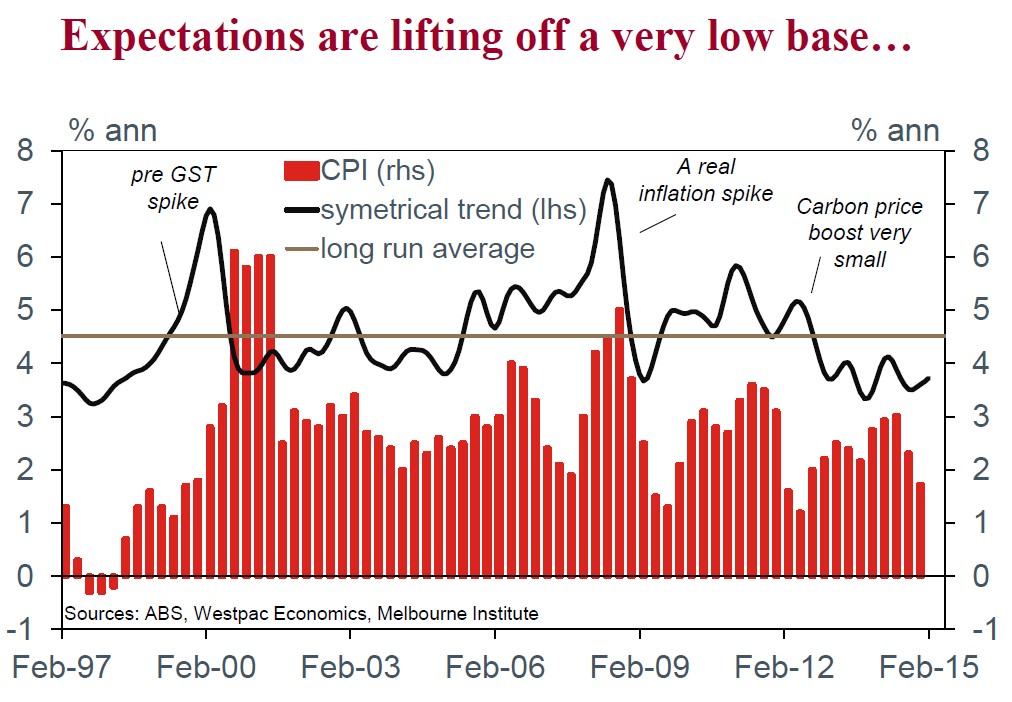

The Melbourne Institute (MI) Inflationary Expectations are reported as a 30% symmetric trimmed mean utilising all responses except for the ‘don’t know’ responses. Compared to the previous old trimmed mean, this adds 2ppt to the level of the index (chart 5). But the new series appears to express greater cyclical amplitude which can be useful for picking turning points in the inflation cycle.

In Feb, consumer expectations for the annual pace of inflation lifted 0.8ppts to 4.0%, getting back close to the small spike to 4.1% in Nov. The trend is now modestly rising again at 3.7% from 3.6% in Dec (was previously flat at 3.5% since Sep 2014) returning it to a modest acceleration path. Expectations are, however, still well below the average since 1995 of 4.5%.

We suspected that the small Nov bump in expectations was due to the surprising rise in petrol prices (pump prices rose +1.0% in Oct). This was not the case for Jan where petrol prices fell 12%.

A closer look at the distribution of responses revealed that the proportion of respondents expecting increases in prices lifted to 70.6% from 63.5% in Jan and close to the 70.9% print in Dec. The proportion of respondents anticipating falls in prices fell to 1.6% from 6.0% in Jan from 2.0% in Dec.

Westpac simplifies this into a net balance that was on an easing trend since May 14 (74.6%). The net balanced bumped a little higher in Feb to 69.0% from 57.5% but it is still less than the 73.2% print in Oct 2014. The trend decline from 74.6% in Jun 14 remains in place (64.7% in Feb from 65.9% in Jan) but were closely watching to see if the breadth of price rise expectations widens again.

