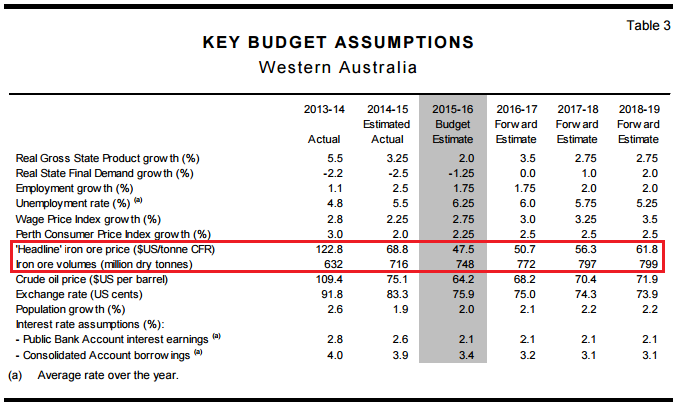

With the release late yesterday of the WA Budget, we can say that Colin Barnett and his treasurer Dr Mike Nahan (let’s call them Dr Nahnet for ease) have learned their lesson; that it’s not a great idea to make fanciful iron ore price forecasts. The new Budget slashes the outlook for the iron ore price:

$47.50CFR is $8 lower per tonne than Joe Hockey. I’m not sure why they don’t agree. It’s still too high but at least it’s plausible. The increases in price in later years will actually be decreases but we’ll let that go.

The volumes are also interesting. There is roughly 150mt in new production coming from 2015/16 through 2018/19 but the Budget sees only 83mt being added for a total of 799mt. BREE by comparison sees a 2019 total of 935mt, over 100mt higher. According to the WA Treasury someone is going to be cutting volumes severely and not just juniors, and they haven’t told Canberra about it.