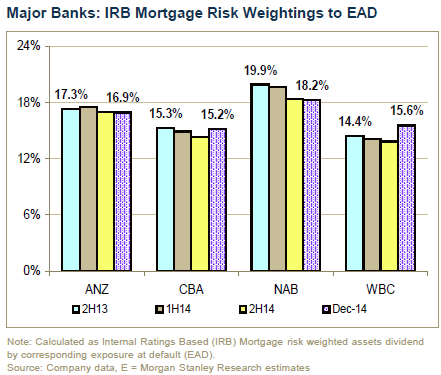

Our Chart of the Week shows that mortgage risk weightings (RW) under the internal ratings-based (IRB) methodology have risen for CBA and WBC by ~0.9ppt and ~1.7ppt, respectively. WBC noted a 21bp reduction in the CET1 ratio due to: “Changes to the determination of probability of default”. In our view, mortgage RWs will increase further. APRA Chairman, Wayne Byres, observed that internal models “lack credibility as a reliable measure of financial strength” and that regulatory capital for housing held by IRB banks was not sufficient to cover losses under APRA’s 2014 stress tests (refer APRA: The Rule Maker). In our base case, we assume that APRA will lift major bank capital requirements by: 1) adding an additional 100bp D-SIB buffer; and 2) imposing a 20% mortgage risk weight floor that would add ~90bp. This would increase major banks’ average mortgage RW from ~16% currently to ~28%. We estimate that every 5% increase in the RW floor lifts the major banks’ capital requirement by ~A$6bn, with WBC the most impacted and ANZ the least impacted.

For perspective, recall that to reach actual capital levels, IRB discounts must be multiplied by the 8% Basel III capital discount for mortgages, so based on the above figures you reach the very reassuring level of bank capital of $1.30 per $100 of mortgages.

Of course there’s some offset in the Lenders Mortgage Insurers, but only so long as they remain solvent.

And that, my friends, is how big banks turn lousy credit growth into high returns on equity, by employing ludicrous leverage!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.