by Chris Becker

Concrete losses from speculating in mining towns and related areas in Western Australian and Queensland are being confirmed with the release of CoreLogic RP Data’s quarterly Pain and Gain Report.

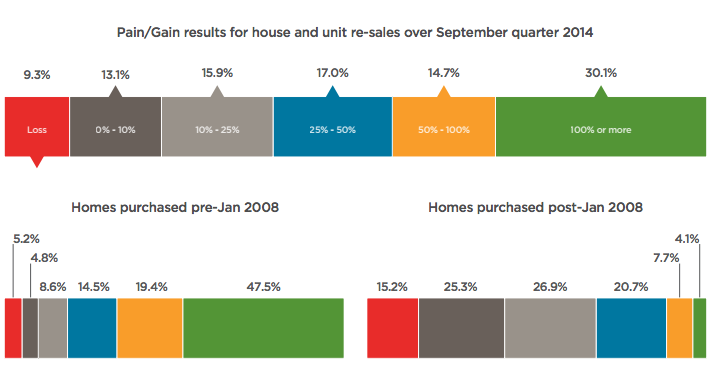

Its not just the frothy end of the mining boom as the September 2014 quarter reported a gross loss over 9.3% of all resales, compared with 9% from the June quarter, or about $383 million.

That’s the bad headline news, the “good” news is more than 90% of returns were positive with over 30% doubling their returns! And thats only nominal, imagine with leverage?! Can’t go wrong with bricks and mortar hey? We’re talking over $13 billion in gross profit, or over $220,000 per property.

Houses will always trump holes. Or innovation or real productive investment.

Timing and time held is always a factor with a substantial 40% or so of all sales since the GFC being inflation-adjusted losers, but before that only a handful of buyers have lost out:

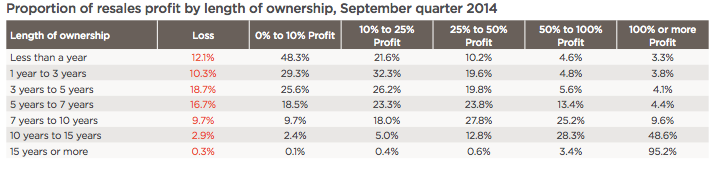

Losers had an average holding time of only 5.7 years versus winners with a 9.9 year hold, and the double-down crowd holding on for 16 plus years:

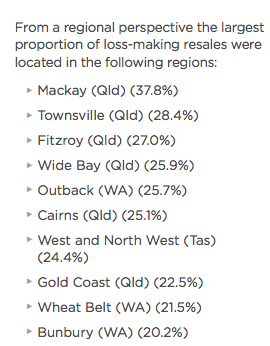

And where you buy also determines success or failure:

CoreLogic RP Data research analyst Cameron Kusher confirmed Regional Western Australia surpassed Regional Queensland for the quarter as the region to record the highest proportion of loss-making resales; Regional Western Australia recorded 22.5 per cent of all resales at a loss while Regional Queensland recorded followed at 22.0 per cent.

Mr Kusher said that while there is an improvement in buyer demand and dwelling values, the weakness in these two regions is reflective of the recent underperformance of coastal markets. “Recent data highlights the growing weakness in markets linked to the mining and resources sector where values are generally falling.”

Given the rabid increases in property prices (don’t confuse that with value) across the country, but particularly in Sydney and Melbourne, its no surprise that “the proportion of loss making resales has consistently been lower than the national average since early 2009”. The divergence with regional sectors is stark with only ca. 6% of capital cities reporting losses vs over 15% in regional markets.

This divergence is likely to continue as more speculative activity continues in Sydney and Melbourne and the mining capex cliff draws ever closer with rising unemployment putting further losses in front of those regional property speculators.