From Investing in Chinese Stocks, land sales for Jan/Feb were down 30% year-on-year 前两月土地出让收入降3成 地方官直言财政紧张:

By the real estate market adjustments on state-owned land use right transfer income 455.3 billion yuan, up by 257.9 billion yuan, down 36.2 percent. There are local financial system to the “Daily Economic News” reporter, said the future revenues and expenditures or conflicts will become more prominent, and the need to further cut costs.

And the cause? Also from Investing in Chinese Stocks:

With the end of the “liang hui” (两会), bad news is flowing again in the Chinese media. Out today are a couple of stories on financing collapses in 2014, which still ongoing in 2015 as the government deals with and tried to get to the bottom of, a major credit bubble implosion.

The real estate market and private lending market collapsed in Nanyang, Henan. Since August of last year, the market has been in trouble, but in recent months, illegal fundraisers have gone down like a series of dominoes. One investor who lost his money said he estimates half the city participated in various fundraising schemes. One government official said many investors have already died, either by suicide or out of despair, and many government officials have also lost their money.

This incident isn’t isolated, in fact similar stories are playing out across all of Henan province, including the capital of Zhengzhou, Anyang, Luoyang and Jiaozuo. In Xinyang, an investor committed suicide by jumping into the icy river.

A team leader with the Public Security Bureau’s illegal fundraising task force in Nanyang said, “This is only the beginning, I expect next year will be even more serious.”

A 40 year-old investor Li said he invested ¥2,490,000 with Nanyang Moyu Development. Since August, he’s been unable to get his money. Everyday he does two things: demand repayment with other investors and fight with his wife. 38 year-old investor Song invested ¥1,700,000 with Moyu and said he quickly realized after investing that he had been duped. Investor Fang took his life savings and the savings of his family. He invested ¥1,000,000, hiding the fact even from his son, and now finds his money is stuck. The three stories are a sample of the more than 3000 investors who are victims of the latest real estate collapse in China.

Around Spring Festival, Moyu, Daxin and Yilin, three investment companies, went broke one after the other. All told more than 10,000 investors are estimated to have lost upwards of ¥1 billion in a still unfolding collapse that has crushed their dreams of striking it rich.

Aforementioned Song only last winter invested ¥700,000, attracted by the allure of 2% monthly interest, or ¥14,000 in interest. To put that number in perspective, the average monthly salary in Nanyang last year was ¥4696. Had Song placed the money in the bank, he would have earned only ¥1000 in monthly interest.

Aside from greed, Song said a big reason why he invested was that a “trustworthy relative/friend” came looking for money. After interest at 10 times the bank’s rate started flowing into his account, he lowered his guard and added another ¥1,000,000 to what he had lent his relative/friend.

“It’s like multi-level marketing, illegal fundraising in a traditional Chinese way between friends and relatives” said Song. Everyone involved is a relative or close friend. The illegal fundraising companies also offered investors a cut of interest from new investors, leading many to start large scale fundraising operations, inviting their fathers, sisters and even sons to invest.

In 2012, the China National Farmers Games’ were held in Nanyang. Many real estate developers came to the city and home sales in July of that year jumped 71% above June levels. Li Liang of Nanyang’s Finance Bureau and official in charge of illegal fundraising cases, said that all developers had to do was buy land. They didn’t begin construction or take any steps towards building, yet they sold out their homes.

Moyu was started by a retired city official, Zhao Mingyun, looking for something to do. “At that time, I never thought it would get so big.” He was considered trustworthy by friends, so several put up ¥3,000,000 each for an equity share. His first project in 2007 involved a distillery with environmental problems. Working with the government, the factory was moved from the city center and he built housing on the land. He spent ¥9,000,000 and earned ¥10,000,000 on the project. He admitted that like every other developer, he was able to sell homes before construction was completed. Today, he has 10 projects ongoing and not one of them is completed.

With government no longer supporting real estate, banks refusing to lend and the housing market cooling, illegal fundraising firms had one choice: raise money from the general public. Li Liang says of Daxin, since inception the firm never borrowed from a single financial institution. Since 2011, Moyu was unable to borrow from banks, so the firm turned to illegal fundraising. Zhao Mingyun says the government had to be aware of what he was doing, “Every developer was like me, they relied on social financing for development.”

Seeing the chance to turn big profits into great profits, developers jumped at high interest rate loans via illegal fundraising. They expanded their projects in the city and branched out to other cities and industries, encompassing hospitals and tourism among others. The projects exceeded these small developers’ operating and management capabilities. For example, Zhao Mingyun grew his company with more and more projects, needing more and more money, causing him to look everywhere for capital.

Things changed in a single month. Suddenly, real estate sales dried up and firms could not repay their loans. It was June 2014, with the national market already cooling, a Nanyang developer Sanjie was exposed by CCTV for using substandard steel rebar. The government ordered all projects halted. One developer remembers the situation, it was like dominoes falling over. Sales collapsed and the market entered a depression. Some homebuyers also came back to demand developers inspect the rebar in the buildings. Zhao Mingyun’s firm was no different and with capital needs increasing, interest costs rising and unable to recoup capital, the firm collapsed.

