Today’s Lending Finance data for January, released by the ABS, revealed that lending outside of housing remains weak.

The below charts, which track lending on a trend basis, illustrate the current state of play.

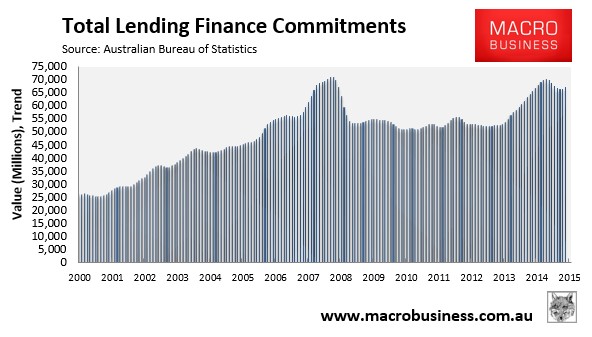

First, total finance commitments peaked in June 2014, and have been trending down ever since, down 4.6% since June, despite rebounding in January:

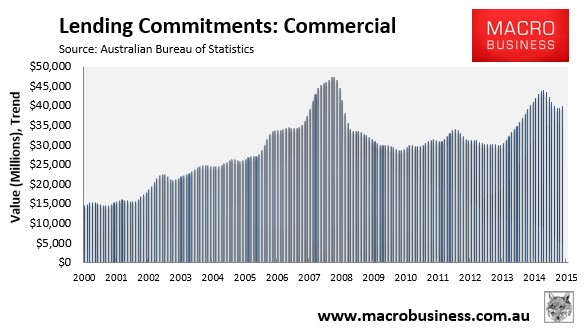

The overall fall in finance commitments has been driven by commercial, where the value of commitments has fallen 9.4% since June 2014, despite rebounding in January:

It’s important to note that around one quarter of commercial loans are lending for property investment, which are growing fast (see my earlier post). This suggests that loans to other commercial enterprises – the productive economy – have fallen fairly sharply.

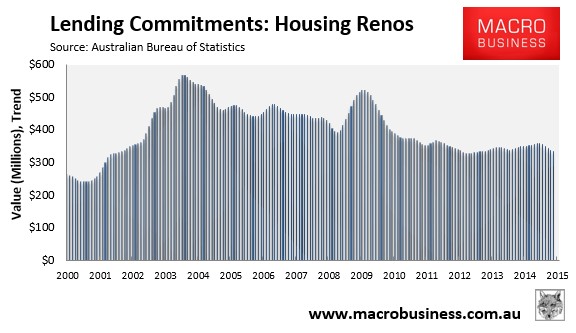

Most of the other components of lending have also been weakening. Housing renovation activity has fallen for four consecutive months and is down 6.3% since June:

Lease finance commitments have been falling sharply, down 12.7% since June:

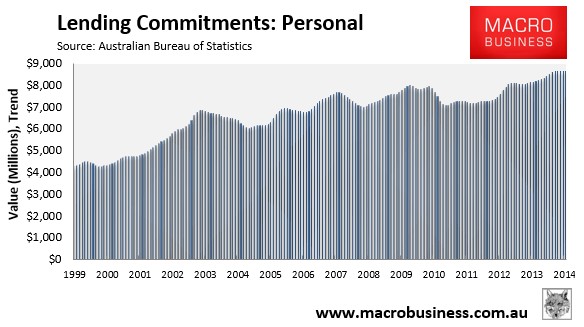

Whereas personal finance commitments have plateaued, up only 1.7% since June but falling over the past few months:

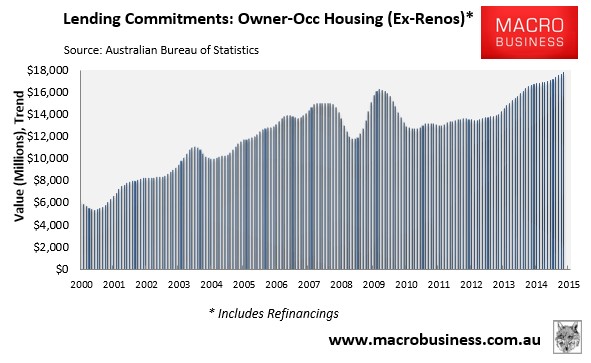

The notable exception to all this is owner-occupied housing finance commitments (excluding renovations), which hit a new record in January, up 5.0% since June:

No doubt about it, our banks are all about housing.