From The AFR’s Chris Joye comes his latest missive on the epic housing bubble developing in Australia:

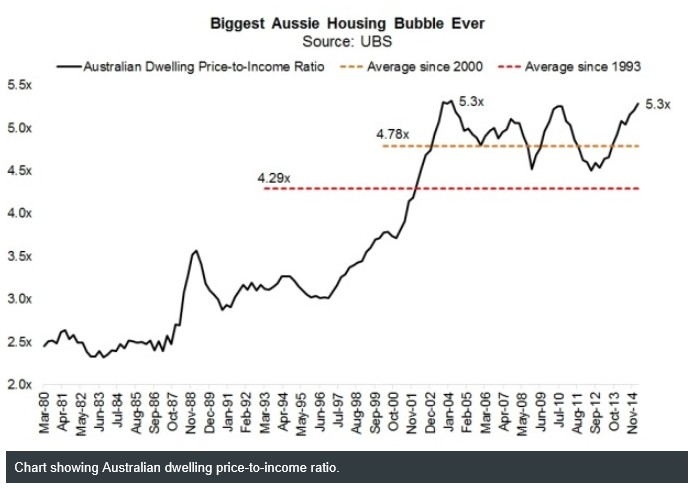

According to UBS, in March the ratio of Australian dwelling prices-to-disposable household incomes equalled – and is presently surpassing – the previous record of 5.3 times set back in September 2003. And they predict it will climb further.

While there were serious concerns [from the RBA] in 2002-03 about mounting indebtedness, all the key measures the RBA publishes on this subject are far worse today. The household debt-to-disposable income ratio hit a new peak of 153.8 per cent in March (the previous ceiling was 152.7 per cent in September 2006). Australia’s household debt-to-income ratio is now 19 per cent above the 129 per cent level that raised eyebrows in 2003…

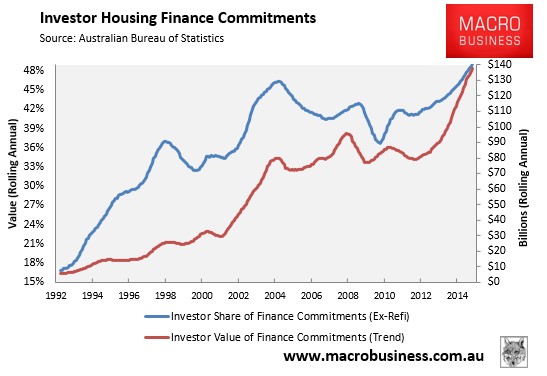

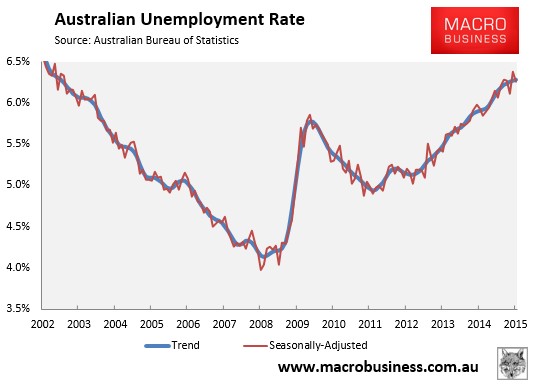

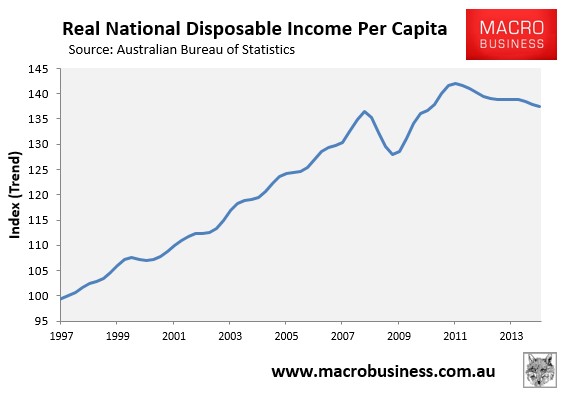

Spot on. If the RBA was worried about a housing bubble in 2003, why isn’t it terrified now given:

1) The unprecedented investor participation, which dwarfs the 2003 experience:

Advertisement

2) The deteriorating labour market (in contrast to 2003):

3) Falling national income (in contrast to 2003):

Advertisement

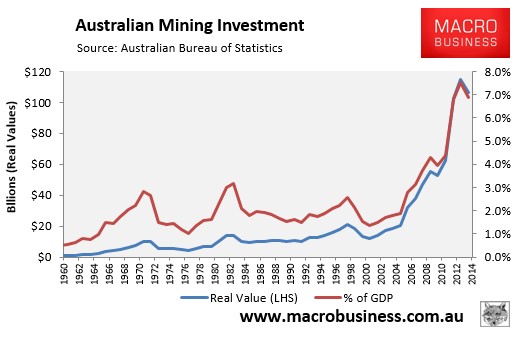

4) And the…err…troubled economic outlook, given the massive ongoing decline in commodity prices and mining investment (see next chart), as well as the closure of the local car industry.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.