Three developments in the past two weeks suggest that Chinese policymakers are yielding to the pressure arising from economic deceleration and are easing the implementation of fiscal reform. These policy adjustments are being touted by many as a major retracement of reform and deleveraging efforts, but we do not entirely agree.

1) Resumption of preferential tax breaks. In November 2014, as part of the tax reform, local governments were required to phase out all preferential tax treatment aimed at competing for investment. The granting of local tax breaks is considered to have led to market distortion, local protectionism and thus inefficient investment. However, there has been a backlash by both local governments and corporates, which, at least according to local governments, have been one reason behind weak investment. On 10 May, the State Council issued a notice calling for the continued implementation of those tax breaks that have already been formally promised before the reform.

2) More bank loans to ongoing infrastructure projects only. On 11 May, the State Council called on all banks to support the funding needs of ongoing infrastructure projects and said that new borrowing by local government financing vehicles (LGFVs) will be considered government debt. Reading the fine print, we noticed that the announcement only covers ongoing infrastructure projects that had obtained official approval before the reform guidelines for local government debt management (also known as Doc. No.43) were put in place in September 2014. Although Doc. No.43 stated clearly that LGFVs are forbidden to increase borrowing in the name of the government, the Ministry of Finance has been working on a set of supplementary guidelines that could grant a one-year grace period to ongoing projects. Therefore, the 11 May statement does not really contradict the reform guidelines, but it was necessary as some banks seem to have started cutting back credit lines to LGFVs in anticipation of the full implementation of the reform.

3) LGFVs likely to regain access to bond financing. This week, it has been widely reported that the National Development and Reform Commission (NDRC) has issued an internal policy notice on relaxing bond issuance by LGFVs. According to one of the more reliable sources, this notice is still a draft. If implemented, more LGFVs will be able to regain access to the bond market, thus partially reversing the tightening policy installed by the NDRC last September. However, there are two caveats. First, the new rules, as outlined in the draft, only concern key projects in key infrastructure areas. Actually, the NDRC formally issued a few policy documents in early April and has already relaxed bond financing for the construction of urban underground transportation, elderly care facilities and urban car parks. Second, all of the new conditions, both confirmed and unconfirmed, still accord with the principal that the credit risk of LGFV bonds lies with LGFVs, not local governments.

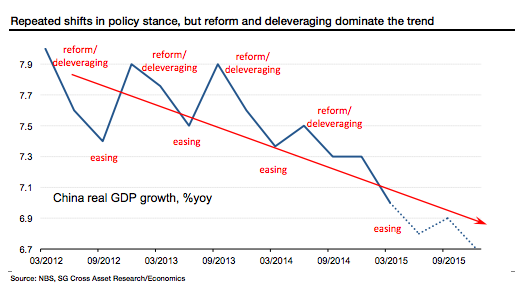

In a nutshell, most of the adjustments are about toning down the strictness of implementation under the same set of reform principals. This is a pragmatic approach, and so we do not think that the changes indicate a permanent setback for the reform process. Furthermore, this is not a new phenomenon. Since 2012, Chinese policymakers have been switching their stance between reform (and deleveraging) and tactical policy easing every two to three quarters. Given the sustained downtrend in both economic and credit growth, one has to recognise that reform and deleveraging is a higher priority over the medium term.

I totally agree. The glide slope has steepened too far and must be corrected. The real story here is that each easing is less effective as the structural adjustment takes hold. In the end, the only sustainable turn in growth will come when the adjustment dividend arrives with rising productivity.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.