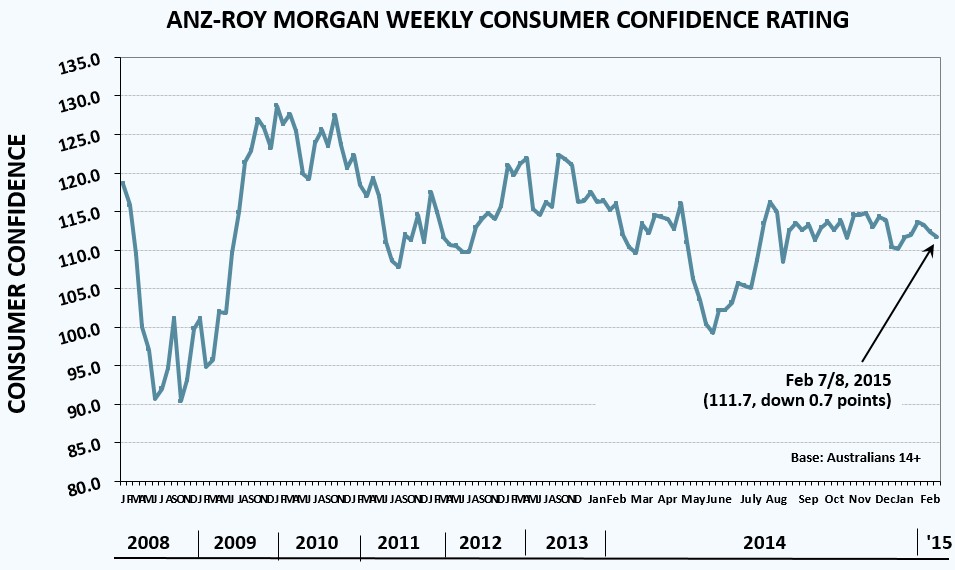

The ANZ-Roy Morgan Research (RMR) consumer confidence index was down for a third consecutive week, falling 0.7 points to 111.7 in the week ended 8 February, to be tracking just below the long-run average (see next chart).

According to ANZ chief economist, Warren Hogan:

Confidence in the economic outlook over the next year (-3.6%) and next five years (-2.6%) both declined. The fall was likely driven by the weakening growth outlook which prompted the RBA to cut rates and government instability which may have reduced confidence in the medium-term economic outlook.

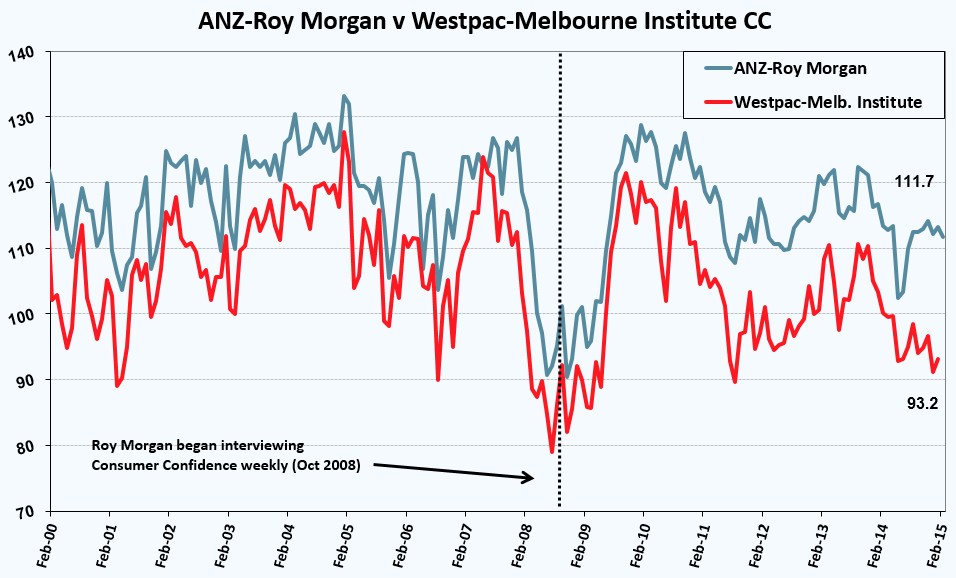

The below chart plots the most recent Westpac-Melbourne Institute Consumer Sentiment index against the latest ANZ-RM Consumer Confidence index. Note the historically large divergence persists between the two measures, with Westpac reporting that pessimists continue to easily outweigh optimists:

It’s worth also noting that consumer confidence is down 1%/10% from the same time last year according to ANZ-RM and Westpac.

unconventionaleconomist@hotmail.com