Sydney, May 26, 2015 — Moody’s Investors Service says that recent changes by Australia’s four leading banks to their criteria for residential investment lending are credit positive for these institutions, but they will also need to implement additional changes to fully address the risks in the housing market.

“In our view, these initiatives are credit positive since they reduce the banks’ exposure to a higher-risk loan segment,” says Ilya Serov, a Moody’s Vice President. “In the absence of mitigating actions, the increasing proportion of investment and interest-only loans would, in our view, lead to a weakening of the bank portfolios’ quality.”

“At the same time, it is likely that further initiatives will be required during 2015 to bring investment lending in line with regulatory guidelines, as well as to adjust lending criteria and capital levels to respond to the rising tail risks embedded in the banks’ evolving housing portfolios,” adds Serov.

Serov was speaking on the release of a new Moody’s report, “Australian Banks’ Moves to Curb Residential Investment Lending Are Credit-Positive”.

Moody’s also says that its expectations of more conservative loan originations and increasing capital continue to support its stable outlooks on the ratings of Australia’s four major banks — Australia and New Zealand Banking Group Ltd, Commonwealth Bank of Australia, National Australia Bank and Westpac Banking Corporation.

Media reports and company disclosures indicate that the big four have recently made changes to their lending practices for residential investment lending, including the removal, or reduction, of the mortgage interest rate discounts offered to new investors. In some cases, the changes also include loan-to-value ratio (LTV) caps and other measures designed to tighten investment lending criteria.

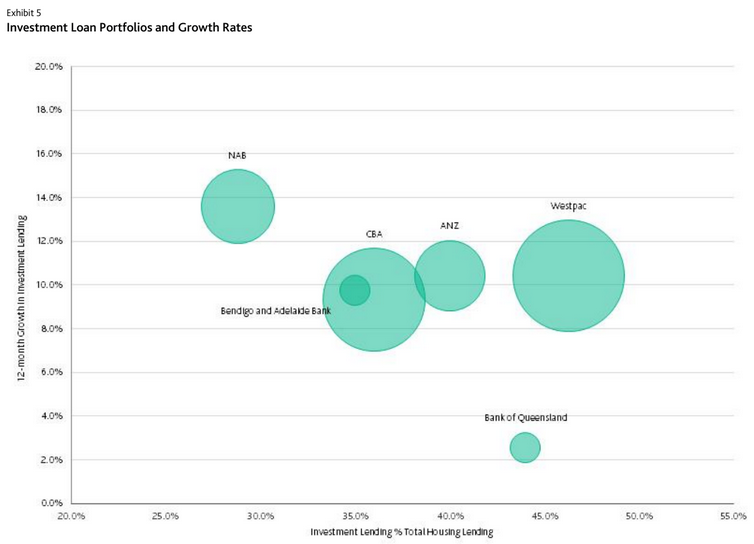

“We expect the changes made by the banks will slow investment lending growth closer to regulatory benchmarks. Although a number of Australian banks are currently running above the 10% regulatory benchmark on a 12-month basis, the latest 3-month annualised data suggest the banks have already taken some actions to bring their investment lending growth rates below the 10% cap. The additional lending constraints are likely to slow down investment lending further,” says Serov.

At the same time, the growing imbalances in the Australian housing market pose a longer-term challenge to the Australian banks’ credit profiles, over and above the immediate concerns around investment lending, says the Moody’s report.

The Australian housing market is characterized by elevated and rising house prices, declining mortgage affordability, and record levels of household indebtedness. In this context, addressing the tail risks embedded in banks’ housing portfolios is likely to entail further tightening in the banks’ lending criteria and/or increases to their capital levels.

“Accordingly, we expect the banks to further curtail their exposure to high LTV loans and investment lending over the coming months. Moreover, we expect that over the next 18 months, the banks will gradually improve the quantity and quality of their capital — likely through a combination of upward revisions to mortgage risk weights and capital increases,” says Serov.

“These considerations, in conjunction with the banks’ actions to improve their underwriting standards, support our stable outlook on the major banks’credit ratings,” says Serov.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.