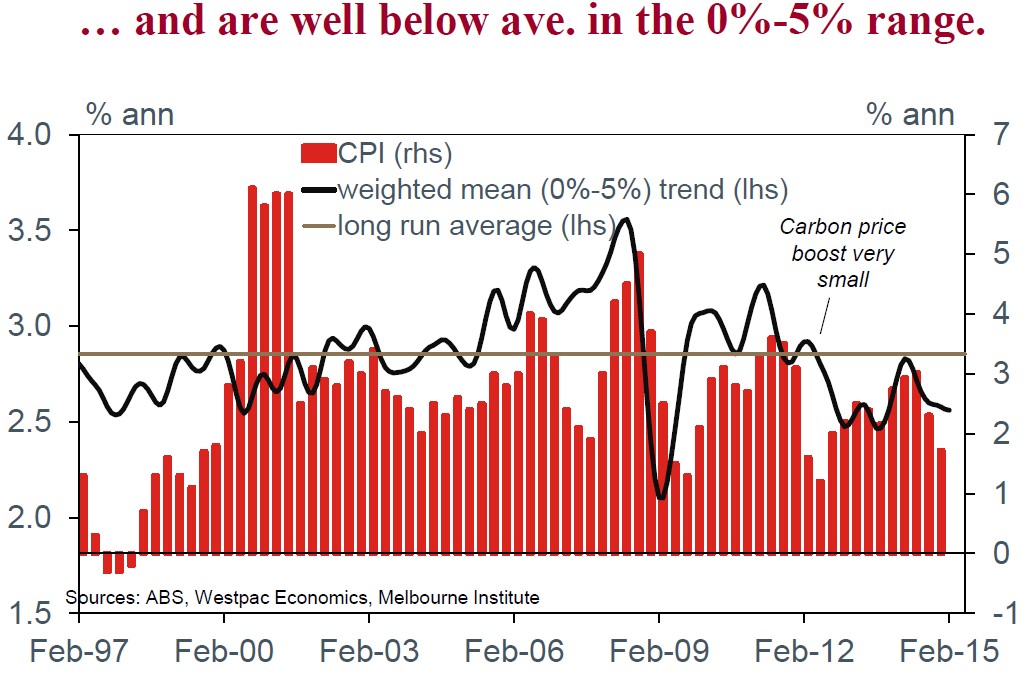

The proportion of respondents (excluding the ‘don’t knows’) expecting inflation to fall within the 0-5% range lifted a touch to 72.5% from 71.6% in Jan. The weighted mean of responses within the 0-5% range was 2.4%yr from 2.6%yr in Dec.

Westpac has found an inverse relationship between the share of those reporting 0–5% expected inflation and actual inflation as reported by the CPI. That is, as the share those expecting inflation to fall within that range declines, it has generally been associated with a pick-up in inflation. Very few ever expect prices to fall so a declining share generally means there is a greater share of very high (and sometime extreme) expectations.

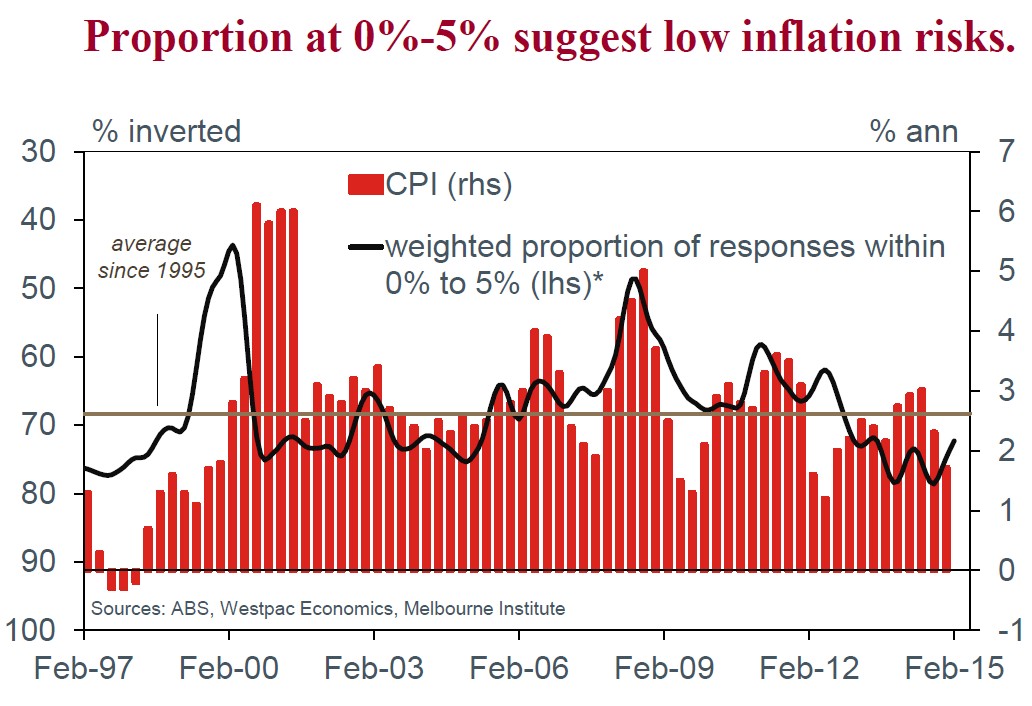

The trend in this series was 72.3% from 73.5% (revised from 73.4%) and 74.8% in Dec. But while it has eased somewhat, it is still much higher than the long-run average of 68.3% suggesting few consumers hold an extreme outlook for inflation. You could argue that further weakness in the AUD could alter this but, at least for now, falling petrol prices are more much great disinflationary influence.

Overall, inflationary expectations remain low and well anchored.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.