Shares in the country’s biggest lender are running red hot, with new research showing that CBA is trading at a dramatic premium to its Big Four competitors ANZ, NAB and Westpac.

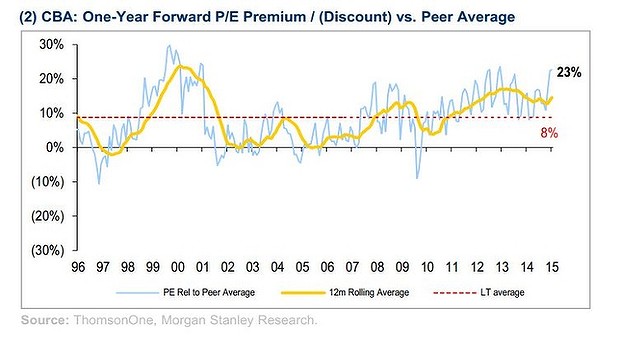

CBA stock is valued 23 per cent higher than its peers based on forward P/E multiples, well above a historical premium of 8 per cent, calculate analysts at Morgan Stanley.

The bank’s share price have been trading at record highs and briefly touched $90 in recent days as the prospect of lower interest rates have propelled investors out of safe but low returning deposits and towards high yielding blue-chip stocks.

The shares trade at 15.7 times estimated earnings for this financial year, according to Morgan Stanley, against an average of around 12.9 over the past decade or so. CBA also trades at a price/book ratio of 3 against a longer term average of around 2.3. Unsurprisingly, all this enthusiastic buying has had the effect of pushing the bank’s one-year forward dividend yield to 4.8 per cent (before franking) against an average in this decade of 5.9 per cent.

The fundamental reason is simple enough. As I’ve said many times, the capital value of yield investments will rise as interest rates fall and the risk free rate gets closer to zero. So, with rate cuts coming and likely to keep flowing, the final leg in the yield play could be quite aggressive.

You don’t necessarily have to see this as a bubble, either, if you think that rates are down more or less forever. Though you do have to accept you’re not discounting any risk of contagion from the commodity economy into the broader economy, and good luck with that!

Advertisement

It is interesting to speculate on the genesis of the little CBA bubble. The bank is well managed (within the limited framework that these things are judged in Australia), has a substantial technology edge and no exposure to offshore markets (like NAB or ANZ) but that doesn’t explain it. Morgan Stanley sees it this way:

CBA (Overweight): In our view, CBA’s business mix, franchise momentum, cost flexibility and capital generation mean it is better placed than peers to deal with a subdued operating environment and the prospect of higher capital requirements. We believe that these factors support the stock’s premium trading multiples vs major bank peers.

ANZ (Underweight): ANZ is our least preferred major bank because there is downside risk to consensus earnings estimate, and we believe it is more vulnerable than peers to higher capital requirements, because it has a relatively weak CET1 ratio, and its strategy relies more heavily than peers’ on balance sheet growth. We think a subdued operating environment and a need for more capital could force ANZ to revise its ROE target.

WBC (Equal-weight): WBC’s yield and risk profile remain investment positives, while its Australian franchise momentum has improved. However, with loan losses at the bottom of the cycle, WBC needs to deliver better revenue growth and target positive jaws, we think. We also believe franchise momentum could disappoint during CEO transition. WBC’s trading multiples are full, in our view, and de-rating risk will increase once the upgrade cycle ends and dividend growth slows.

NAB (Equal-weight): We believe some “self help” is encouraging (given efforts to accelerate the exit of non-core businesses, deal with legacy assets, strengthen conduct cost provisions and raise some capital), but a sustainable re-rating vs peers requires an Australian turnaround and a clearer UK exit path. In the meantime, we forecast profit growth (ex write-downs) of ~2% and a flat dividend in FY15.

This is the kind of hair-splitting one gets in the over-consolidated Australian economy. The four banks are much the same, with similar returns on equity (excepting NAB’s UK albatross) and capital ratios (though WBC lags).

Advertisement

My guess is that the CBA premium is really a safe haven play. The above chart shows you that it expands dramatically when economic pressure mounts. As the former central bank in Australia and the one that carries the stamp of the sovereign, everyone turns to CBA as the bastion of economic strength when trouble strikes.

It’s an illusion of course. All four majors are too big to fail. And, in fact, if trouble ever does come to the big banks, the CBA premium may well collapse, making it less of a safe haven after all.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.