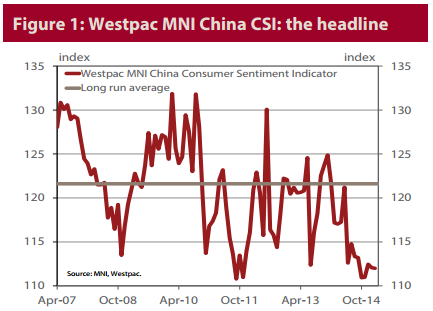

• The Westpac MNI China Consumer Sentiment Indicator, hereafter the Westpac MNI China CSI, decreased by 0.1pts in February, printing 112.0 versus 112.1 in January, –0.1% over the month and –4.4% over the year. The February outcome is 7.9% below the long run average. The absolute level of the CSI indicates that Chinese consumers are still relatively anxious about their own personal financial wellbeing and the economy more broadly. However, the pronounced pessimism that dominated much of 2014 has clearly lessened since the October trough, with the shift in the policy stance the proximate cause.

• Three of the five components that go into the calculation of the Westpac MNI China CSI increased from the previous month. Business conditions ‘one year ahead’ and ‘five years ahead’, and ‘time to buy a major household item’ all moved higher, the latter strikingly so. That was offset by weaker responses on both current and expected family finances, with steep declines in the sentiment of older respondents out-weighing resilient outcomes for the young and middle aged. Current business conditions (not a part of the headline composite, but tightly correlated with official industrial production data) deteriorated.

• A month ago the “current” portion of the CSI was down by 11.3% from a year ago, whereas the “expected” portion was down by a lesser 5.9%. The updated figures are –7.7% and –2.4%. Periods where the forward looking responses are materially stronger than current assessments tend to presage improvement in economy-wide conditions. The caveat is that genuine turning points tend to have stable current readings coinciding with rising expectations. The jury is thus still out.

• The employment indicator declined by a cumulative 11.3% between May and October, and has since increased by 3.4%. The February reading is 8.0% below the long run average. The survey is arguing that in absolute terms job security remains in short supply. Consumers are awaiting a durable pick-up in growth before they fundamentally reassess the job outlook.

• The consumers’ attitude towards real estate (see table 3 on page 4) was more positive in February, following on from the modest cumulative improvement in Nov-Jan. Expectations for house prices gained ground; the share of respondents reporting it was a ‘good time to buy a house’ edged higher; while 19.7% of consumers now nominate domestic real estate as the ‘wisest place for their savings’, the highest since June. Also on the positive side, the proportion of consumers nominating a housing purchase as their primary motivation for saving rose for a third month, albeit modestly. Looking more closely at the house price results, a key feature of the ‘recovery’, such as it is, has been a widening gulf between the East and the Central & Western (C&W) regions. That trend tallied nicely with the official data. The gulf narrowed sharply in February though, on a large improvement in the C&W. Relative to the recent peak, the East is now down by 0.9% versus the C&W at –5.5%. A month ago, those figures were –2.1% and –10.9%. We are treating the size of the C&W gain with scepticism given the evident imbalances, but the idea that housing has passed the worst is becoming more appealing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.