Cross posted from Martin North’s DFA blog.

The latest DFA Household Finance Confidence Index (FCI) to end April 2015, showed a further slight fall, from 91.97 in March to 91.87 in April, and continues to track below the long term neutral position.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health.

To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

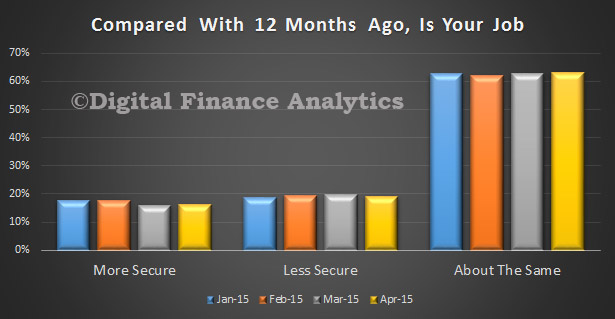

Looking at the drivers of the index, for all Australia, we see that households are a little more confident about their employment status (+0.28%), but there was overall little change (63.2%). We noted a rotation in confidence towards NSW and away from WA, reflecting the impact of the mining boom coming off.

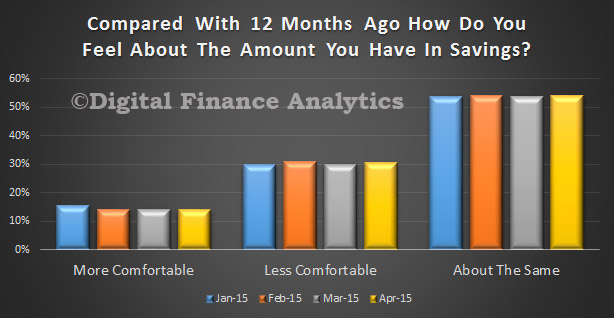

Looking at confidence with respect to savings, we find that whilst about half of the households scored about the same, there was a further deterioration in those more comfortable (-0.3%) and a rise in those less comfortable (+0.43%). The main factors which are driving this related to ever lower deposit interest rates, and the need to tap into savings as income growth stalls. Males tend to be more confident than Females.

Turning to debt, we see that households are less comfortable about the the amount of debt they hold (-0.9%), this is explained by a growth in the absolute level of debt many households have, and concerns that cash flow is under pressure making it more difficult to repay on time. Lower interest rates have not translated into lower debt costs as many hold balances in credit cards where interest rates remain high.

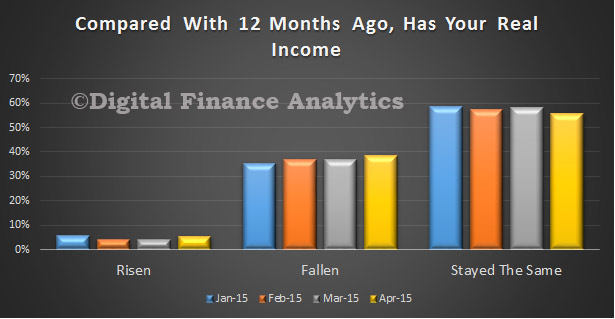

Turning to real income, some households have seen their incomes rise and were more comfortable (+1.5%), but in contrast more are also less comfortable, as their incomes were eroded in real terms (+1.4%), so as a result, the number who stayed the same fell by 2.2% to 55.8%. Those in part-time work tended to be less confident.

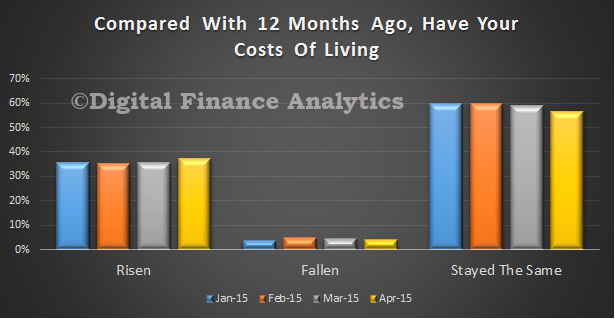

Households whose costs of living rose were up by 1.6% to 37.2%, driven by higher child care costs, garage repair bills, some foods and council rates. 57% of households saw no major change and 4% saw their cost fall, thanks to reductions in fuel costs and some foods. The falling AU$ also had some impact on the results.

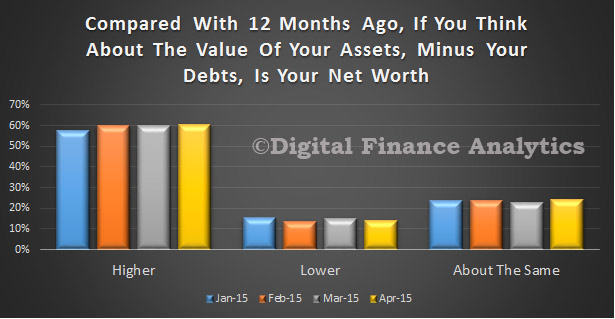

Finally, we looked at net worth, 60% of households think their net worth has improved, thanks to higher house prices and paying forward on mortgage repayments, whilst 14% believe their net worth fell. Many of these households live in rented accommodation, and have substantial debts, and relatively few assets. Those not borrowing, but holding substantial savings balances were more likely to see their net worth reduced.

This data is averaged across the states, though we note some significant differences between WA (overall confidence lower) and NSW (overall confidence higher), thanks mainly to differential movements in house prices and employment prospects.

Note, these results were collated before the last RBA interest rate cut, and the budget speech. We will examine the impact of these factors on households next month.