Via FTAlphaville comes B0fAML calming the ruffling yuan waters:

Indeed, the trend in diminishing profit growth among Chinese industrial enterprises has correlated strongly with real CNY appreciation in tradeweighted terms, implying limited economic upside for short-term CNY appreciation.

While we retain our broader view that CNY appreciation has still further to run over the longer run, we believe the shorter-term, three- to six-month horizon will see increasing CNY flexibility, depreciation risks, and volatility by extension.

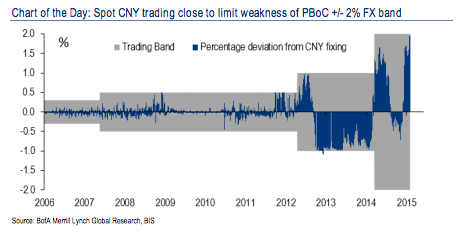

…In our note “CNY weakness – suspects, motives, hedges,” we highlighted that there has been weakness in the Yuan against the USD despite the broad Asia FX benefitting from the ECB’s QE. We believe this weakness is a combination of: (a) domestic capital flight, (b) corporate hedging flows, and (c) PBoC’s FX policy bias. Among these, the PBoC’s FX policy shift presents the biggest risk to CNY, against which we hedge with a 6M USD call, CNH put ratio spread.

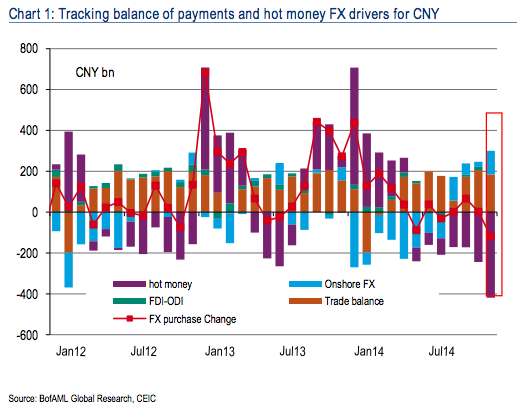

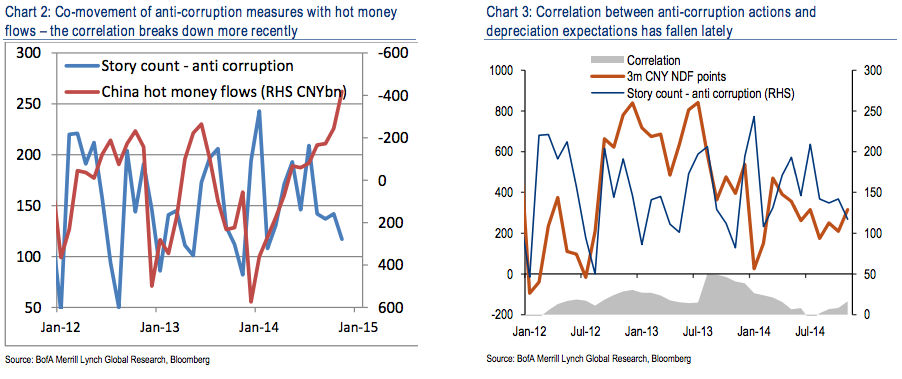

A second driver is cyclical or “reactive” and driven by periodical scare over China’s hard landing or anti-corruption crack down. Overall these tend to be short-term in nature. Chart 3 next page shows the number of Bloomberg stories that are tracking China’s anti-corruption drive against the 3M CNH point or premium that reflects the degree of CNH depreciation expectations being priced in. Chart 3 overlays the same time series of news stories against our measure of hot money flows shown in chart 2.

The two charts illustrate that there was some correlation between China’s anti-corruption drive and expectations of CNH depreciation and a measure of capital flight. However, the key thing is that this correlation appears to have fallen more recently. This would also confirm our suspicion that the CNY118bn FX payment outflows reported outflow in December 2014 is related to seasonal private external debt repayments.

…As such, this cause of CNY weakness does not appear to be the prime suspect, moreover the rally in both domestic bonds and equities would suggest that local investors are adding to their domestic investments. This is also consistent with our previous assessment that China’s economic data has come in better than expected and policy uncertainty has fallen.

I agree. If it’s hot money outflows that are driving the currency tension, then there seems little point going beyond the obvious, that global (and local) speculators no longer see a one-way case for yuan appreciation. That’s not going away.

Even so, I still see the PBOC fighting this outflow for the foreseeable future. Rebalancing is not helped by a weaker currency as income is implicitly redistributed from households to exporters. The upshot is more monetary easing will be needed ahead just to keep credit stable, Shanghai Securities News sees it clearly:

Advertisement

Replace system funding lost via the capital account

Need to provide liquidity ahead of the Chinese New Year

As well as the economic slowdown

But added that addressing the longer-term interbank liquidity picture was the main concern

“Because the PBOC has basically stopped its regular interventions in the foreign exchange market, foreign exchange is no longer a source of long-term liquidity so you must use other channels and tools to deliver liquidity”

“Using the reserve requirement and other monetary tools is needed to increase the money multiplier, to maintain the reasonable growth of broad money and a moderate level of liquidity and lending and to guarantee the stable growth of total social financing”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.