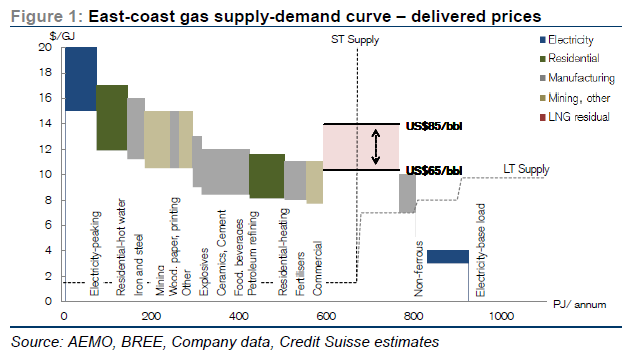

Market is short; in absence of a supply response, demand to do the balancing: the east-coast gas market is short more than 200PJ of supply to meet current domestic demand plus required third party supply to the LNG projects. Undeveloped 2P reserves exist, but a 24-30 month development timeframe suggests that, in the short term, demand must fall to balance the market. As illustrated in Figure 1, the oil price will determine whether the LNG projects or domestic consumers can bid more for supply.

And the proposed solution:

From a national perspective, there is one point we would like to clarify. In, and of itself, it is entirely right and logical to export a product which a country has a competitive advantage in. If the economic rent of doing so is greater than the economic loss from consequential factors, then at the national level it clearly makes sense.

However, the key is that the exporting nation should be the one that extracts the economic rent. Unfortunately, in this situation, it is hard to see who has actually won. Capex bills across the 3 LNG projects are at about $80bn and counting – collectively it is highly unlikely that returns will be greater than 7-9%.In other words, the E&P industry hasn’t even covered its cost of capital – equity markets have been the funders, and losers, from it.

Meanwhile, domestic gas consumers are clearly suffering from higher price. Whilst it is clear that domestic gas prices would have gone up anyway, as the marginal cost of all gas was rising fairly alarmingly, there is no economic underpinning that would logically suggest they would have risen as quickly (or arguably as high at all) with the export projects.

But what can be done to solve the muddle, now we are in it? One the great challenges we see in this situation, from a holistic perspective, is that the tough decisions that have to be made potentially transcend both political and executive team tenures. The greater good may need a decision to be taken today that is deeply unpopular for the incumbent, but makes life far easier for their successor. Common sense needs to prevail.

One of the greatest challenges of it all is funding that $10-15bn of capex that is needed over the coming years. Aside from the Arrow resource, and the Bass Strait of course, large chunks of the unsanctioned resources in the east coast of Australia are owned by Santos,

Origin or the mid-caps. All of these companies have balance sheets that simply can’t afford to fund the scale of investment needed without major injections of equity.

Whilst this will undoubtedly be necessary, and should be given to them assuming returns are palatable, we also wonder whether the government could facilitate the entrance of major gas users taking equity stakes in major projects. Perhaps with major tax breaks, large cap manufacturers could help fund developments whilst also receiving their equity gas at cash costs. When one looks at an asset like Ironbark, where Origin currently own 100%, surely a win/win situation can be facilitated by policy support to entice domestic consumers into the upstream assets?

Domestic reservation taking the form of a facilitated partnership that bails out the LNG white elephants and prevents the fallout getting worse for everyone else.

The moral hazard is pretty sick but all sinking together doesn’t make a lot sense.

Advertisement

But it only makes sense if you think prices will rebound. If the Asian LNG price remains around$7-8mmBtu with an export net back price of $5-6 then price shock is manageable and LNG export volumes will fall over time as their cheaper resources deplete, leaving the shareholders to carry the can not the taxpayer.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.