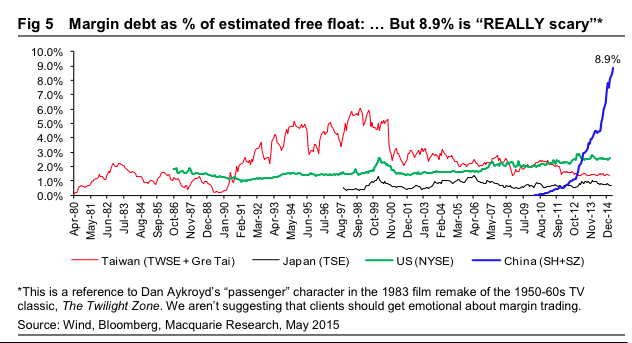

Margin positions in the Chinese equities market have continued to rise in the past month, since we wrote our first Twilight Zone note on April 20. Since then, margin positions have risen by 9.2% MoM to RMB1.9 trillion, or an unprecedented 8.9% of the market capitalization of the combined free float of Shanghai-Shenzhen stock markets. This could already be the highest level of margins vs free float in market history…

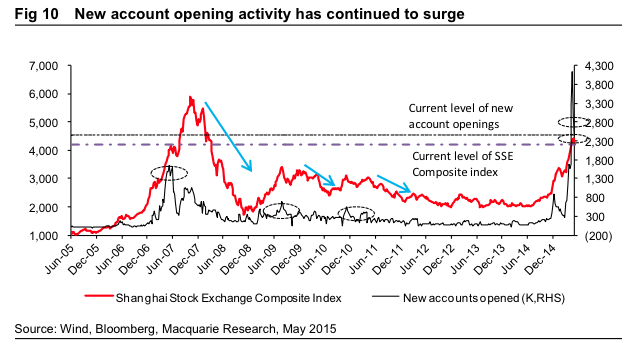

New investor interest was already high in 4Q14, when it reached levels only seen in 2007. However, the CSRC’s move in April to scrap the restriction of one brokerage account per investor resulted in account opening activity spiking to unprecedented heights. A total of 12.8 million new accounts were opened in the subsequent four weeks, and this four-week figure is 36% more than the total new accounts opened during the whole year of 2014.

This extremely high level of margin debt has already dwarfed any historical example that we can find in other markets using the data that is available to us. It is possible that other bubble markets saw higher leverage (ie, the US in the decade-long boom that ended in 1929, Taiwan & possibly Japan in their 1980s bubbles) but we find it difficult to believe that leverage would have moved up as quickly as what has happened in China.

We see the high margin position as a liquidity overhang and thus a risk for share prices in stocks that are highly margined. We are NOT suggesting that widespread margin calls or forced selling is around the corner, or that margin finance – if properly carried out – represents a credit risk for margin lenders in today’s markets. The average coverage ratio for margin positions in China is still high at 2.6x, which should limit both the credit risk to margin lenders (who hold collateral on these loans) and also the risk that positions will require margin calls (which start at 1.5x coverage) or forced selling (1.3x).

Liquidity risk for margin lenders could be another issue. But given the ongoing search for yield in China, we see this as more of a regulatory risk. We don’t get the sense that the Government wants to see share prices tank, so a strict and sudden crackdown on margin finance is not likely to be in the cards, in our view.

Advertisement

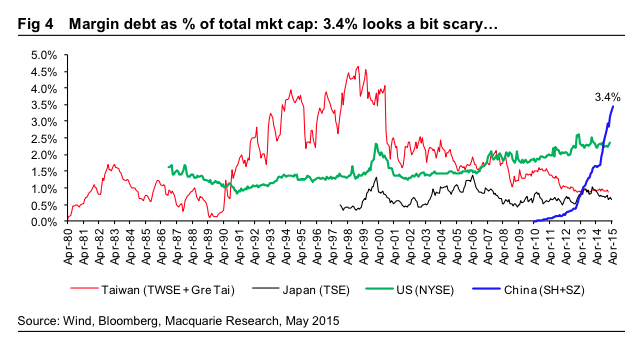

But the margin loans to market cap ratio (now 3.4%) can still be useful for historical comparisons. FT Alphaville [here but, again, we’re open to being pointed to a better figure] came up with an estimated total margin position to market cap (not free float) of “less than 5%” in 1929. Using their 5% figure as representing the epitome of human exuberance, China still has a ways to go. Margin lending could rise by another RMB 854bn, or 46% to reach RMB 2.7 trillion to get to 5% of market cap (assuming no change in prices). Whether or not it gets there is perhaps not a question of animal spirits, which, we can say with a great deal of confidence, are well and truly aroused. The main risk, perhaps, is how much longer Chinese regulators will allow this to continue.

China’s technology stock mania scaled new heights on Monday when shares in a Shanghai-listed real estate company rose by the maximum 10 per cent daily limit after it changed its name to P2P Financial Information Service Co.

The company, formerly known as Shanghai Duolun Industry, acknowledged in filings that it had not started developing a peer-to-peer lending business.

But the company estimated that an Internet domain it recently registered, www.p2p.com, was worth $100m.

The website currently features a few photos and a Chinese caption stating “This domain is worth $100m.”

Advertisement

…Lastly, as we pointed out in our April note, banks’ share prices in Taiwan, Japan, and the US typically peaked and began to decline before the large-scale unwinding of margin positions in previous bubble markets. This has very often – but not always – coincided with financial crises in the respective markets (eg Japan in 1990 and 2007, Taiwan in 1998-2000, USA in 1998 and 2007).

Of course, the past is not a reliable predictor of the future, and China’s markets are different from these historical examples (which, in turn, differ very much from each other). So this very well may play out differently in China.

In any case, the share prices of the China banks do not appear to be pointing toward any such unwinding today. Indeed, the H-Share banks have risen 13% MoM, which makes them the best performers among all Asian banks in that timeframe. This serves to bolster our view that the margin finance boom is likely to persist – not forever, but for a while.

It may be a “Greater Fool” theory, but as Asian regional strategist Viktor Schvets says, the government has little choice but to allow leverage to keep rising. This is because it needs to maintain confidence, and avoiding collapses / encouraging continued increases in asset values is the only way to keep confidence going while re-capitalizing corporates and banks as nominal GDP growth drops towards the 3-6% range going forward.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

for margin positions in China is still high at 2.6x, which should limit both the credit risk to margin lenders (who hold collateral on these loans) and also the risk that positions will require margin calls (which start at 1.5x coverage) or forced selling (1.3x).