Opposition Leader, Bill Shorten, has come out swinging today, claiming that the Government’s decisions on superannuation will drain Australia’s superannuation savings pool of more than $980 billion by 2055, putting pressure on the Aged Pension. From The Canberra Times:

“Last year, the government froze superannuation for nearly 11 million Australians, twice”…

“This decision, combined with their unfair raid on the super accounts of 3 million Australians earning less $38,000 a year, will leave our national savings pool $983 billion worse off by 2055”.

“An average income earner, aged 25, will retire with $100,000 less in retirement savings”.

“How can the government claim a fair pension is unsustainable while trying to wreck our superannuation system – the single best method for easing pressure on pensions and giving all Australians dignity and security in retirement?”

Shorten’s is right to attack the Abbott Government’s cancellation of the Low Income Super Contribution (LISC) – a policy that refunded the 15% tax on super contributions for workers earning less than $37,000 a year.

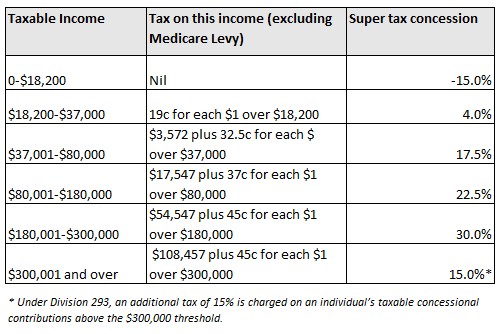

The former Labor Government’s LISC policy was designed to improve the equity and sustainability of the system, which under the flat 15% contributions tax has meant that the amount of concessions received increases as one moves up the income scale (see below table).

That said, Shorten’s claim that the Government’s freezing of the superannuation guarantee at 9.5% (instead of increasing it to 12%) is robbing Australians is inherently flawed.

Superannuation concessions are ultimately paid for by employees, not employers, and to raise the superannuation guarantee would effectively have reduced workers’ take home pay, with potentially harmful implications for lower income earners.

The Henry Tax Review was very clear about who pays for super:

Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement.

Which is why the Henry Review explicitly recommended the superannuation guarantee be retained at 9%, not raised to 12%, so that it didn’t adversely impact lower income earners:

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.

In 2010, as Minister for Financial Services & Superannuation in the former Labor Government, Shorten also acknowledged that superannuation is paid for by employees, not employers:

NEIL MITCHELL:

Okay. When superannuation goes up from 9 per cent to 12 per cent, who pays?..

BILL SHORTEN:

What happens with superannuation is that people’s pay goes up anyway. It goes up each year, by and large. What will happen is that superannuation, the increases to superannuation, will be absorbed as part of people’s pay rises.

…they get a pay rise, of which some will probably go in super, yes…

Between 1992 and 2002, that was the last time super went up, from 3 to 9 per cent… What happened was that real wages increased and super went up. But if you have a look at the years when the super went up, wages didn’t spike. It’s not an extra tax on employers, because the only way that could be is if you assume that employers will never increase the wage of their employees ever.

NEIL MITCHELL:

Okay. So you’re saying that the superannuation increases will be paid for by absorbing money out of the wage increases.

BILL SHORTEN:

That’s the evidence…

NEIL MITCHELL:

Well, so, just to get it clear, business will not be paying an extra dollar, right?

BILL SHORTEN:

No, I can’t see that business will be paying any more in the future than they otherwise would have been if the superannuation changes hadn’t gone through. But what I do recognise is that a portion of what would have been employees’ increases will go into compulsory savings, which is concessionary taxed.

As argued previously, a more equitable and cost effective way to improve Australian’s superannuation system is to:

- Abolish the flat 15% tax on superannuation contributions and replace it with a flat concession (e.g. 15%) that is the same for all income earners (with the lowest income earners receiving a rebate). A reform of this nature would not only improve equity by maintaining the progressiveness of the superannuation system, since all taxpayers would receive the same taxation concession, but also boost lower income earners’ super savings, thereby reducing their reliance on the Aged Pension and relieving pressures on the Budget.

- Increase the access age to superannuation (from 55 or 60 years currently) so that it more closely matches the pension access age.

- Remove the tax-free status of superannuation earnings for those aged over-60.

- Reducing the ability to draw superannuation as a lump-sum.

Shorten should focus his efforts on these areas, rather than seeking to raise the superannuation guarantee to 12%, which would merely heighten inequities already present in Australia’s superannuation system and worsen the long-term sustainability of the Budget.

unconventionaleconomist@hotmail.com