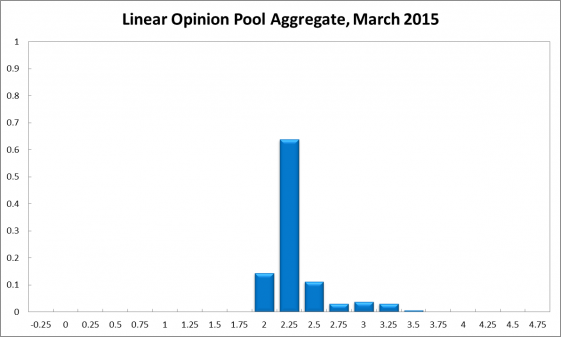

Contrary to the CAMA RBA Shadow Board, which on balance recommended a policy of no change, the Reserve Bank of Australia at its February meeting lowered the cash rate from 2.5% to 2.25%. The RBA pointed to a likely fall in economic growth over the next 12 months – around 2.25%, well below trend of 3% – as the main reason for lowering the cash rate. Weak labour market data confirms the soft economic outlook, and financial markets are anticipating another possible rate cut during the next few months. The CAMA RBA Shadow Board, however, on balance prefers to hold rates and still considers it necessary that the cash rate is lifted in 6-12 months. In particular, the Shadow Board recommends with confidence that the cash rate be held at its current level of 2.25%; the Board attaches a 64% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 14%, while the confidence in a required rate hike stands at 22%.

Recent labour market data underline the cracks in the Australian economy: according to the Australian Bureau of Statistics the unemployment rate jumped to 6.4%, its highest since 2002. The seasonally adjusted labour force participation rate remained at 64.8% but wage growth is weak, 2.5% in nominal terms. Stagnant real wages will put the brakes on consumer spending and make it less likely that GDP growth ticks up again.

The fall of the Aussie dollar has halted at around 78 US¢. There are clear signs the weaker dollar is helping the domestic economy. However, the danger is that Australia is becoming embroiled in the global currency war, whereby countries loosen monetary policy in an attempt to gain international competitiveness. While feasible for countries individually, collectively the world as a whole cannot devalue (exchange rates are relative prices, not absolute prices), and consequently the world economy becomes inundated with liquidity, leading to all sorts of false price signals and economic dislocations. Such concerns underlie the scepticism towards further rate cuts.

Confidence measures remained mixed. Consumer confidence bounced back in February, with the Westpac Consumer Sentiment Index coming in at 100.70 this month (93.2 in the previous month). Business confidence measures remain largely unchanged, but the most recent estimate of capacity utilization dropped from 80.53% in December to 79.96% in January. As the economy is rebalancing and trying to come to terms with the many domestic and international uncertainties, consumer and business confidence measures will continue to lack clear direction.

The picture for the global economy looks much the same as in the previous month: Europe is weak while working through a plan to restructure Greek debt, China is steadying, while the US economy remains the only relative highlight in the world economy.

The consensus to keep the cash rate at its current level of 2.25% equals 64%. There is little confidence (only 14%) that another rate cut is appropriate whereas the Shadow Board considers it more likely (22%) that a rate hike, to 2.5% or higher, is the appropriate policy decision for this month.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 2.25% equals 31%. The estimated need for an interest rate increase lies at 56%, while the need for a rate decrease is estimated at 13%. A year out, the Shadow Board members’ confidence in a required cash rate increase equals 63%, in a required cash rate decrease 12% and in a required hold of the cash rate 26%.

More overly limited and idealistic clap trap. It is certainly the case that currency wars don’t help the world, but standing back on a point of principle and letting the world take your production is hardly a solution.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.