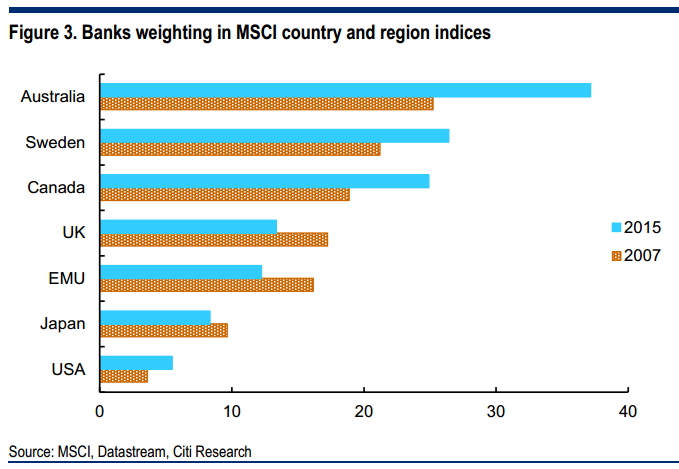

Bubbling along? — The question has come up a couple of times in the past few years, no doubt raised by the six years of outperformance of the broader market the banks have now enjoyed. This has left them accounting for a third or more of the market’s capitalization, in the sort of territory that other major sectors reached in booms of recent decades, like the tech and resources sectors. Of course, the banks have been of significant size within the market for a while, compared to banks in other countries, but even this has increased dramatically in the past half-decade.

Not entirely clear — Other indicators give a different impression. For example, in the tech and resources booms, heady valuations were showing up in the broader market itself, with the market PE over 20x in the tech boom, and market price to book around 3x in both booms, but neither ratio is looking too extreme at present (figure 1). In both the earlier episodes, the sectors ultimately priced in unsustainable earnings, with elevated PEs or ROEs, but with the banks, neither ratio is high, as share prices haven’t moved up much beyond earnings, nor earnings beyond assets.

Citi argues that with credit saturation and increasing competition, bank returns will fall over time so no bubble. There is also the argument I have myself made several times that as yield falls across the economy then it is rational for the price of any yielding investment to rise, also mitigating against the notion of a bubble.

The point that matters, however, is nicely captured in the chart. At almost 40% of the national bourse, the banks are the tip of an economic imbalance iceberg that makes them, if not a bubble, then acutely vulnerable to an underlying economic adjustment.

With 60% of lending in mortgages that are feeding a clear property bubble, you can choose your term to describe bank equity, but I humbly suggest it should not be the word “normal”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.