by Chris Becker

Is Westpac ringing a bell here for banking stocks a day before the RBA will most likely give the oligopoly another boost? The first half net profit of the country’s second biggest mortgage holder was completely flat, unchanged at $3.6 billion as it reported this morning.

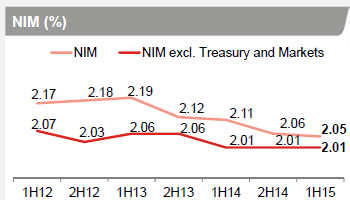

Just as flat analysis points to this as only because of some nasty losses in its derivative business a closer look at what matters – cash earnings (flat), return on equity (down 0.7% to 15.8%), net interest margin (only just above 2%) – shows the bank needs another kick from Martin Place stat!

Advertisement