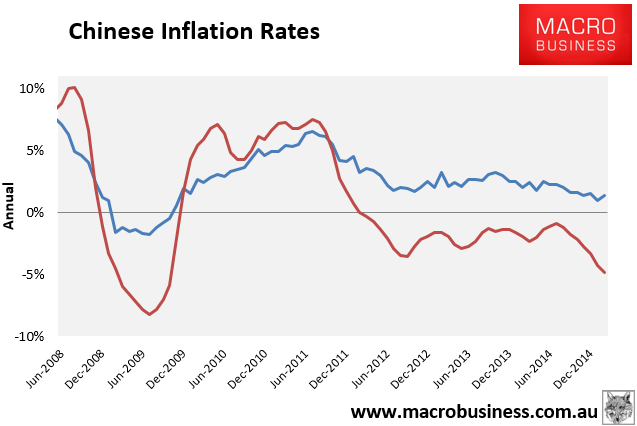

China’s February inflation numbers are out and are decent if your leveraged to the consumer but very poor if you depend upon production. The CPI rebounded as expected to 1.4% which is good because real rates in China (bond yields adjusted for CPI) are lower and it means financial conditions are slightly easier but it alos means a lower probability of rate cuts.

But the PPI is now crashing to post-GFC lows at -4.8%, a full half percent worse than expected:

As I have explained many times, the undulations of the PPI are an excellent proxy for the trend in the China’s industrial economy, especially around construction, steel and mining.

Advertisement