The RBA’s SoMP offers a deeper dive into the impacts of LNG on the terms of trade:

Over the past decade, movements in Australia’s terms of trade – the ratio of export prices to import prices – have been driven by movements in the prices of commodities, particularly of bulk commodities such as iron ore and coal (Graph A1). This reflects both large changes in the prices of these commodities and the fact that they comprise around one-third of Australia’s total exports. Australia’s terms of trade rose to record levels following significant increases in bulk commodity prices over the eight years to 2012. The terms of trade have declined since then, following substantial falls in commodity prices.

Movements in oil prices are likely to play an increasingly important role in determining Australia’s terms of trade. Given that Australia is currently a net importer of oil, the recent fall in oil prices is expected to lead to an increase in the terms of trade as the effect of the fall in prices for imported oil outweighs that of the fall in prices of exported oil.

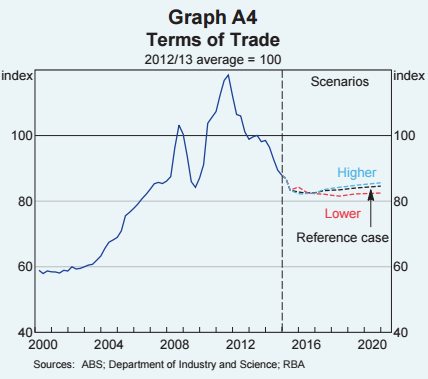

The sensitivity of the terms of trade to changes in oil prices can be illustrated by considering three scenarios: a ’reference case’, which assumes that the Brent oil price follows prevailing futures market pricing (i.e. oil prices move to US$74 per barrel by the end of 2020); a ‘lower case’, where oil prices fall to US$40 per barrel; and a ‘higher case’, which assumes that oil prices rise to US$100 per barrel.

In the reference case, assuming that the historical relationship between US dollar oil prices and Australian dollar prices for Australian gas exports continues to hold, Australian LNG export prices are estimated to fall noticeably by mid 2015 (in response to the oil price having declined by around 50 per cent since mid 2014). 4 LNG export prices then rise again towards their previous level, reflecting the recovery in oil prices implied by futures market pricing (Graph A3). In the case of ‘higher’ oil prices, LNG export prices would rebound more sharply and surpass their current level. In the case of ‘lower’ oil prices, LNG export prices would fall further and remain below their current level over the entire period.

Under these scenarios, the projections for the terms of trade are not markedly different, particularly in the near term (Graph A4). The differences become larger over time, however, as the projected share 4 For the purposes of this analysis, growth in US dollar prices for Australian natural gas exports are modelled using an autoregressive distributed lag model that includes the growth in US dollar Brent oil prices and a constant. Gas export prices are then converted to Australian dollars. The estimation period is from 2000 onwards. Consistent with the sample period, the model implies that for a given increase in oil prices, gas export prices would rise by proportionately more.

And the upshot is that the terms of trade do not move much owing to LNG:

This all holds so long as LNG remains oil-linked, which is unlikely in my. I expect the coming glut to erode if not break the contract system and hence the impacts on the terms of trade from any oil spike will be more negative (mind you, I don’t expect one). You can also lower every forecast line owing to the structural optimism of son-of-BREE assumptions.

But, in short, the impacts of relative prices around LNG are somewhat hedged for the economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Over the past decade, movements in Australia’s terms of trade – the ratio of export prices to import prices – have been driven by movements in the prices of commodities, particularly of bulk commodities such as iron ore and coal (Graph A1). This reflects both large changes in the prices of these commodities and the fact that they comprise around one-third of Australia’s total exports. Australia’s terms of trade rose to record levels following significant increases in bulk commodity prices over the eight years to 2012. The terms of trade have declined since then, following substantial falls in commodity prices.

The sensitivity of the terms of trade to changes in oil prices can be illustrated by considering three scenarios: a ’reference case’, which assumes that the Brent oil price follows prevailing futures market pricing (i.e. oil prices move to US$74 per barrel by the end of 2020); a ‘lower case’, where oil prices fall to US$40 per barrel; and a ‘higher case’, which assumes that oil prices rise to US$100 per barrel.

Under these scenarios, the projections for the terms of trade are not markedly different, particularly in the near term (Graph A4). The differences become larger over time, however, as the projected share 4 For the purposes of this analysis, growth in US dollar prices for Australian natural gas exports are modelled using an autoregressive distributed lag model that includes the growth in US dollar Brent oil prices and a constant. Gas export prices are then converted to Australian dollars. The estimation period is from 2000 onwards. Consistent with the sample period, the model implies that for a given increase in oil prices, gas export prices would rise by proportionately more.