By Martin North, cross-posted from the Digital Finance Analytics blog:

Today we round out the latest survey results, by updating our other segments. The property as investment bug continues to spread.

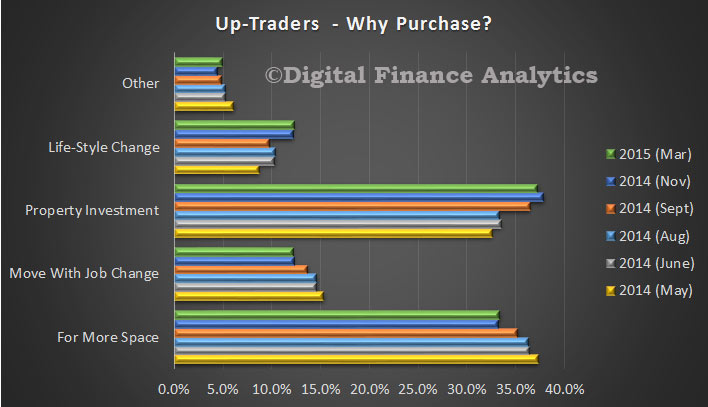

First, those looking to trade up. Property investment has now overtaken the desire for more space as the main driver to transact. We also see that life style changes and purchases due to job changes are of similar significance. Up traders will be looking the purchase property from down traders, who slightly outnumber them.

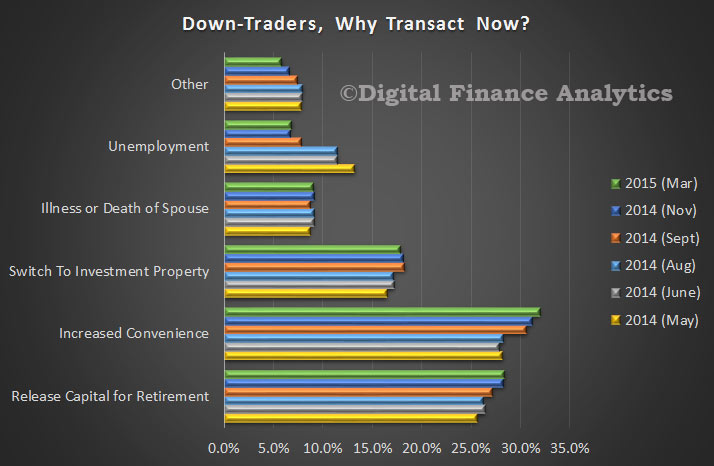

The one million households looking to trade down are still motivated first by the desire for greater convenience, but we also see an increasing desire to release capital for retirement and to lock in capital gains. This segment continue to be less bullish on future house price appreciation. Trading down because of unemployment and death of spouse also figure in the results. About 17% of down traders expect to use some or all of the proceeds of sale to facilitate the purchase of an investment property.

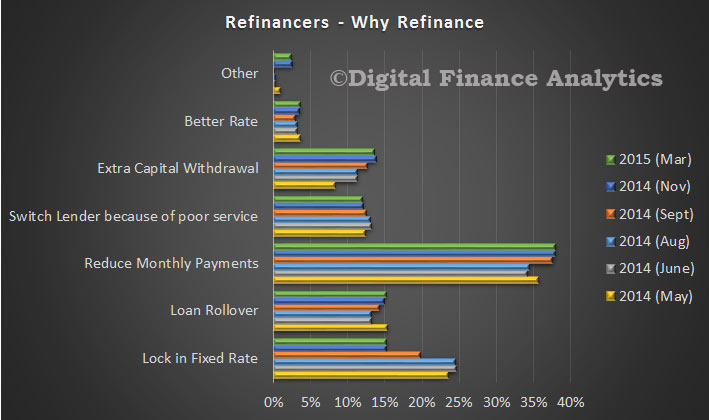

Refinancers are still motivated by the desire to reduce monthly mortgage repayments, though the proportion looking to lock in a fixed rate has fallen, on the expectation of lower rates in coming months. About 16% of these households are looking to release capital, thanks to lifting house prices. This capital will flow to purchase specific items like a new car, or holiday, or as a deposit for an investment property. The flow of money into further property assets of course works against the RBA’s desire to lift household spending towards facilitating economic growth.

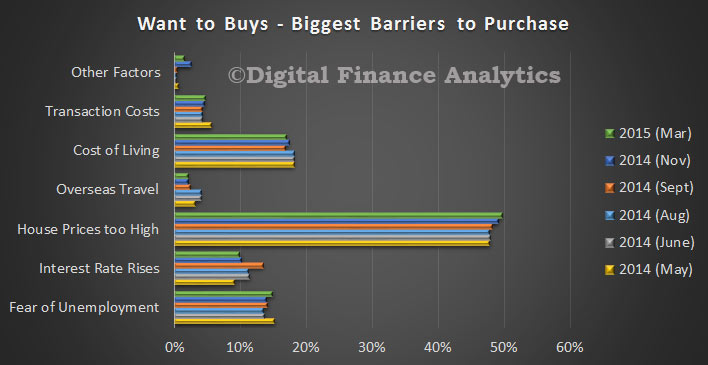

Finally, as we highlighted before, the number of households who want to buy, but cannot continues to rise. The main barrier is the high price of property. Concern about interest rate rises has fallen in the light of RBA expectations.

This concludes the results from our latest surveys, and we will be incorporating the updated findings in the next edition of the Property Imperative, to be released in April.

Standing back, it is all about investment property. The nation is fixating on property speculation. A logical reaction to low interest rates, high house prices, and the search for yield, maybe. However, not good for long term productive growth. Yet, the recipe to address the underlying problem, greater housing supply, changes to negative gearing, increases in banking capital for housing, and other macroprudential measures seem beyond the powers that be. The current trajectory is deeply flawed, but I fear little will be done. Worst still, further interest rate reductions, would pour more fuel on the fire.