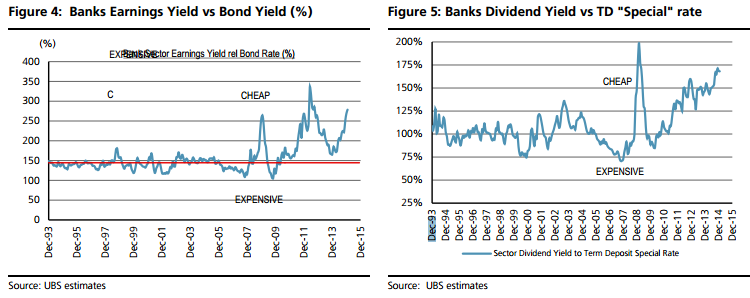

UBS is looking for another leg up in bank valuations today:

A benign outlook is not a bad thing

With a patchy economy and a pick-up in market volatility, we believe many investors are struggling for high conviction investment alternatives. With many industries under pressure, high quality franchises which offer reasonable growth have become crowded trades with stretched valuations. Australian bond yields are now near record lows and the market is pricing in rate cuts. In this environment, we believe the benign outlook and strong dividend yields of the banks make them relatively attractive investments.

Likely share price drivers over coming months

(1) Interest rates – Lower bond yields and rate cuts are negative for NIM’s. However, strong bank returns and dividends are likely to continue to attract retail investors and yield funds. Although the banks’ absolute valuations are not cheap, further re-rating is possible. (2) Capital – While this ‘can has been kicked’ for a few months, we believe many investors underestimate the potential requirements needed to make capital ratios “unquestionably strong”. The global push for more capital is ongoing with the Basel Committee focused on risk weight floors and calibration of Advanced to Standardised methods. Global peers are continuing to strengthen their capital positions. We believe APRA could adopt higher mortgage risk weights sooner rather than later. (3) Bad Debts – Can the banks continue to write-back provisions and release CP to hold charges at record low levels? (4) Trading income – should bounce back give increased volatility especially in the AUD. This may provide the biggest leverage to ANZ & WBC near term.

Jonathon Mott is a good analyst and I’m inclined to agree with him. Bad debts won’t really rise until the commodity bust begins to drag down housing and that’s probably a 2016 story, outside of Perth.

Last night the US 30 year bond hit another all time low and Australian bond yields will continue to price lower as well as rate cuts come and go, not do enough, and be priced again.

Advertisement

With the Fed not raising rates this year, either, there’s potential for one last leg up in the local yield play. Especially since the global backdrop is ZIRP everywhere. FTAlphaville quotes BofAML which suggests European yield stocks could double:

“Safe” dividend stocks, to be precise.

It’s a straightforward argument: as yields on high-grade government debt increasingly turn negative, so the search for income amongst investors will channel money into quality equities.

Barnaby Martin and Manish Kabra at BoA Merrill Lynch reckon that with the stock of such negative yielding debt in the Eurozone now close to €1.4 trillion and Japan now pushing towards €2.4 trillion, there’s a distinct lack of alternatives…

That’s over the top given the business cycle is clearly getting long in tooth but it may still be valid for another leg up. Then again, that’s kinda contradictory, no? Why would I buy yield for short term trade?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.