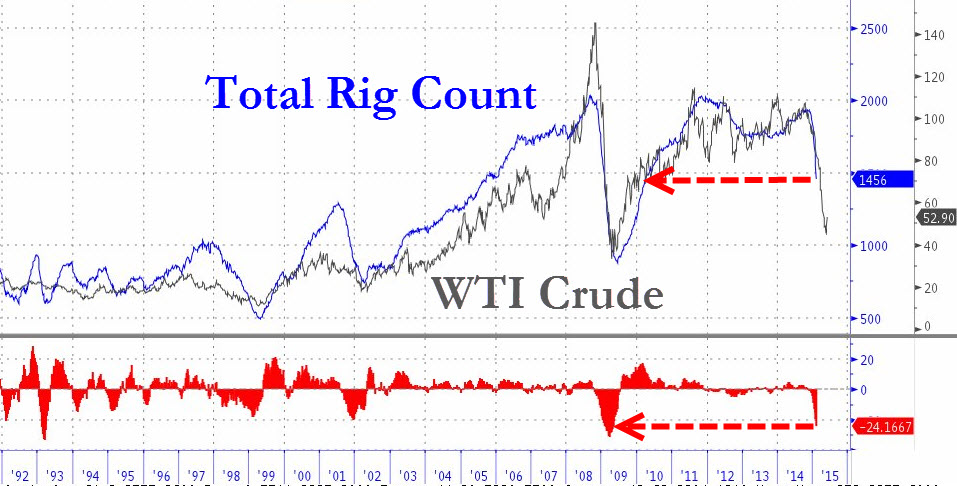

The big news in oil today is the weekly US rig count which tumbled again Friday, unsurprisingly:

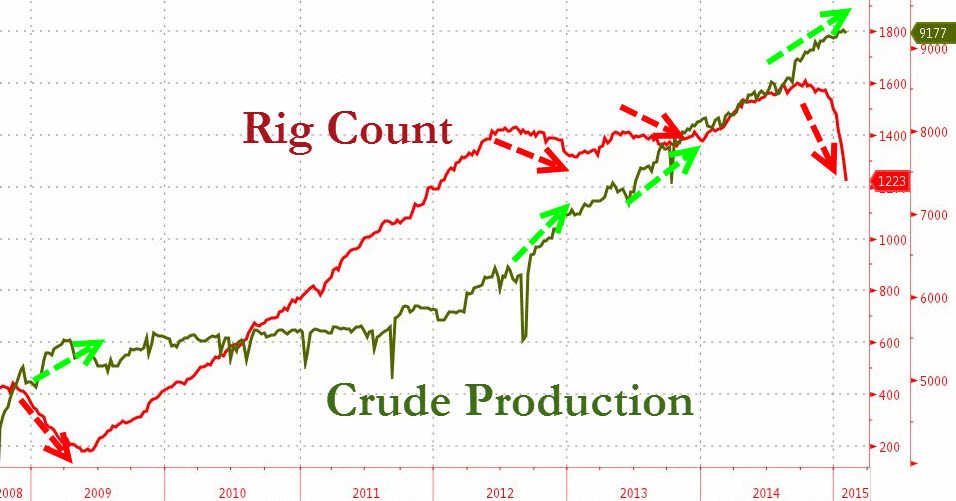

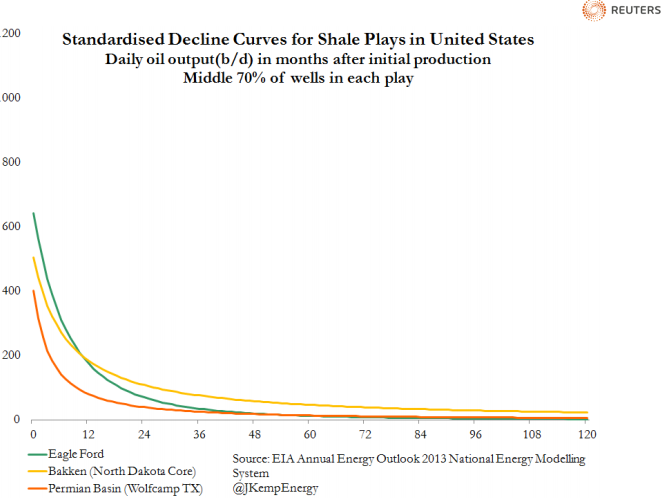

We’ve months yet to run with this but by mid year US oil production is going to be stalling. A few charts from Reuter’s John Kemp shows why:

Advertisement

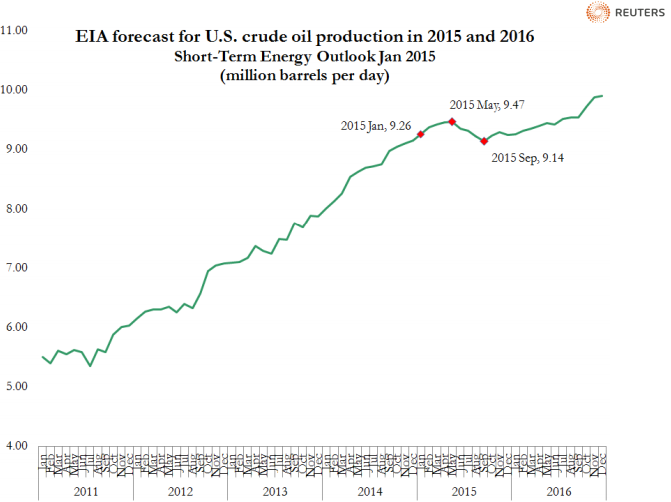

Those are ripping depletion rates in the lower caliber wells that make the majority of production very price sensitive. The EIA sees production falls from May:

Advertisement