From Adair Turner, UK central banker via Project Syndicate:

To spur economic growth and achieve prosperity, China has sought to follow the path forged by Japan, South Korea, and Taiwan, but with one key difference: size. With populations of 127 million, 50 million, and 23 million, respectively, these model Asian economies could rely on export-led growth to lift them to high-income levels. But the world market is simply not big enough to support high incomes for China’s 1.3 billion citizens.

To be sure, the export-led model did work in China for some time, with the trade surplus rising to 10% of GDP in 2007, and manufacturing jobs absorbing surplus rural labor. But the flip side of China’s surplus was huge credit-fueled deficits elsewhere, particularly in the US. When the credit bubble collapsed in 2008, China’s export markets suffered.

In order to stave off job losses and sustain economic growth, China stimulated domestic demand by unleashing a wave of credit-fueled construction. As commodity imports soared, the current-account surplus fell below 2% of GDP.

China’s own economy, however, became more unbalanced. Investment rose from 42% of GDP in 2007 to 48% in 2010, with property and infrastructure projects attracting the most funding. Likewise, credit swelled from 130% of GDP in 2007 to 220% of GDP in 2014, with 45% of credit extended to real estate or related sectors.This property boom resembled Japan’s in the late 1980s, which ended in a bust that led to a protracted period of anemic growth and deflation from which the country is still struggling to escape. With China’s per capita income amounting to only a quarter of Japan’s during its boom, the risks the country faces should not be underestimated.

The rejoinder is that China is relatively safe, because its per capita capital stock also remains far below Japan’s in the 1980s, and much more investment will be needed to support its rapidly expanding urban population (set to increase from 53% of the total in 2013 to 60% by 2020). But counting on this investment may be excessively optimistic. Though China will indeed need more investment, its capital-allocation mechanism has produced enormous waste.

…China’s local-government financing model could hardly be more effective at producing overinvestment and excessive leverage. Local governments use land as collateral to take out loans to fund infrastructure investment, then finance repayment by relying on revenues from subsequent land sales. As the property boom wanes, their debts become increasingly unsustainable – a situation that has already reportedly compelled some local governments to borrow money for land purchases to prop up prices. In the economist Hyman Minsky’s terminology, simple “speculative” finance has given way to completely circular “Ponzi” activity.

As a result, though total credit in China continues to grow three times faster than nominal GDP, a major downturn is now underway. Property sales have fallen, particularly outside the largest cities, and slower construction growth has left heavy industry facing severe overcapacity. The latest survey data indicate a major slowdown in industrial activity. Last month, producer prices were down 4.3% year on year. The resulting decline in demand has caused commodity prices to fall considerably, undermining the growth prospects of other major emerging economies.

…China may well be able to meet the challenge ahead. But, as the investment-led phase of its development ends, a significant growth slowdown is certain – and will inevitably intensify deflationary forces in the world economy. Given this, 2015 may well prove to be another year in which hopes of a return to normality are disappointed.

Versus Glenn Stevens, the central banker that bet biggest on China’s building boom by jacking rates and the currency and “making room” for the thirty year “sell ’em dirt” boom:

RESERVE Bank governor Glenn Stevens has delivered a striking vote of confidence in the ability of the Chinese authorities to continue managing a high-growth economy.

In his testimony to the House of Representatives Economics Committee on Friday, Stevens commended the Chinese authorities for hitting their 2014 growth target of 7.5 per cent and said a target for 2015 of 7 per cent would be appropriate.

“They are by now … the largest trading economy in the world. An economy of that size growing at 7 per cent is still quite an impressive performance, if they can do that,” Stevens said.

It was impossible to say whether the target would be achieved, but Stevens said: “They have done a pretty good job of managing things thus far. I would say there are few countries that could better their track record of growth — I cannot think of any.”

Growth anywhere between 6.5 per cent and 7.5 per cent would be a good result for a country China’s size. Stevens said the main challenge for China was not managing its growth but rather handling the financial excesses left by a period of double-digit growth. “So far, so good, but that will inevitably remain an open question.”

Stevens remains confident in the ability of the Chinese authorities to manage the financial system, including the so-called “shadow-banking” or unregulated sector where most of the problems are believed to lie. “As far as I can see, they are across the issues and are managing them fairly well.”

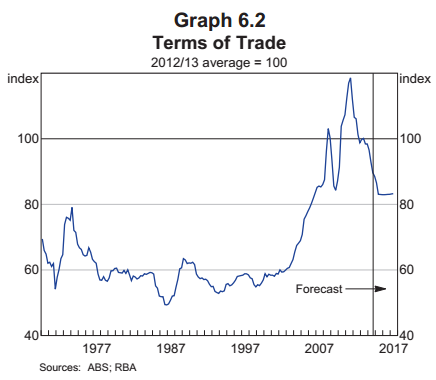

Yes, they are, but they are not issues you ever forecast, nor expected. In fact, the RBA forecast extreme terms of trade levels for Australia forever:

And here’s what’s actually happened so far:

Yet, as you can see, even today the RBA expects a “permanently high plateau” for commodity prices.

You were wrong, Captain Glenn, wrongly wrong, and you’re still wrong with the terms of trade headed inexorably back into high historical ranges sooner rather than later.

Time to own it, Captain, the failure to do so is preventing any sensible policy discussion about how to address the blunder.