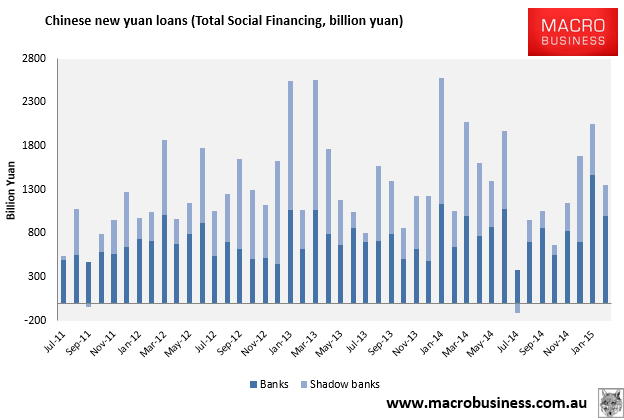

China’s credit data for February was out Friday and showed a decent bounce that effectively restored its deleveraging glide slope. Chinese banks extended 1.02 trillion yuan in new loans and shadow banks added another 348 billion:

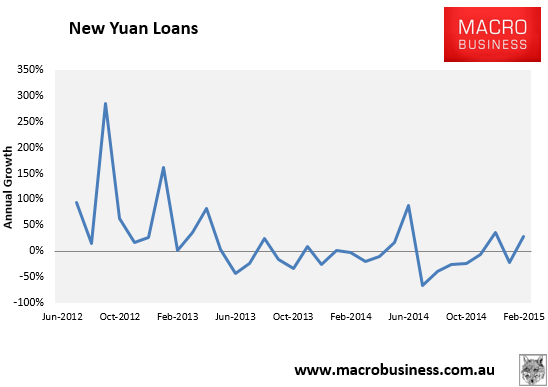

February year-on-year growth was restored to 28%:

However, owing to CNY distortions we should add January and February for a better annual comparison and that calculation delivers and annual fall in new credit of 6%. Subtract a 7% larger economy and you’re deleveraging at a pretty good clip.

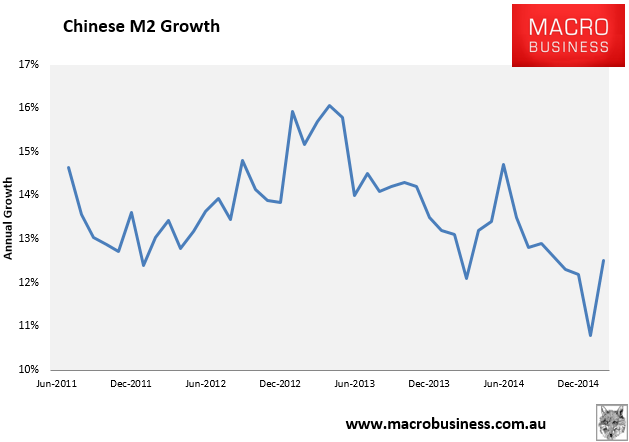

Needless to say, that means falling money supply growth but it did rebound to a more than respectable 12.5% in February:

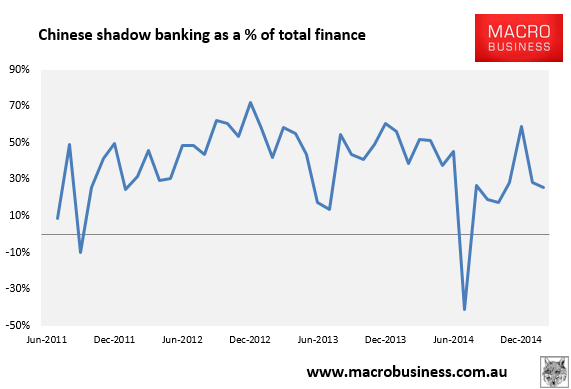

Nothing changed for the structure of lending with shadow banks still under the PBOC’s boot:

In sum, China restored its credit growth to a decent glide slope lower in the first two months of the year, largely though ramping up bank lending as shadow banks decline. It is the mid-year 2014 lending weakness we are seeing in the real economy now. So with some order restored, Chinese growth ought to stabilise mid year on its way to achieving a moderate undershoot to its “about 7%” growth target.

One last point, these figures hint that any more monetary easing will have to wait, though I we’ll need to see the firmer trend continue in March/April to be sure.