Li Liang revealed that some firms were offering as much as 3% and 4% monthly interest. With up to ¥500 million invested, this came to ¥20 million in interest each month. He says at that point, the illegal fundraising was purely a scam. According to one official with the PSB, the real estate fundraising cases are only part of the picture. This year could expose even more serious cases.

Henan’s case has attracted the attention of the central government, which has called on the province to clean up the problem and reform. For three straight years, Henan’s illegal fundraising amount was the largest of any province in China. Song Jianbo of Nanyang’s Finance Bureau says the government is working on classifying the cases. Those that involve outright fraud or with a failed project will be handled directly, but those where the project is ongoing, the government will offer help. OF the latter, he said arresting people settles the matter, but it is not good for stability.

In all of 2014, there were 13 cases of illegal fundraising investigated by the government. In a little over one month in 2015, there are already 5 cases. iFeng: 南阳楼市崩塌致非法集资链断裂 数位投资人死亡

Bye, bye shadow banking. And from Deutsche’s Zhiwei Zhang via FTAlphaville the flow on effects are spreading fast:

China’s Ministry of Finance disclosed the fiscal data of January to February 2015 today. National budgetary income grew by a mere 1.7% yoy vs. 8.6% in 20141 . In further details, central budgetary fiscal income grew by -1.8% yoy (vs. 7.1% in 2014) and local by 4.7% yoy (vs. 9.9% in 2014). Among major tax categories, VAT was down 0.6%, industrial corporates profit tax down 3.3%, individual income tax down 7.1% and import VAT/consumption tax down 9.7%, echoing the weak domestic demand and consistent price pressure.

National government fund income contracted 30.7% yoy. Such a drop was mainly dragged by the sharp decline in land proceeds which was down 36.2% yoy, in line with our projection in the China’s unexpected fiscal slide report but much worse than market expectation and government’s 2015 budget. Total government income was down 6.3%, vs. +7.1% growth in 2014.

Weak revenue led to slower growth in spending. National government fund expenditure dropped by 18.6%, of which expenditure related to land purchases dropped by 21%. Budgetary expenditure grew by 9.5%, mostly driven by central government spending which was up 21%, as the government tried to mitigate the fiscal shock from weak land sales. Combining budgetary and government fund expenditures, total government spending grew by 2.6%, down from 6.4% in 2014.

This fiscal shock came in worse than we had expected. The shortfall in land sale is in line with our expectation. What surprised us is that budgetary revenue also weakened quickly. In retrospect, we should have seen this coming. We expected growth to slow sharply in Q1, and cut our GDP growth forecast to 6.8% yoy on 5 January (Q4: 7.3%, Consensus: 7.2%). Indeed growth slowed quickly in Jan-Feb (see our report China – Economy slows in Jan-Feb as fiscal slide kicks in), but we did not expect the knock-on effect on fiscal revenue to happen so quickly.

…We believe the government has been keeping its policy stance tight. This is true from a fiscal, monetary, as well as exchange rate perspective. The PBoC cut interest rates but the real rates remain high due to lower inflation. Moreover, the short-term interest rates such as a seven-day repo stay elevated. In other words, the policy easing cycle has not yet started.

We believe the government will start easing policies in April.This shift in policy stance will likely happen on both fiscal and monetary sides. On the fiscal side, we may see more fiscal spending, through the central government as well as policy banks. On the monetary side, we expect to see a cut of RRR by 50bp in early April when March economic data become available to policy makers. We also expect another interest rate cut in May.

A big question going forward is how the government will fill the financing gap and avoid a fiscal-driven hard-landing. We continue to expect the government to take many initiatives to fill the gap, including privatization, raising taxes and introducing new taxes, issuing more debt, and opening up domestic capital market to foreign investors… We have doubt on the effectiveness of the “public-private partnership” initiative, and we believe the PBoC will have to allow M2 growth to rise significantly above the target of 12%.

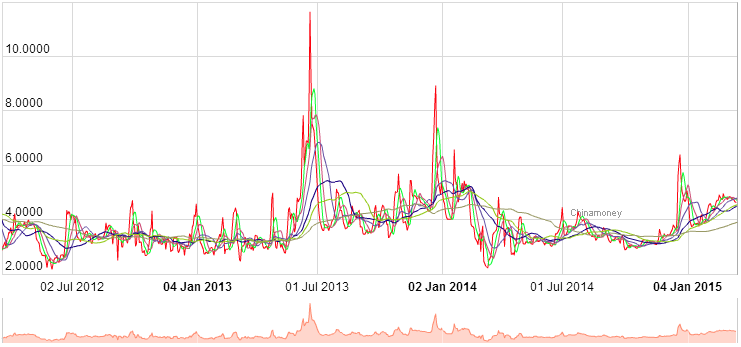

Yes, real rates have been tight. But there is a conundrum here for the PBOC and rate cuts. Capital outflow is ensuring that market interest rates remain high and further easing will only intensify that outflow, further retarding shadow banking especially. Interbank markets remain very tight for SHIBOR:

And repo:

The solution will have to be largely fiscal and more spending coming from the Feds.