In its Bulletin yesterday, the RBA released a solid article on Chinese property:

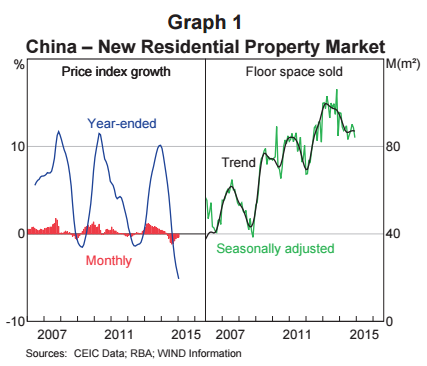

Property development, especially of residential property, represents a sizeable share of China’s economic activity and has made a considerable contribution to overall growth over recent history. Residential property cycles in China have been larger than cycles in commercial real estate, and may pose risks to activity and financial stability. The current weakness in the property market differs somewhat from previous downturns as there are indications that developers may be much more highly geared than in the past, contributing to financial stability risks. Although urbanisation in China may provide support for property construction in coming years, weakness in the residential property market is likely to persist. Policymakers have taken actions to support activity and confidence in the market, and have scope to respond with further support if needed. However, broader concerns about achieving sustainable growth may limit the scale of any stimulus they are willing to provide to the sector.

That sums it up nicely. Here are the crucial charts. Sales peaking: