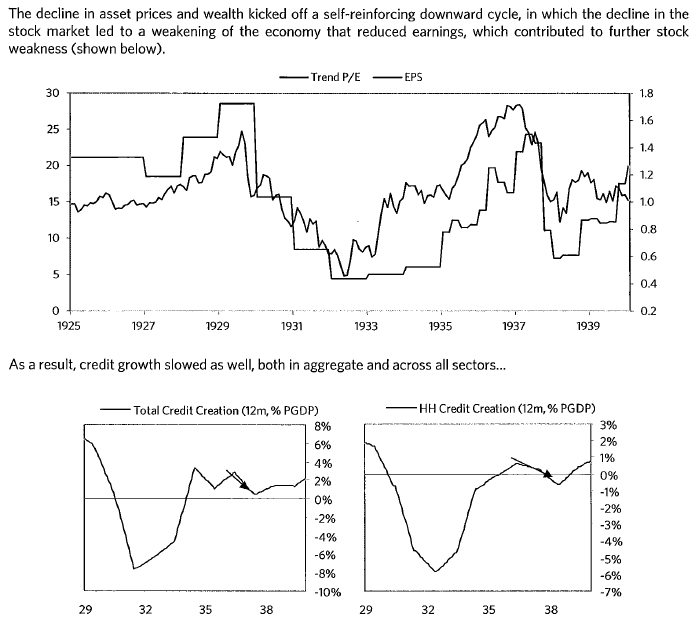

Dalio goes on with a series of charts that tell the tale:

The 1937 analog is spookily familiar with the Federal Reserve looking to prevent asset markets from getting out of control today and to restore some ammunition to its arsenal. But Wall Street and Main Street remain out of sync and it is very likely too early for the economy to tighten.

That does not necessarily make it wrong. If the Fed is confronted with irrational exuberance in markets then it ought to act so rather than characterising the 1937 tightening as a mistake it might simply be a the function of the system, much as it is today if the S&P500 were to pour on greater heights.

Contemporary inflation may be largely limited to asset prices but that does not mean it is not inflation nor that if left unchecked its consequences are not worse than dealing with it shorter term.

So, that’s the clear risk to global cycle. How would that play out in Australia?

First, bond yields will spike across the curve during the tightening. As liquidity dries up in bond markets this will be global and the Australian curve will also rise. Stocks will get hammered as a result, especially the yield plays that have been central to the great reflation to date.

US consumers will bunker as wealth evaporates, sending a trade shock around the world. This, in turn, will crash corporate earnings, making the stock selloff worse.

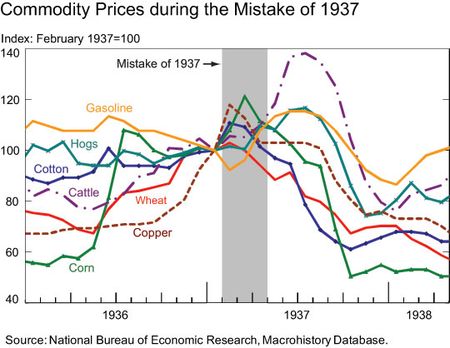

Commodity prices will crash, just as they did in 1937:

As the panic builds, global bank funding costs will also soar.

So, Australia will be in line for a double shock. The first one will be soaring bank funding costs as bond markets dry up globally. The RBA will drop rates as low as it dares and can and it will start using its liquidity facility to keep the banks afloat but the external rollovers are large and the banks will need to increase their net interest margins so the real rate relief for consumers will be minimal even as sentiment cracks.

This will be exacerbated by the second shock, to income, as commodity prices collapse to 2003 lows, and various sovereign downgrades transpire at the federal and state levels, especially as banks are bailed out via LMI nationalisation. Some stimulus will be possible but nothing like 2009/10 and so unemployment will jump. That’s the end the property bubble.

In global terms the Fed will reverse course and print. So will the ECB and China. But there is every chance that the first round of US carnage is followed up by a second phase as trouble explodes in Europe or China. The former could see peripheral nations leave in crisis. The latter could see its own debt crisis as capital floods outwards seeking the US safe haven. It’s a good bet there’ll be some form of very serious contagion in the emerging markets.

I don’t see this as some “end of days” event destroying fiat currencies. That’s some time in the future, perhaps. Rather, it’s a trigger for another round of massive money printing that will restore order eventually, but only so that we can all go through it again.

Australian authorities are totally unprepared for this world. They have neither the ideological framework nor macroeconomic tools to deal with it. These will only come through a reform process triggered by crisis.

And that crisis is property.