Business Spectator’s Callam Pickering has published an interesting article today looking at new research from economists Stephen Cecchetti and Enisse Kharroubi, who conclude that faster growth in finance is bad for real economic growth:

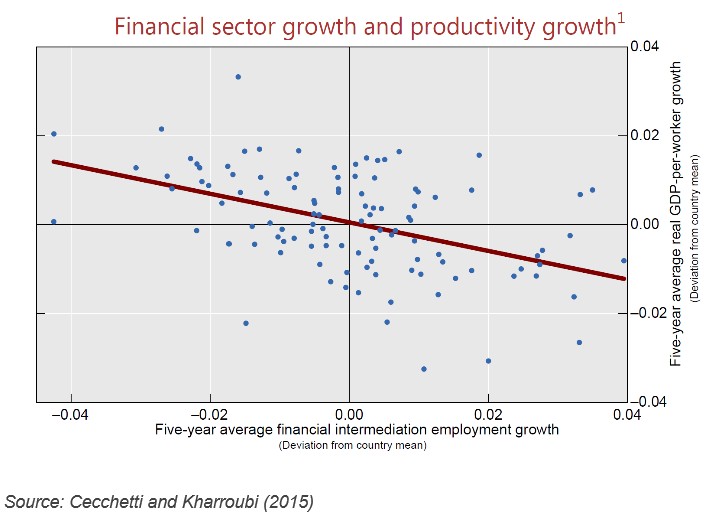

This is readily apparent between 1980 and 2009 — a period in which employment within the financial sector across a range of advanced economies rose at an unprecedented pace. A quick comparison between employment growth in the financial sector and real GDP per worker growth shows a clear downward trend.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.