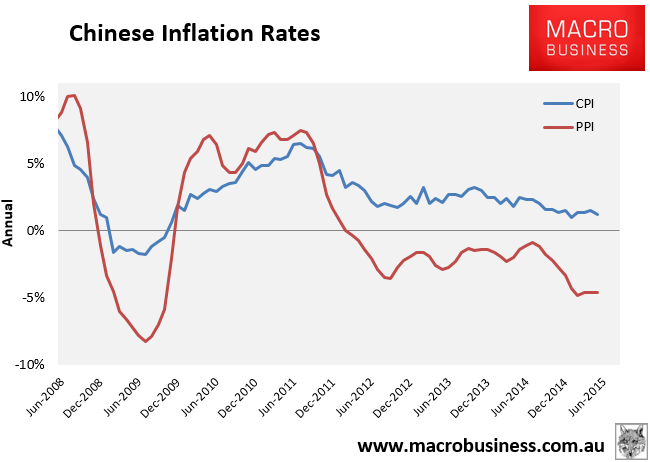

The second of the week’s China data dumps is out and has again missed muted recovery hopes with the CPI at a lousy 1.2% versus 1.3% expected and the PPI at -4.6% versus -4.5% expected:

As you can see, the PPI especially has followed the ebbs and flows of stimulus pulses in growth since the structural adjustment began in late 2011. The current pulse remains dead despite recent easing across the board.

Another bad one for bulk commodities even if markets will leap to the short term conclusion that there will be more easing.

Advertisement