From Westpac:

Four of the five components that go into the calculation of the Westpac MNI China CSI declined from the previous month. Current family finances, business conditions ‘one year ahead’ and ‘five years ahead’, and ‘time to buy a major household item’ all moved lower. Family finances ‘one year ahead’increased strongly though, presumably jointly reflecting the lower inflation and interest rate expectations reported elsewhere in the survey. Current business conditions (not a part of the headline composite, but tightly correlated with official industrial production data) were basically steady.

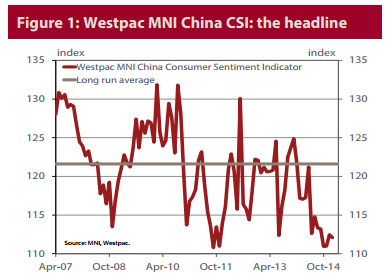

We noted a month ago that forward looking indicators of the economy had improved more so than the coincident ones. In January, we build on that observation by noting that the “current” portion of the headline index is down by 11.3% from a year ago, whereas the “expected” portion is down by a lesser 5.9%. The gap between current and expected readings over the last year is most pronounced in family finances, where there is an 8ppt gap. We note that annual minimum wage increases have impacted upon the expected measure in the past, so we await the various provincial announcements with great interest.

The employment indicator declined by a cumulative 11.3% between May and October, and has increased by 2.4% in Nov-Jan combined. The January reading is 8.9% below long run average. The survey is arguing that in absolute terms job security remains in short supply, notwithstanding the fact the indicator is off its lows. Consumers seem to be awaiting a durable pick-up in demand conditions before they fundamentally reassess the outlook for the labour market.

The consumers’ attitude towards real estate (see table 3 on page 4 of the bulletin) was mixed in January, following on from back-to-back improvements in Nov-Dec. Expectations for house pricesshed some ground and the share of respondents reporting it was a ‘good time to buy a house’declined. However, 19.3% of consumers now nominate domestic real estate as the ‘wisest place for their savings’, the highest since June. Also on the positive side of the ledger, the proportion of consumers nominating a housing purchase as their primary motivation for saving, rose for a second month. Looking more closely at the house price results, there is a widening gulf between the East and the Central & Western (C&W) regions. This indicator is down a cumulative 2.1% since June 2014 in the East versus 10.9% in the C&W. That tallies nicely with the official house price and activity data, where the market consolidation, such as it is, is basically confined to the wealthy coastal cities.

Consumers reported considerably lower levels of confidence in the share market performance of firms with real estate linkages in January. Margin lending curbs also served to lower the proportion of respondents nominating equities as the ‘wisest place for their savings’. Investors felt the stock market became better value over the month, with literally zero respondents nominating it was “very expensive”, but 3 month stock price expectations still decreased by 1.8%.

Buying conditions reportedly improved in the markets for cars, IT products, communications devices and other appliances, while expected spending on shopping moved higher. Expected spending ondiscretionary services edged lower. 17.7% of respondents are planning a car purchase in the next year, up from 13.8% in December.

Not a lot of ‘rebalancing towards the consumer’ in that lot. Full report.